Wage Reporting: Need to Know

SUTA Dumping

SUTA dumping involves the manipulation of an employer's unemployment tax rate and/or payroll reporting to owe less in unemployment taxes. DWD is committed to investigating, detecting, and preventing this practice and maintains a SUTA Dumping Investigation Unit for this purpose. It is important to abide by the following to avoid running afoul of the SUTA dumping law:

Mandatory Transfers

UI experience account balances must be transferred whenever there is:

- Substantially common ownership, management, or control between the parties

- One entity transfers all or part of its trade or business (including its workforce) to another entity

Both the employer from which the employees / assets exited and the employer to which the employees / assets were received must report the transfer to Indiana. See the prior section, Transfers, for reporting requirements.

Prohibited Transfers

A new employer acquiring the trade or business of an existing employer for the sole purpose of qualifying for a lower premium rate is not entitled to the previous owner’s UI experience account. This practice results in higher rates for other employers and is not allowed. A new employer premium rate will be assigned. See the section titled Selling and Acquiring Businesses for additional information. Existing businesses are also prohibited from acquiring a different trade or business for the purpose of transferring their workforce to another account with a lower UI experience rating.

Penalties for SUTA Dumping Any employer that knowingly violates or attempts to violate the law regarding SUTA Dumping will be subject to the highest premium rate for the year in which they violated the act and for the following three years. If the employer is already at the highest tax rate or if the amount of the increase is less than 2%, a penalty of 2% additional contributions will be imposed. Any person that advises an employer on how to carry out SUTA Dumping is subject to a civil penalty of up to $5,000 per incident. This penalty is assessed to non-employers such as accountants, attorneys, tax advisors, and third-party reporting agents that knowingly or recklessly assist or advise an employer in violating the requirements of the Act. |

Why SUTA Dumping is Harmful

Under the experience rating system, employers pay UI premiums at a rate that is based on the benefit claims filed against their business and the amount of wages paid.

Employers with more employees receiving UI benefits should pay higher premium rates. Employers with fewer employees claiming UI benefits should pay less.

Employers who engage in SUTA Dumping practices (or other tax schemes) to avoid paying their fair share unfairly shift the burden to other employers.

SUTA Dumping is harmful because it:

- Compromises the integrity of the UI system

- Results in an uneven playing field

- Increases rates for all employers

- Results in the UI Trust Fund losing money

Terminating a Business

The form of notification required by DWD is SF46800, SUTA Account Termination or Transfer Request, which can be located here or by calling (800) 891-6499 and select the employer option. SF46800 should be filed within thirty (30) days of the final decision to cease business operations. |

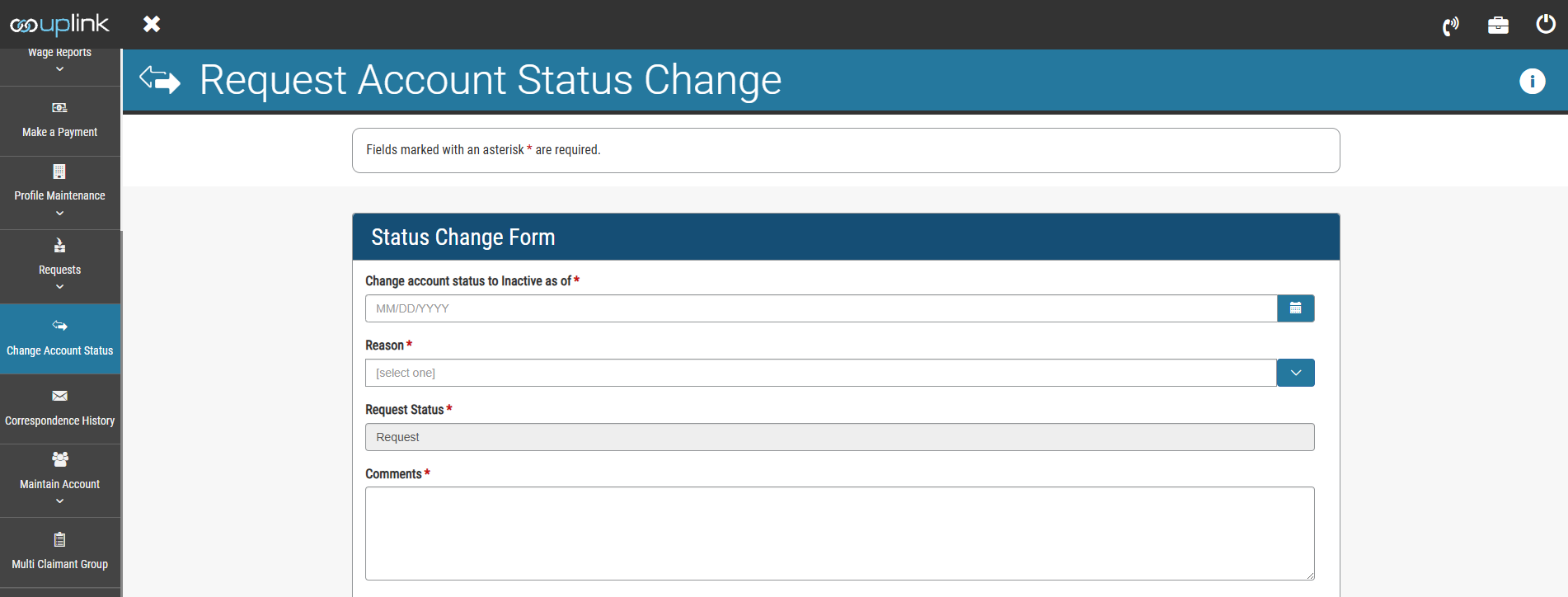

To Change your Account Status, you can:

|

Organizations are required to file documentation with DWD if they are ceasing to operate, distributing assets, or otherwise removing themselves from Indiana operations whether voluntarily or involuntarily. This requirement applies to all organizations whether non-profit, for profit, corporate or noncorporate entities.

If the organization fails to notify DWD as required, all responsible parties will become personally responsible for any liabilities owed to DWD under the Act. A responsible party is (1) for a corporate entity, the corporation’s officers and directors; or (2) for a non-corporate entity, the entity’s chief executive.

Failure to timely file the notice of dissolution can result in the assessment of penalties in addition to any other assessments made against the organization and / or the organization’s responsible parties. The penalty is thirty percent (30%) of the contribution outstanding at the time of the dissolution assessed to the responsible parties if reasonable efforts are not made to set aside assets to pay DWD at the time of dissolution.

If the organization is in good standing with DWD at the time of the cessation of business operations, and if a responsible party timely files SF46800 along with a request in writing for a clearance letter, DWD will issue such clearance releasing the responsible parties from personal liability for any outstanding liability to DWD. Only those responsible parties disclosed to DWD as an attachment to the SF46800 can be protected by DWD’s issuance of a clearance letter.