Flood Risk and Flood Insurance

The importance of purchasing flood insurance in Indiana

Flooding is one of the most common natural disasters that occur in the United States, with 99% of U.S. counties being affected since 1996. Indiana experienced 65 flooding or heavy rain events in 2024 alone. According to the Federal Emergency Management Agency (FEMA), $281 million of FEMA flood insurance claims have been paid in Indiana since 1980. There are more than 2.5 million households in Indiana, but only 15,781 insurance policies in effect as of 2025, per FEMA. Despite the severe financial harm flooding hazards present, less than 1% of the state's households are covered.

In an effort to reduce the number of homes financially devastated by flooding, the Indiana Department of Homeland Security (IDHS), Indiana Department of Natural Resources (DNR), Indiana Department of Insurance (IDOI) and FEMA encourage all Hoosier homeowners and renters to purchase flood insurance protection. While purchasing flood insurance might seem costly, the National Flood Insurance Program (NFIP) is available to help provide citizens flood insurance coverage based on the area they live in.

Ready to buy flood insurance?

Contact your insurance agent or use the floodsmart.gov tool linked below to look up insurance providers that offer the National Flood Insurance Program.

The NFIP is a federal program designed to reduce the impact of flooding by providing flood insurance policies to property owners, renters and businesses all around the United States. NFIP policies oftentimes can be purchased through the same insurance agents who provide homeowner's and renter's insurance. Once purchased, NFIP policies can take up to 30 days to go into effect. Learn more about the NFIP at floodsmart.gov.

{kind=link}

A standard homeowner's and renter's insurance policy does not automatically include flood insurance protection. Homes in high-risk flood areas with mortgages from federally regulated or insured lenders are required to have flood insurance. Even if flood insurance isn't required, it is still important to purchase.

IDHS Director of Emergency Management Mary Moran says it is crucial for all Indiana residents to purchase flood insurance.

"Everyone lives in a floodplain. It is just a question of how much water it takes to impact their structures," Moran said. "No home is completely safe from the risks of flooding."

In 2021 there were 103 flash floods, floods or heavy rain events in Indiana. These events led to 123 flood insurance claims, which paid property owners and renters nearly $3.5 million. An important note about this is that there were no federally declared disasters in the state for 2021. In order for property owners or renters to be eligible for disaster assistance, there must be a federal disaster declaration. Even then, typical disaster relief payments are in average amounts of about $1,600–$1,800. Property owners and renters may also be eligible for low-interest loans to repair damages. However, these must be paid back and can be burdensome if they already have a mortgage. Having flood insurance is the best solution to a faster and more whole recovery.

According to FEMA, high-risk flood zone areas have at least a one-in-four chance of flooding during a 30-year period. Nationally, almost 40 percent of flood-insurance claims come from low-to-moderate risk areas or areas outside the mapped flood hazard areas on the Flood Insurance Rate Map (FIRM).

FEMA "Before, During & After" podcast episode

FEMA discussed misconceptions about the flood insurance program and how the program is designed to help people protect themselves.

Several factors influence the cost of flood insurance:

- Distance to the flooding source

- Amount and type of coverage

- Replacement cost of the structure

- Type of construction

- Deductible you choose (building and contents)

- Amount of coverage you choose (building and contents)

It is important to note that flood insurance prices do not differ between different insurance companies.

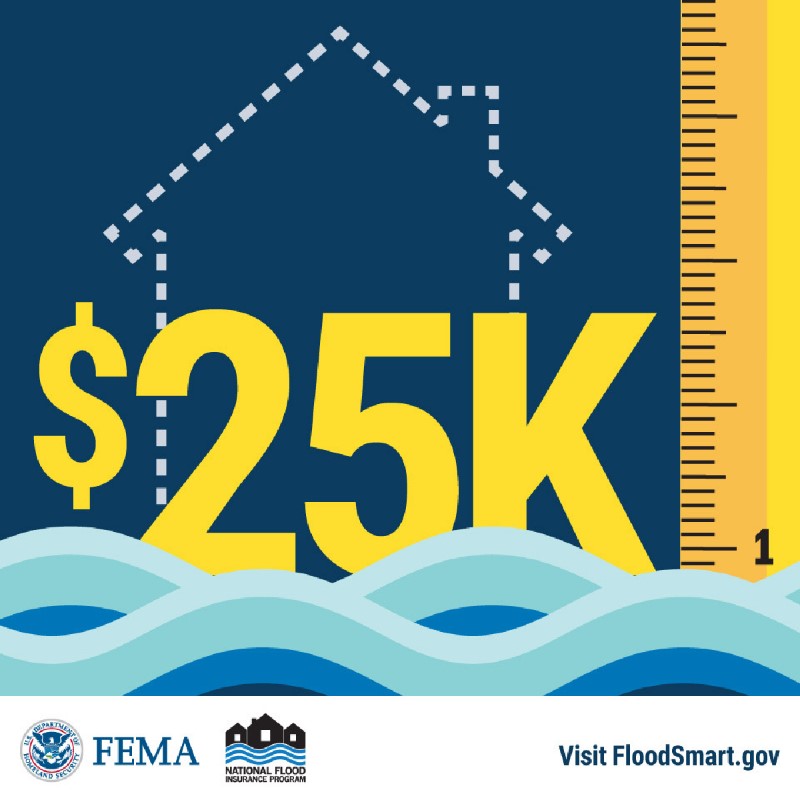

Paying for a flood insurance policy ensures cost efficiency when recovering from flood damage, even if there hasn't been a Presidential Disaster Declaration. According to FEMA, just 1 inch of water can cause approximately $25,000 of damage to an average 2,500 square-foot, one-story home. Rather than paying straight out of pocket or through loans, flood insurance will cover the majority of the cost.

Use FEMA's Estimated Flood Loss Potential document to determine your home's estimated flood loss potential.

FEMA provides information to help citizens understand how NFIP flood insurance premiums are determined. Both homeowners and renters can use FEMA’s Policy Quote Tool to determine policy and premium costs. FEMA’s Flood Insurance Mitigation Discount Tool can help estimate potential insurance premium discounts for mitigation efforts.

The Indiana Floodplain Information Portal (INFIP) is a mapping application developed by the DNR, Division of Water, that provides floodplain information for public use. The portal displays floodplain information from both FEMA and DNR sources, including mapped floodplains and flood elevation points along waterways. In addition, the revised INFIP allows users to generate a Floodplain Analysis and Regulatory Assessment (FARA) by using the FARA Report Generator. A FARA is required for local floodplain permitting and FEMA Letter of Map Amendment applications in A zones.

- A FARA is also required for regulatory determination when the upstream drainage area is greater than 1 square mile, for areas that are unmapped on the FIRM or for areas known to be flood prone.

- Base Flood Elevation (BFE) determinations are often used for proposed development and flood insurance purposes.

- The Indiana Floodplain Information Portal (INFIP) displays the Best Available Floodplain mapping as well as the BFE.

- The layers tab allows the user to view the effective layer.

- A FARA can be generated by selecting “run” once a point is selected.

- A BFE will be provided for the site, then the FARA should be downloaded and saved by the user for future reference.

- There is the opportunity for users to submit a site for review if they wish to contest the FARA, if their site is near a stream without a mapped floodplain/floodway or if their point is nearest to a stream with no floodplain and the tool took the BFE from a different stream.

First-time users of the site are encouraged to carefully review the instructions to the right side of the page when it opens.

Indiana Department of Insurance (IDOI) resources

How to choose a company and agent

Before purchasing a policy, check the company's financial condition. You can do this by asking the agent and a number of insurance rating services to rate the financial strength of the company. Collect the names of several agents (also called producers) through recommendations from friends, family and other sources. Visit the IDOI Getting Started page to see the questions you should ask before making your decision.

Insurance claim tips

To help avoid problems getting claims paid, follow the tips on the IDOI Insurance Claim Tips page.

Actual cash value versus replacement cost

You have choices when insuring your home and personal property with a homeowner's insurance policy. Actual Cash Value or Replacement Cost coverage are two different options. Take a look at each and decide which is best for you. It's your choice; get covered.

How to file a consumer complaint

The primary role of the IDOI Consumer Services Department is to protect consumers from illegal insurance practices by ensuring that insurance companies and producers that operate in Indiana act in accordance with state insurance laws. IDOI assists Hoosiers with insurance questions and complaints about health, life, automobile and property and casualty insurance. Complaints must be received in writing. Learn how to file a consumer complaint

More flood insurance tips and tools

The following are resources offered by the National Association of Insurance Commissioners (NAIC).

Flood insurance basics

Know the facts before you buy flood insurance. Use this helpful guide to learn more about the basics of flood insurance.

Go-Bag interactive tool

Pack a go-bag with disaster essentials to reduce your risks during and after a storm. See what you should pack with the NAIC interactive Go-Bag tool.

What The Flood! quiz

See if you have what it takes to protect your home from flood, and test your knowledge of flood-related insurance with the NAIC What the Flood! quiz.

NAIC home inventory

The NAIC Home Inventory App makes it easy for you to make a home inventory and be prepared in case of damage to your home and belongings. Download the app in the App Store or in Google Play.

Myths versus realities

The risks associated with flooding are real, and it affects more people than many realize. Flooding can happen to anyone at any time anywhere it rains. The Myths vs. Realities tab on the NAIC Flood Insurance page will clear up some misconceptions about flooding and flood insurance to help you better understand your flood risk and policy options.