Search for Keywords

- A

Affordable Care Act Penalties, Fines, or Tax

Annual Financial Report

Annual Financial Report and 100-R Not Filed Timely

Annual Financial Report vs Annual Report

We have received inquiries concerning who has the responsibility regarding access and retention of public records such as when a bank/payroll vendor will be serving as an agent for an Indiana governmental unit. An example would be a bank only offers to provide on line access to cancelled checks. We consulted with the Indiana Commission on Public Records and the response we received provided in part "The bank/vendor would thus be required to maintain the checks, bank statements, payroll records, etc. for the same period as the agency. The bank/vendor may well hold the information, but the obligation remains with the agency to provide access upon request, not the bank or vendor. The agency further has the obligation to provide access to the materials throughout the required retention. In the case of cancelled checks/warrants they are currently required to be maintained for 6 (six) years after the completion of the State Board of Accounts Audit. Payroll records are dependent upon the type."

Township Form 1C, Financial and Appropriation Record, has been prescribed to be used as the ledger of Townships. This is a manual system. In lieu of using this ‘ledger book,’ many Townships are switching to some form of computerized accounting systems. We receive quite a few questions asking us what systems we approve and suggest. We do NOT approve systems and cannot suggest which ones to use. If you are thinking of switch to a computerize system (or switching systems), there are a couple of things you need to keep in mind. First, all output forms from the system must be replicas of the forms that we prescribe. A list of those forms can be seen in Chapter 2 of the Township Manual. There is a provision in the March 2014 Bulletin that allows for approval of forms that are not exact replicas.

AFFORDABLE CARE ACT PENALTIES, FINES, OR TAX

The State Board of Accounts has received many questions regarding our audit position with regards to the Affordable Care Act. Most of the questions have inquired specifically about the penalties, fines, or tax associated with this law. While our general audit guidelines prohibit the paying of penalties and interest and states that those payments would be a personal charge to the fiscal officer, administrator, or board, we do not believe this general guideline should apply to this controversial, mandated, and complicated law.

We also believe that the governing boards should be making the fiscal decisions associated with their unit of government and the implementation of this law. Therefore, if the fiscally wise decision of the board is to pay the penalties, fines, or tax instead of the cost of the insurance then we will not personally charge the officials involved. One of the conditions necessary to not charging the penalties, fines, or tax is to have the governing board officially document their decision to not comply with the Affordable Care Act. This could be a motion in the board minutes, a resolution, or an ordinance.

In summary, as long as there is an official action of the board to choose to pay the fines, penalties, or tax, the State Board of Accounts will not personally hold anyone in that unit of government accountable for reimbursing the cost of those penalties, fines, or tax.

IC 5-3-1-3 applies when another statute requires meetings or notices to be published. If the statute that requires the meeting does not mention IC 5-3-1-3, then you would follow the requirements of the open door law (IC 5-14-1.5). Meetings that follow the requirements of the open door law would require notice posted 48 hours in advance and it is not required to publish notice in the newspaper(s).

The dates and the medium of certain notices required by statute are outlined below:

- Notice of meetings not specifically mentioned in statute – 48 hours (Notice by Township Office).

- Elections – 10 days before the date of the election (Newspaper).

- Sale of Bonds – 15 days before the sale and the second publication at least 3 days before the sale (Newspaper).

- Receiving Bids – published twice, with at least 1 week apart and at least 7 days before bids are received (Newspaper).

- Establishment of Cumulative or Sinking fund – published twice, with at least 1 week apart and at least 3 days before hearing (Newspaper).

- Publication of Annual Report – within 4 weeks after the third Tuesday following the first Monday in January (2 Newspapers).

- Indebtedness of Township – first Monday of August (Notice by Township Office).

- Budgets – Refer to the Budget and Tax Rate Calendar provided by the Department of Local Government Finance (DLGF).

If the Officer is charged with the duty of publishing any notice required by law and is unable to procure publication of the notice at either (1) the price fixed by law, (2) because newspapers qualified to publish refuse to publish, or (3) because newspapers qualified to publish refuse to post notice on their respective websites, it is sufficient for the officer to post printed notices in three prominent places in the Township.

IC 5-3-1-2.3 applies to notices containing errors or omissions. Notice is not required to be republished if (1) a reasonable person would not be misled by the error or omission and (2) the notice is in substantial compliance with the time and publication requirements.

When you are required to publish in two newspapers, but you do not have two newspapers published in your Township, then you only have to advertise in one. If you do not have a newspaper published in your Township, then you would advertise in a newspaper that is published in your County and circulates within your Township.

ANNUAL FINANCIAL REPORT AND 100-R NOT FILED TIMELY

We want to remind all Townships that we will continue our practice of issuing subpoenas to the Trustee if the Certified Personnel Report (100-R) and the Annual Financial Report (AFR) are not filed timely in Gateway. The 100-R is due by January 31st and the AFR is due by March 1st.

The Annual Financial Report and 100-R must be filed through Gateway. To login to Gateway, please go to https://gateway.ifionline.org/login.aspx and enter your Gateway User Name (e-mail address) and Password.

Please be aware that any person who fails to file the Annual Financial Report as required by law commits a Class B infraction and forfeits office. Ind. Code § 5-11-1-10.

Indiana Code 5-11-1-4(a) states in part: “The state examiner shall require from every municipality and every state or local governmental unit, entity, or instrumentality financial reports covering the full period of each fiscal year. These reports shall be prepared, verified, and filed with the state examiner not later than sixty (60) days after the close of each fiscal year. The reports must be in the form and content prescribed by the state examiner and filed electronically . . . “

Please be aware that any person who fails to file the 100R Report as required by law commits a Class C infraction and is subject to impeachment or removal from office. Ind. Code § 5-11-13-3. Indiana Code 5-11-13-1 states in part: "Every state, county, city, town, township, or school official . . . shall during the month of January of each year prepare, make, and sign a written or printed certified report, correctly and completely showing the names and addresses of each and all officers, employees, and agents . . . and the respective duties and compensation of each, and shall forthwith file said report in the office of the state examiner of the state board of accounts."

ANNUAL FINANCIAL REPORT VS. ANNUAL REPORT

We have received inquiries about the Annual Financial Report (AFR) and if the incoming Trustee or the outgoing Trustee is required to submit this in Gateway.

The incoming Trustee would be responsible for submitting the Annual Financial Report in Gateway and performing any duties of the Trustee when the office expires. There are three reports commonly referred to as the Annual report:

1. Report required by IC 36-6-4-12 to be presented to the Township Board;

2. Report required by IC 36-6-4-13 to be published in accordance with IC 5-3-1; and

3. Report required by IC 5-11-1-4 to be filed with the State Examiner (AFR in Gateway)

The first report should be presented to the incoming Trustee by the outgoing Trustee required by IC 36-6-4-12 no later than the 3rd Tuesday after the first Monday in February. We have designed the Gateway submission to accomplish all three required reports. The outgoing Trustee can have “edit rights” to the Gateway system and fill out the necessary information to print out a report to fulfill their duties in IC 36-6-4-12. Then the incoming Trustee could go in and verify the information input with the ledger and submit the AFR in Gateway before the deadline on March 1st. The prior Trustee providing this assistance is not required but recommended for a smooth transition if elected officials are changing. If the Gateway report is not submitted by the 3rd Tuesday after the first Monday in February the incoming Trustee can produce a custom report, that would be similar to the “Cash and Investment Combined” report in the AFR, from information recorded in the ledger.

ASSESSING EXPENSES - Bond premium paid by County

The bond premium on the official bond of the township assessor should be paid from county funds and not from township funds.

IC 5-4-1-18 states in part (a)". . . the following . . . individuals shall file and maintain in place an individual surety bond: . . . (4) Township assessors. . . ". We are not aware of any statutory requirements for a deputy assessor to execute a bond: however, such a bond may be required by the elected township assessor. When so required, such bond must be recorded in the office of the county recorder.

IC 6-1.1-3-5 states: "Before the assessment date of each year, the county auditor shall deliver to each township assessor the proper assessment books and necessary blanks for the listing and assessment of personal property."

Inquiries have questioned the correct procedure for accounting for township audit costs.

We find IC 5-11-4-3(b) remains applicable to guide these processes. IC 5-11-4-3(b) states in part: “… Immediately upon receipt of the certified statement, the county auditor shall issue a warrant on the county treasurer payable to the treasurer of state out of the general fund of the county for the amount stated in the certificate. The county auditor shall reimburse the county general fund, except for the expense of examination and investigation of county office, out of the money due the taxing units at the next semiannual settlement of the collection of taxes.”

Therefore, counties shall continue to forward examination of record payments to the Treasurer of State for township audits when billed by the State Board of Accounts. The county general fund shall then be reimbursed from property tax collections of that township at the next semiannual settlement.

To properly account for the township’s audit costs the full amount of property and excise taxes (before audit costs) are to be receipted to the appropriate township funds. A disbursement for the examination of records is to be posted to township funds. The Statement of Engagement Costs should be compared to the amount withheld for the Examination of Records to ensure the amounts agree.

IC 5-11-4-4 provides that all disbursing offices are authorized to make payments required under this chapter without appropriation. Therefore, the examination of records costs would be considered an unappropriated disbursement.

- B

Bonds of Officers and Employees of the Department of Parks and Recreation

The Office of the Attorney General of the State of Indiana provided the following Unofficial Advisory Letter on June 11, 1991 in response to a request for an opinion concerning the following questions:

1. May the Township Board appoint its own attorney?

2. May the Trustee as the authorization officer for Poor Relief funds and the distribution officer for Civil funds compensate a Township Board Attorney?

3. After salaries have been fixed by the Township Board, is the Township Executive compelled to compensate employees to the fullest extent of salaries provided, even though the employee may be deficient when evaluated by written performance appraisal in view of Indiana Code Section 36-4-7-2.

CONCLUSION

1. The Township Board is not authorized to appoint its own attorney.

2. This question is moot. See question 1.

3. The Township Trustee does not have the authority to change the salary of an employee that is fixed by the Township Board. The Township Board may not change the salary of an elected or appointed officer during the fiscal year for which they are fixed. The Township Board may change the salary of any other employee. The Township Trustee may remove any employee who is deficient in the performance of his or her duties. If procedure for removal has been provided, the Township Trustee should follow that procedure.

Subsequent to the issuance of the aforementioned Advisory Letter questions have been raised of whether "Home Rule" would provide authority for a township board to also hire an attorney. IC 36-6-4-4 states in part concerning powers of a township trustee: "The executive may do the following . . . Appoint an attorney to represent the township in any proceeding in which the township is interested." The question was asked in Attorney General Advisory Opinion 98-13 issued July 9, 1998, "Can a school corporation or other unit of government expand the provisions of a statute with "home rule?" The answer provided by the Attorney General’s Office stated in part ". . . those entities may not exercise home rule powers in an area pre-empted by the General Assembly."

IC 36-6-6-10(b) states in part: “The township legislative body shall fix the: (1) salaries; (2) wages; (3) rates of hourly pay; and (4) remuneration other than statutory allowances; of all officers and employees of the township.”

We suggest that this be done in conjunction with the board approval of the Township budget, however, just approving the budget is NOT sufficient to fulfill this statute. The board must fix the sales, wages, rates of pay, etc. of all officers and employees in a public meeting. This can be done through a resolution if the board so chooses. The Township Form 17, as described in Chapter 2 of the Township Manual is an optional form that has been provided for this purpose. A sample of the Form 17 can be seen in the appendix as well.

A couple of other statutes to keep in mind when completing this:

IC 36-6-6-10 states in part: “(c) Subject to subsection (d), the township legislative body may reduce the salary of an elected or appointed official. However, except as provided in subsection (h), the official is entitled to a salary that is not less than the salary fixed for the first year of the term of office that immediately preceded the current term of office.

(d) Except as provided in subsection (h), the township legislative body may not alter the salaries of elected or appointed officers during the fiscal year for which they are fixed, but it may add or eliminate any other position and change the salary of any other employee, if the necessary funds and appropriations are available.

(e) If a change in the mileage allowance paid to state officers and employees is established by July 1 of any year, that change shall be included in the compensation fixed for the township executive and assessor under this section, to take effect January 1 of the next year. However, the township legislative body may by ordinance provide for the change in the sum per mile to take effect before January 1 of the next year.

(f) The township legislative body may not reduce the salary of the township executive without the consent of the township executive during the term of office of the township executive as set forth in IC 36-6-4-2.

(g) This subsection applies when a township executive dies or resigns from office. The person filling the vacancy of the township executive shall receive at least the same salary the previous township executive received for the remainder of the unexpired term of office of the township executive (as set forth in IC 36-6-4-2), unless the person consents to a reduction in salary.

(h) In a year in which there is not an election of members to the township legislative body, the township legislative body may vote to reduce the salaries of the members of the township legislative body by any amount.”

BONDS OF OFFICERS AND EMPLOYEES OF THE DEPARTMENT OF PARKS AND RECREATION

IC 36-10-3-16 provides "(a) Every officer and employee who handles money in the performance of duties as prescribed by this chapter shall execute an official bond for the term of office or employment before entering upon the duties of the office or employment. (b) The fiscal body of the unit may under IC 5-4-1-18 authorize the purchase of a blanket bond or crime insurance policy endorsed to include faithful performance to cover all officers' and employees' faithful performance of duties. The amount of the bond or crime insurance policy shall be fixed by the fiscal body and, in the case of a municipality, must be approved by the executive. (c) All official bonds shall be filed and recorded in the office of the county recorder of the county in which the department is located. (d) The commissioner of insurance shall prescribe the form of the bonds or crime policies required by this section."

OFFICIAL BONDS

The bond amount for a Township Trustee must be thirty thousand dollars ($30,000) for each one million dollars ($1,000,000) of receipts of the Township during the last complete fiscal year before the purchase of the bond. The bond amount must be at least $30,000, but not greater than $300,000 unless approved by the fiscal body. [IC 5-4-1-18(d)(1), (2)]

Employees or contractors of a Township “whose official duties include receiving, processing, depositing, disbursing, or otherwise having access to funds that belong to the federal government, the state, a political subdivision, or another governmental entity” must have a bond of at least $5,000. [IC 5- 4-1-18(a)(7), (e)(2)]

The SBOA may increase minimum bond coverage amounts if an examination report finds malfeasance, misfeasance, or nonfeasance that resulted in the misappropriation of, diversion of, or inability to account for public funds. [IC 5-4-1-18(j), (k), (l)]

Effective January 1, 2016, all bonds must have a one year term. A continuation certificate is not sufficient. Consecutive yearly bonds must provide separate coverage for each year. [IC 5-4-1 18(m)(1), (2)]

We will not take exception to a new calendar year bond term greater than one year if the current bond expires before December 31, 2015. For example, if the current bond expires on September 30, 2015, we will not take exception to a new bond term from October 1, 2015 to December 31, 2016, even though it is greater than one year. Similarly, we will not take exception to a new calendar year bond term less than one year if the current bond expires after December 31, 2015, but before December 31, 2016. For example, if the current bond expires on March 31, 2016, we will not take exception to a new bond term from April 1, 2016 to December 31, 2016, even though it is less than one year.

Term bonds issued on or after January 1, 2016, are not allowable [IC 5-4-1-18(m)(1)] We recommend that all current term bonds be converted to one year bonds starting January 1, 2016, to comply with the spirit of the amended statute and to reduce the risk of financial exposure to the Township.

Blanket bonds are allowable if they are authorized by resolution, endorsed to cover faithful performance, and include aggregate coverage sufficient to cover all officers, employees, and contractors required to be bonded. [IC 5-4-1-18(b)]

We will not take exception to schedule bonds—by name or position—if the bonds are authorized by resolution, endorsed to cover faithful performance, and include aggregate coverage sufficient to cover all officers, employees, and contractors required to be bonded.

Crime insurance policies providing additional coverage for criminal acts or omissions committed by officers, employees, or contractors are permitted if they are authorized by resolution. [IC 5-4 1-18(c)] We will not take exception if a Township purchases a crime insurance policy in lieu of a bond if the crime insurance policy is authorized by resolution, endorsed to cover faithful performance, and includes aggregate coverage sufficient to cover all officers, employees, and contractors required to be bonded.

The aggregate liability for a surety or insurer for a policy year is the sum of the amounts specified in the bonds issued by the surety or insurer for that policy year. [IC 5-4-1-18(m)(2)] For example, if a Trustee has four consecutive yearly bonds for $30,000, the maximum liability of the insurer is $30,000 for each of the four years.

Effective January 1, 2016, all bonds must commence on one of the following: The first day of the calendar year; the first day of the fiscal year of the Township; or the first day of the individual’s service in the office or employment position for which a bond is required. [IC 5-4-1-18(m)(1)]

All official bonds shall be made payable to the State of Indiana. [IC 5-4-1-10] The State is considered an additional named insured on all crime insurance policies. [IC 5-4-1-18(c)]

All bonds must be filed with the county. Beginning July 1, 2015, copies of the bonds must also be filed with the Trustee. [IC 5-4-1-5.1(b)]

Bonds must be filed with the county recorder and the Trustee within ten days after their issuance. [IC 5-4-1-5.1(c)]

The Trustee must submit copies of all bonds to the State Board of Accounts electronically via Gateway with their Annual Financial Report. [IC 5-4-1-5.1(e)]

Current bonds already filed with the county recorder are not required to be re-filed with the Trustee. For example, a bond obtained in January 2015, and properly filed with the county recorder does not need to be filed with the Trustee. However, when the January 2015 bond expires and a new bond is obtained in January 2016, it must be filed with both the county recorder and the Trustee.

Indiana Code 5-4-1-18(a)(7) states that bonds are required for individuals: “(A) who are employees or contractors of a city, town, county, or Township; and (B) whose official duties include receiving, processing, depositing, disbursing, or otherwise having access to funds that belong to the federal government, the state, a political subdivision, or another governmental entity.” It is our position that for the purposes of IC 5-4-1-18(a)(7), a ‘contractor’ is a person or business in a contractual relationship with the Township who has a fiduciary relationship with or performs a fiscal responsibility for the Township, and whose accounts are not otherwise covered by the Federal Deposit Insurance Corporation (FDIC). For example, a contractor providing payroll or billing services for the Township is required to be bonded, but a snow removal contractor or lawn service provider is likely not required to be bonded.

The Township must determine who must be bonded under the statute. The term ‘official duties’ is not defined. It is our position that ‘official duties’ may include duties set forth in a job description, duties that are customary or routinely performed, or duties that are assigned but not frequently performed. For example, if an office has three employees who routinely accept payments in the Townships office, then all three employees must be bonded. If an employee is assigned to accept certain registration fees but only receives funds once every other year, then that employee must be bonded.

There is no dollar threshold or de minimis exception in the statute. However, we will not take exception if employees of the Township who receive, process, deposit, disburse, or otherwise have access to public funds in an amount less than $5,000 are not bonded.

- C

Cash Balance -vs- Appropriation Balance

Establishing the Estimated Cost of Capital Assets

Cemeteries

Attorney General Official Opinion 91-5 – Cemeteries

Certification of Names and Addresses to County Treasurers

Compensatory Time Off Under the Fair Labor Standards Act

When Trustee receives Township Assistance

Cumulative Fire Fund (Building or Remodeling and Fire Equipment Fund)

Cybersecurity Incidents - Reporting

CASH BALANCE -VS- APPROPRIATION BALANCE

We receive numerous questions from Trustees and other Township employees that are confused about the difference between their cash balance and their appropriation (or budget) balance. Your cash balance is the amount of cash you have available to spend. This should be reflected in your ledgers and should be reconciled to your bank on monthly basis.

Each year, you work with the DLGF and get a budget passed for your unit. This is your appropriation balance. Whereas your cash balance is the amount of cash you have available to spend, your appropriation balance is what you are allowed to spend. Most, if not all times, these balances will not be the same.

A couple of things to remember. Receipts increase your cash balance, but do NOT increase your appropriation balance. For funds that have an appropriation (there are some funds that do not require a budget), the most common of which are the Township (General) Fund, Fire Fighting Fund, Township Assistance Fund, and Rainy Day Fund, disbursements decrease both your cash balance and your appropriation balance. There are cases in which a disbursement could be made ‘unappropriated,’ but that is very rare. If you get to a point during the course of a year, where you still have cash available to spend, but no longer have an appropriation balance, you can request an additional appropriation from the DLGF. That process is outlined in Chapter 4 of our Township Manual.

To ensure adequate safeguards over capital assets, townships should maintain proper asset records. The State Board of Accounts has a prescribed Capital Assets Ledger, General Form No. 369. Substitute computerized forms approved by the State Board of Accounts may be used.

Every governmental unit should have a complete inventory of all capital assets owned which reflects their acquisition value. Such inventory should be recorded on the applicable Capital Assets Ledger. A complete inventory should be taken at least every two years for good internal control and for verifying account balances carried in the accounting records.

Land

The records of each governmental unit should reflect land owned, its location, its acquisition date and the cost (purchase price). If the purchase price is not available, appraised value may be used.

Buildings

A capital asset account for buildings should reflect the location of each building and the cost value (being the purchase or construction cost) and the cost of improvements, if applicable. If a building is acquired by gift, the account should reflect its appraised value at the time of acquisition.

Improvements Other Than Buildings

A capital asset account should reflect the acquisition value of permanent improvements, other than buildings, which have been added to the land. Examples of such improvements are fences, retaining walls, sidewalks, gutters, tunnels and bridges. The improvements should be valued at the purchase or construction cost.

Equipment

Tangible property of a permanent nature (other than land, buildings and improvements) should be inventoried. Examples include machinery, trucks, cars, furniture, typewriters, adding machines, calculators, bookkeeping machines, data processing equipment, desks, safes, cabinets, books, etc. The value of such items should be carried in the inventory at the purchase cost. The governing body should establish a capitalization policy that sets a dollar amount as a threshold to be used in determining which equipment items will be recorded.

Construction Work in Progress

Where construction work has not been completed in the current reporting calendar year, the cost of the project should be carried as "construction work in progress." When the project is completed, it will be placed on the inventory applicable to the assigned asset accounts.

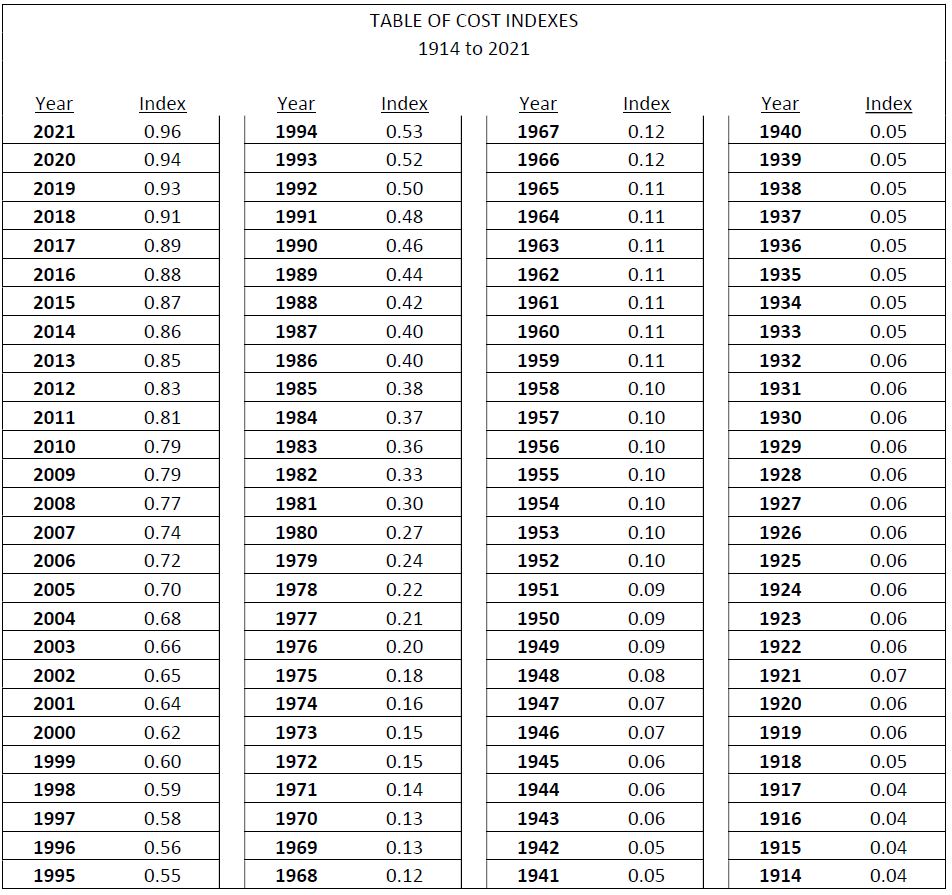

ESTABLISHING THE ESTIMATED COST OF CAPITAL ASSETS

When it is not possible to determine the historical cos of capital assets owned by a governmental unit, the following procedure should be followed.

Develop and inventory of all capital assets which are significant for which records of the historical costs are not available. Obtain an estimate of the replacement costs of these assets. Through inquiry determine the year or approximate year of acquisition. Then multiply the estimated replacement cost by the factor for the year of acquisitions from the Table of Cost Indexes. The resulting amount will be the estimated cost of the asset.

In some cases estimated replacement cost can be obtained from insurance policies; however, if estimated replacement costs are not available from insurance policies, you should obtain or make an estimate of the replacement costs.

If the replacement cost is estimated to be $76,000.00 and the asset was constructed about 1946, then the estimated cost of the asset should be reported as $6,080.00.

Township owned cemeteries are considered capital assets and need to be properly recorded on General Form 369 – Capital Assets Ledger. The cemeteries are to be reported on General Form 369 – Capital Assets Ledger at the actual or estimated historical cost based on appraisals or deflated current replacement cost. Contributed or donated assets are reported at estimated fair value at the time received. An article was published in the September 2019 Township Bulletin (Page 3) to assist in determining the estimated historical cost of the capital asset when the actual cost of the capital asset is not known - https://www.in.gov/sboa/files/TwpBULL%20September%202019.pdf. General Form 369 – Capital Assets Ledger does not have a separate classification for cemeteries, so the cemetery ground will be recorded on the capital asset ledger under land, any structures on the cemetery grounds under buildings, and roads and drainage systems will be recorded under infrastructure. There will be no effect on the value of the asset as plots are sold. The purchase of a burial plot is a real estate transaction; however, cemetery plot deeds grant burial rights that create an easement for the specific purpose of burial but do not alter the Township’s ownership of the cemetery as a whole.

Each township is required to adopt a capital asset policy that details the threshold at which an item is considered a capital asset. A complete physical inventory must be taken at least every two years, unless more stringent requirements exist, to verify account balances carried in the accounting records.

A training on properly maintaining capital assets has been added to the SBOA YouTube Channel. To access the SBOA YouTube Channel, there is a link under the Presentations and Training Materials sections of the SBOA website. You may also click on this link to view other training videos - https://www.youtube.com/channel/UC62Ozm0wY81GZHipK2UrjLA.IC 5-11-10.5-2 states: "All warrants or checks drawn upon public funds of a political subdivision that are outstanding and unpaid for a period of two (2) or more years as of the last day of December of each year are void. No individual, bank, trust company, building and loan association, or any other financial institution may honor, cash, or accept for payment or deposit any such warrant or check which may be presented for payment and which has been issued and outstanding for a period of two (2) or more years as of the last day of December of any year."

IC 5-11-10.5-3 states: "Not later than March 1 of each year, the treasurer of each political subdivision shall prepare or cause to be prepared a list in triplicate of all warrants or checks that have been outstanding for a period of two (2) or more years as of December 31 of the preceding year. The original copy of each list shall be filed with the:

- board of finance of a political subdivision; or

- fiscal body of a city or town.

The duplicate copy shall be transmitted to the disbursing officer of the political subdivision. The triplicate copy of each list shall be filed in the office of the treasurer of the political subdivision. If the treasurer serves also as the disbursing officer of the political subdivision, only two (2) copies of each list need be prepared or caused to be prepared by the treasurer."

IC 5-11-10.5-4 states: "Each list prepared under section 3 of this chapter must show:

- the date of issue of each warrant or check;

- the fund upon which the warrant or check was originally drawn;

- the name of the payee;

- the amount of each warrant or check issued; and

- the total amount represented by the warrants or checks listed for each fund. "

IC 5-11-10.5-5 states: "(a) Upon the preparation and transmission of the copies of the list of the outstanding warrants or checks, the treasurer of the political subdivision shall enter the amounts so listed as a receipt into the fund or funds from which they were originally drawn and shall also remove the warrants or checks from the record of outstanding warrants or checks. (b) If the disbursing officer does not serve also as treasurer of the political subdivision, the disbursing officer shall also enter the amounts so listed as a receipt into the fund or funds from which the warrants or checks were originally drawn. If the fund from which the warrant or check was originally drawn is not in existence, or cannot be ascertained, the amount of the outstanding warrant or check shall be receipted into the general fund of the political subdivision."

Therefore, the State Board of Accounts is of the audit position that not later than March 1 of each year, the township trustee shall prepare a list in duplicate showing: (1) the date of issue of each check; (2) the fund upon which the check was originally drawn; (3) the name of the payee; (4) the amount of each check and (5) the total amount presented by the checks listed for such fund. The original copy of such list shall be filed with the local board of finance and the duplicate copy filed with the trustee.

The amounts of such checks shall be receipted into the fund or funds from which originally drawn by writing an official receipt or receipts therefore. If the fund from which the check was drawn is not now in existence or cannot be ascertained, the amount of such check shall be receipted into the township fund. Upon issuing the receipt or receipts the checks shall then be removed from the trustee's list of outstanding checks.

CEMETERIES

Attorney General Official Opinion 91-5

The Attorney General of the State of Indiana, in response to a request for an opinion whether a cemetery may legally deny families the right to use United States government veteran markers provided the following conclusion:

It is, therefore, my Official Opinion that although the owner of every cemetery may make, adopt, and enforce rules and regulations specifying the size and type of markers or monuments under Indiana Code Section 23-14-1-11, no owner of a cemetery may adopt and enforce rules and regulations in violation of Indiana Code Chapter 23-14-11, which prohibits the board of trustees, or other governing body or custodian, controlling any cemetery in the state from refusing to allow the setting up of markers for the graves of deceased soldiers in its grounds provided that such markers shall conform to the standard markers furnished by the United States government for marking the graves of deceased soldiers of the United States army.

Many of the calls we receive regarding cemetery care involve financial-related situations and we are more than happy to provide guidance for these types of questions. However, the Indiana Department of Natural Resources (DNR) has staff that specialize in cemeteries that may have more knowledge about the State’s requirements for the upkeep and maintenance of cemeteries. For these types of questions please visit their website or contact the Indiana Department of Natural Resources.

CERTIFICATION OF NAMES AND ADDRESSES TO THE COUNTY TREASURER

IC 6-1.1-22-14(a) requires the trustee to certify the name and address of each person who has money due the person from the township to the treasurer of the county in which the township is located on or before June 1 and December 1 of each year (or more frequently if the county legislative body adopts an ordinance requiring additional certifications).

This report should not be confused with the Report of Names, Addresses, Duties and Compensation of Public Employees (Annual Personnel Report - Form 100R) required by IC 5-11-13.

USE OF COMPENSATORY TIME OFF UNDER THE FAIR LABOR STANDARDS ACT

The Fair Labor Standards Act (FLSA) is a federal law that sets standards for minimum wage, overtime, and child labor. Pursuant to an agreement with employees or their representatives, state or local government agencies may arrange for their employees to earn comp time instead of cash payment for overtime hours.

As a condition for use of compensatory time off in lieu of overtime payment in cash, an agreement of understanding must be reached prior to performance of the work. Any comp time arrangement must be established pursuant to the applicable provisions of a collective bargaining agreement, memorandum of understanding, any other agreement between the public agency and representatives of overtime-protected employees, or an agreement or understanding arrived at between the employer and employee before the performance of the work. This agreement may be evidenced by a notice to the employee that compensatory time off will be given in lieu of overtime pay (for example, providing the employee a copy of the personnel regulations). The comp time must be provided at a rate of one-and one-half hours for each overtime hour worked. For example, for most state government employees, if they work 44 hours in a single workweek (4 hours of overtime), they would be entitled to 6 hours (1.5 times 4 hours) of compensatory time off. When used, the comp time is paid at the regular rate of pay.

Most state and local government employees may accrue up to 240 hours of comp time. Law enforcement, fire protection, and emergency response personnel, as well as employees engaged in seasonal activities (such as employees processing state tax returns) may accrue up to 480 hours of comp time. An employee must be permitted to use comp time on the date requested unless doing so would “unduly disrupt” the operations of the agency.

When employees reach these ceilings, any additional overtime that is worked must be paid. FLSA compensatory time off stays on the books until the employee uses the time or until it is paid out. Employees cannot "use or lose" compensatory time off.

For answers to other questions on the Fair Labor Standards Act or the Family and Medical Leave Act, contact your nearest U.S. Department of Labor, Wage and Hour office: Indianapolis: (317) 226-6801; South Bend: (574) 236-8331.

The State Board of Accounts hopes all public officials will avoid any situations whereby conflict of interest becomes a question. Due to their position of public trust, public servants should be extremely sensitive to any transactions that may cause concern of the taxpayers that either elected them or caused them to be appointed to or employed in a public office. ]

Please seek the written advice of your township attorney if you have any questions relating to IC 35-44.1-1-4. The Uniform Conflict of Interest Disclosure Statement can be found Gateway.

CONFLICT OF INTEREST STATEMENT REQUIREMENT WHEN TRUSTEE IS ALSO VENDOR TO RECIPIENT RECEIVING TOWNSHIP ASSISTANCE

Instances may arise in which a township trustee may be legally eligible under IC 12-20 to be the direct payee as a vendor of a township resident requesting township assistance through the trustee’s office. Our audit position is that a conflict of interest disclosure is to be filed when the trustee is the direct payee as a vendor of township assistance under IC 12-20. A township trustee that benefits from township assistance received by a township assistance applicant may be requested to repay the township the amount of the benefits received if there has not been proper disclosure of the conflict of interest. We also recommend maintaining a separate file with a copy of the conflict of interest disclosure and the supporting documentation for the township assistance payments.

Per IC 35-44.1-1-4(b) “A public servant who knowingly or intentionally: (1) has a pecuniary interest or (2) derives a profit from; a contract or purchase connected with an action by the governmental entity served by the public servant commits conflict of interest, a Level 6 felony.” A “pecuniary interest” means an interest in a contract or purchase if the contract or purchase will result or is intended to result in an ascertainable increase in the income or net worth of: the public servant; or dependent of the public servant who: is under the direct or indirect administrative control of the public servant; or receives a contract or purchase order that is reviewed, approved, or directly or indirectly administered by the public servant.

IC 35-44.1-1-4(c) “It is not and offense under this section if any of the following apply: ...(6) A public servant makes a disclosure that meets the requirements of subsection (d) or (e) and is: (A) not a member or on the staff of the governing body empowered to contract or purchase on behalf of the governmental entity, and functions and performs duties for the governmental entity unrelated to the contract or purchase; (B) appointed by an elected public servant; (C) employed by the governing body of a school corporation and the contract or purchase involves the employment of a dependent or the payment of fees to a dependent; (D) elected; or (E) a member of, or a person appointed by, the board of trustees of a state supported college or university.

The conflict of interest disclosure must: (1) be in writing; (2) describe the contract or purchase to be made by the governmental entity; (3) describe the pecuniary interest that the public servant has in the contract or purchase; (4) be affirmed under penalty of perjury; (5) be submitted to the governmental entity and be accepted by the governmental entity in a public meeting of the governmental entity before final action on the contract or purchase; (6) be filed within fifteen (15) days after final action on the contract or purchase with: (A) the state board of accounts; and (B) if the governmental entity other than the state or a state supported college or university, the clerk of the circuit court in the county where the governmental entity takes final action on the contract or purchase; and (7) contain, if the public servant is appointed, the written approval of the elected public servant (if any) or the board of trustees of a state supported college or university (if any) that appointed the public servant.

Persons required to file the Conflict of Interest Disclosure with the State Board of Accounts can use the form available at https://forms.in.gov/Download.aspx?id=8264. Once the form has been completed, scan it as a pdf and upload at https://gateway.ifionline.org/sboa_coi/.

Each township board shall adopt a contracting policy that includes, at a minimum, the requirements set forth in IC 36-1-21. The policy may include requirements that are more stringent or detailed. These policies should be retained locally. There is no requirement that a new policy be adopted annually.

When completing the Certified Report of Names, Addresses, Duties and Compensation of Public Employees (Form 100R), the trustee must indicate if a contracting policy has been implemented. If a policy has not been implemented, the Department of Local Government Finance may not approve the township's budget or any additional appropriations for the township. If the township board implements a contracting policy after the trustee has completed the Form 100R, the trustee should send an email to sboaannualreports@sboa.in.gov and ask for the report to be unlocked. After the report is unlocked, the trustee should go back into the report and indicate that a policy has been adopted. The trustee must submit the report again in order for this change to be effective.

IC 36-1-21-4 states: "(a) This chapter establishes minimum requirements regarding contracting with a unit. The legislative body of the unit shall adopt a policy that includes, at a minimum, the requirements set forth in this chapter. However, the policy may:

- include requirements that are more stringent or detailed than any provision in this chapter; and

- apply to individuals who are exempted or excluded from the application of this chapter.

The unit may prohibit or restrict an individual from entering into a contract with the unit that is not otherwise prohibited or restricted by this chapter.

(b) The annual report filed by a unit with the state board of accounts under IC 5-11-13-1 must include a statement by the executive of the unit stating whether the unit has implemented a policy under this chapter."

IC 36-1-21-7 states: "If the state board of accounts finds that a unit has not implemented a policy under this chapter, the state board of accounts shall forward the information to the department of local government finance."

IC 36-1-21-8 states: "If a unit has not implemented a policy under this chapter, the department of local government finance may not approve:

- the unit's budget; or

- any additional appropriations

for the unit; for the ensuing calendar year until the state board of accounts certifies to the department of local government finance that the unit has adopted a policy under this chapter."

BUILDING OR REMODELING AND FIRE EQUIPMENT FUND (CUMULATIVE FIRE)

IC 36-8-14 authorizes townships to provide a cumulative fire fund for the purchase, construction, renovation, or addition to buildings or purchase of land used by the fire department or the volunteer fire department serving the unit and for the purchase of firefighting equipment, for use of the fire department or the volunteer fire department serving the unit including making the required payments under a lease rental with option to purchase agreement made to acquire the equipment. The fund may also be used for the purchase, construction, renovation or addition to a building or the purchase of land or purchase of equipment for use of a provider of emergency medical services under IC 16-31-5 to the township establishing the fund.

IC 36-8-14 limits the tax levy to no more than three and thirty – three hundredths cents ($0.0333) on each one hundred dollars ($100) of assessed valuation in the taxing district. Any tax collected after establishing the tax levy shall be deposited in a special fund to be known as the "Building or remodeling and fire equipment fund." Expenditures may be made only after an appropriation has been made available.

Any questions regarding procedures to establish the fund should be directed to the Department of Local Government Finance, Indiana Government Center North, Room N-1058B, 100 N. Senate, Indianapolis, IN 46204.

REPORTING CYBERSECURITY INCIDENTS

House Enrolled Act 1169 (2021) added IC 4-13.1-2-9 as a new section to the Indiana Code which requires political subdivisions, as defined in IC 36-1-2-13, to report any cybersecurity incident using their best professional judgement to the Indiana Office of Technology (IOT) without unreasonable delay and not later than two business days after discovery of the cybersecurity incident. A cybersecurity incident may consist of one or more of the following categories of attack vectors: (1) Ransomware, (2) Business email compromise, (3) Vulnerability Exploitation, (4) Zero-day exploitation, (5) Distributed denial of service, (6) Web site defacement, (7) Other sophisticated attacks as defined by the chief of information officer and that are posted on the officer’s Internet web site. (IC 4-13.1-1-1.5)

Cybersecurity incidents can be reported on IOT’s web site at the following webpage. https://www.in.gov/cybersecurity/report-a-cyber-crime/

- D

Data Processing Services by a Bank

Disaster Relief Funds - Accounting and Budgeting

Disposition of Old Outstanding Checks

DATA PROCESSING SERVICES BY A BANK

The Indiana Attorney General, in Official Opinion No. 46 of 1966, included the following provisions and conclusions in response to an inquiry concerning a contract between a county hospital and the data processing center of a bank (other than its duly designated depository) for the preparation and use of the bank’s official checks for payroll purposes:

1. Contracts entered into must be in writing. Further, it becomes difficult to conceive how the State Board of Accounts could properly consider and approve accounting systems and procedures established by an oral contract.

2. Accounting forms and procedures established in contracts entered into between banks and local Officials must be approved by the State Board of Accounts by using the form approval process noted under section ‘F’ on this page.

3. Contracts of the nature pursuant to the Opinion need not be bid.

4. Officials and board members are required to be made parties to the contract.

5. The local officials and their sureties are liable for misfeasance by the bank or its employees in handling the accounts. The bank constitutes an agent for the official. The official cannot delegate responsibility when he delegates duties.

6. A bank or trust company is not required to be a depository selected under the Public Depository Act for the officers for whom it is acting.

7. In substance, the bank is acting as a local official in performing his duties. Its work belongs to the public. The checks issued by the bank, signed by it, and drawn on its funds belong to the public and the original must be turned over to the local official in his official capacity. (However, please see below.)

All canceled checks must be returned by the bank to the township. IC 5-15-6-3 states in part “. . . ‘original records’ includes the optical image of a check . . .” The State Board of Accounts is of the audit position both sides of a check are part of the original record. Therefore, both sides of an “optical imaged check” should be available for public inspection and audit. Encoding, printing or bank certification should exist to ascertain that the back side of a check is part of a particular check, ie, endorsements belong to the front side of a check presented.

The contract may provide that the township shall draw a check or checks to the contracting bank and the bank in turn will write checks on its own funds for and on behalf of the township. The funds to pay any checks outstanding and not cashed for a period of time may remain with the funds of the bank until such time as they are to be returned to the township.

On a few occasions we have found that a township has entered into an agreement with data processing centers other than the data processing center of a bank. If such an agreement is for writing checks, such checks must be on township forms, for the signature of the township and drawn on the bank account of the township.

We have received inquiries concerning designating an acting Trustee under certain circumstances.

The State Board of Accounts is of the audit position that IC 36-6-4-18 provides "(a) Within thirty (30) days after taking office, the executive shall designate a person who shall perform the executive's duties whenever the executive is incapable of performing the executive's functions because the executive: (1) is absent from the township; or (2) becomes incapacitated. The executive shall give notice of the designation to the chairman of the township legislative body, the county sheriff, and any other persons that the executive chooses. The designee shall have all the powers of the executive. The executive is responsible for all acts of the designee. The executive may change the designee under this section at any time."

"(b) The designee shall perform the executive's duties until: (1) the executive is no longer absent from the township; or (2) an acting executive is appointed by the county executive under section 16 of this chapter."

We have not received any Official Opinions of the Attorney General of the State of Indiana which would indicate that a trustee could appoint a current township board member to serve as acting trustee in a township. Potential constitutional conflicts could exist concerning the holding of two (2) lucrative offices. However, Official Opinion Number 87-22 issued November 18, 1987 of the Attorney General of the State of Indiana discussed the possibility of designating another trustee and provides: "It is, therefore, my Official Opinion that a township trustee may appoint or designate pursuant to Public Law 105-1986 (HEA 1374), a township trustee of another township to act for him while he is absent from the township or while he is incapacitated. However, if any compensation is paid to the designee for the performance of the duties of the appointing township trustee, there may be a violation of Article 2, § 9 of the Constitution of Indiana." Therefore, we are of the audit position townships should consider appointing someone who is a resident of the township not currently holding another lucrative office. Examples might be the previous township trustee, previous board members, or a current clerk in the office. Finally, we are of the audit position that we are not aware of any provision for payment of compensation to an individual designated in accordance with IC 36-6-4-18.

DISASTER RELIEF FUNDS – ACCOUNTING AND BUDGETING

Based upon language contained in IC 10-14-3-17(j)(5) which states that a political subdivision may waive procedures and formalities otherwise required by law pertaining to the appropriation and expenditure of public funds where a national disaster or security emergency has been declared, the following procedures should be followed when disaster relief funds are received.

Money received or expected to be received form the Federal Emergency Management Agency (FEMA), the State Emergency Management Agency, or the State Lottery Commission for tornado, flood, ice storm, or other types of declared disasters should be accounted for in the following manner:

- If the money is to be used to reimburse funds for expenditures already incurred and paid and the conditions of IC 10-14-3-12 have been met, the amount received may be added back to the appropriation balances from which the expenditures have been previously made.

- If the money is to be used for future expenditures, a separate fund should be set up entitled “Disaster Relief Fund.” Such fund would not require appropriation or additional appropriation prior to spending the money in the fund.

It is recommended that all related expenditures records (claims, minutes, correspondence, contracts, damage survey report, etc.) be maintained in a separate file for future audits required by State and Federal agencies.

DISPOSITION OF OLD OUTSTANDING CHECKS

Pursuant to IC 5-11-10.5, all checks outstanding and unpaid for a period of two years as of December 31 of each are void.

Not later than March 1 of each year, the trustee shall prepare or cause to be prepared a list in duplicate of all checks outstanding for two or more years as of December 31 last preceding year. The original copy shall be filed with the board of finance of the township and the duplicate copy maintained by the trustee.

The trustee shall enter the amounts so listed as a receipt to the fund or funds upon which they were originally drawn and remove the checks from the list of outstanding checks. If the fund on which the checks were originally drawn is not in existence, or cannot be ascertained, the amount of such checks shall be receipted to the township fund.

Each list prepared must show:

- the date of issue of each check;

- the fund upon which the check was originally drawn;

- the name of the payee;

- the amount of each check issued; and

- the total amount represented by the checks listed for each fund.

IC 5-11-10.5-6 formerly provided for the issuance of another check to replace a canceled check, if a claim was properly filed by the vendor or the person to whom the check was issued within seven years after the date of issuance of the original check. The check would have been drawn upon the fund to which the canceled check was receipted and any check outstanding for more than seven years was to be considered void, and no recovery could be made. However, IC 5-11-10.5-6 was repealed in 1999. Therefore, we suggest the township attorney provide written guidance concerning claims that might be presented.

Following is the audit position of the State Board of Accounts concerning townships receiving donations.

- Restricted donations are defined as those to which the donor has attached terms, conditions, and/or purposes.

- Unrestricted donations are defined as those to which the donor has not attached terms, conditions, or purposes.

- The township has the option to accept or reject both restricted and/or unrestricted donations. Approval shall be obtained prior to accepting a donation.

- The Attorney General held in Official Opinion 68 of 1961 that no appropriation is necessary to expend monies donated for a specific purpose by a donor.

- Restricted donations should be receipted into a separate fund and properly titled. Such fund should not be commingled with other funds within the accounting system. An exception would be concerning statutory requirements; i.e., expenditures related to fire protection are required to be from the Firefighting Fund, etc.

- Expenditures may be made for the purpose(s) restricted without appropriation.

- Unrestricted donations should be receipted into the township fund and must be appropriated prior to subsequent expenditure.

TOWNSHIP ASSISTANCE - DONATIONS

It has been our position to not take audit exception to minimal donations received by the Township, for Township Assistance purposes, being receipted into the Township Assistance fund. If donations are not accounted for in a separate fund, then the funds received would assume the characteristics of the Township Assistance fund and shall be used for Township Assistance as provided by IC 12-20 after the funds have been properly appropriated. A township receiving substantial donations would require township officials to consider the impact that their accounting procedures would have on the tax levy of the fund. Any substantial donations are to be accounted for in a separate fund to ensure property tax levies are appropriate and in compliance with any donor restrictions.

- E

Elected Officials - Leave Policy

Electronic Payment of Vendor Claims

Examination of Records and Statement of Engagement Cost

Jury duty is considered to be a civic responsibility which should not be evaded by public employees.

IC 33-37-10-1 states in part "(a) A juror of a circuit, superior, county, or probate court or a member of a grand jury is entitled to the sum of the following: (1) Except as provided in subsection (f), an amount for mileage at the mileage rate paid to state officers and employees for each mile necessarily traveled to and from the court. (2) Payment at the rate of: (A) fifteen dollars ($15) for each day the juror is in actual attendance in court until the jury is impaneled; and (B) forty dollars ($40) for each day the juror is in actual attendance after impaneling and until the jury is discharged. (b) A county fiscal body may adopt an ordinance to pay from county funds a supplemental fee in addition to the fees prescribed by subsection (a)(2). (c) A juror of a city or town court is entitled to the sum of the following: (1) Except as provided in subsection (f), an amount for mileage at the mileage rate paid to state officers and employees for each mile necessarily traveled to and from the court. (2) Fifteen dollars ($15) per day while the juror is in actual attendance. (d) A city or town fiscal body may adopt an ordinance to pay from city or town funds a supplemental fee in addition to the fee prescribed by subsection (c)(2)."

We are of the audit position that a township may pay an employee the difference between the amount of jury duty pay per day to that employee and the amount of a regular day’s pay for that employee as if the employee had worked a regular day (no overtime). The following audit position applies to all employees for which the daily rate is greater than the daily amount paid for jury duty.

- A township employee could receive the full amount of regular salary and not claim compensation for jury duty.

- A township employee could receive the compensation for jury duty and said amount could be deducted from the regular salary.

- A township employee could receive the full amount of regular salary (no overtime) and turn over the warrant for serving on the jury to your office to be receipted into the fund from which the regular salary is paid.

Travel reimbursement belongs to the employee without being considered compensation for purposes of our audit position. We suggest that the trustee and the township board adopt a policy establishing rules and regulations for jury duty by township employees.

ELECTED OFFICIALS – LEAVE POLICY

We have received questions concerning the authority (or need) for elected officials to be included in the township's vacation leave, sick leave, death leave, or other such leave policy.

Our audit position is that an elected official's compensation goes with the office. This means that the elected official receives his (or her) salary as long as the office to which the official was elected performs the duties and responsibilities of this office. Whether the elected official personally does the work, whether the elected official personally maintains office hours, or whether the elected official shows up at the office has no bearing on the official's right to be compensated. Keep in mind this relates only to elected officials. The ghost employee statute, IC 35-44.1-1-3, prohibits payment to other township employees if they did not properly perform township duties assigned and maintain hours as directed by the township board.

In those few instances where elected officials choose to be included in such employee benefit policy (and were included in the authorizing resolution), the officials must maintain proper attendance records (the same as all other township employees) which shall clearly disclose days worked, days missed, type of leave taken, etc. This decision certainly cannot be made just prior to the close of the official's term. A township board is authorized to grant "a vacation with pay, sick leave, paid holidays, and other similar benefits by ordinance" to "employees of the political subdivision" pursuant to IC 5-10-6-1. The term "employees" is not defined.

ELECTRONIC PAYMENT OF VENDOR CLAIMS

Indiana Code 36-1-8-11.5 allows for the governing body of a political subdivision to pass a resolution that allows the fiscal officer to pay claims by electronic funds transfer. The statue also requires compliance with all other requirements of claims payment. Indiana Code 5-11-10-1.6 provides the requirements and procedures to be completed prior to issuing a check. Most of those requirements involve prior approval of a claim and ensuring that bills/invoices have been reviewed. Therefore, we recommend that if a Township is going to make payments electronically, that they complete the claims approval requirements, and then work with their depository for a payment authorization process. Except for INPRS remittances as detailed in IC 5- 10.2-2-12.5, we would suggest not setting up automatic monthly payments or other instances where vendors are giving access to pull money from the Township’s bank account.

With the opening of a new budget year and a new set of ledgers, it is to the advantage of a township to review the unpaid purchase orders and contracts which remain on the ledgers as “encumbered.”

Those items under purchase order or contract are to be added for each appropriation account and the total carried to the new yearly corresponding account. The actual unpaid amount of the purchase orders or contracts should be totaled and shown as a separate amount on the appropriation ledger sheet for the new year, with proper explanation, and added to the new year’s appropriation for the same purpose. By properly carrying out this procedure, the new year’s budget will not be expected to stand any expense not anticipated in making the budget. We suggest the trustee make a listing of these encumbered items and make it part of the township board minutes.

E-1 ENTITY ANNUAL REPORT

Entities are defined as providers of goods, services, or other benefits that are maintained in whole or in part at public expense or supported in whole or in part by appropriations, public funds, or taxation. The definition does not include the state or municipalities but does include for-profit and not-for profit corporations, unincorporated associations and organizations and individuals.

Financial assistance is defined as payments received in the form of grants, subsidies, contributions, aid etc.

Entities are primarily nongovernmental organizations, many of which conduct their business as a not-for-profit corporation. By contract or other form of agreement, these entities provide a service or benefit to the public on behalf of and paid for by government.

IC 5-11-1-9 delegates the “oversight” responsibility of these entities to the State Board of Accounts. Specifically, the State Board of Accounts is to ensure that audits, in accordance with agency guidelines, are performed for all entities receiving financial assistance from state or local government sources. The State Board of Accounts is also required to establish a system of review, follow-up, and resolution of any findings of noncompliance identified during the audit process.

All entities receiving assistance from state and local government, involving federal or non-federal dollars are subject to audit by state law.

IC 5-11-1-9 requires and organization-wide audit of an entity when the public funds disbursed by that organization are equal to or greater than 50% of its total disbursements. The State Examiner may waive the audit requirement if the public funds disbursed are less the 50% of its disbursements or if public funds disbursed are at least 50% of total expenditures but public funds expended are less than $750,000.

Additionally, fee-for-service arrangements with governmental entities are required to be reported on the E-1 report per the Uniform Compliance Guidelines. It will be the determination of the State Board of Accounts and not the entity, as to whether the funding arrangement meets the definition of fee-for-service. Copies of the contracts and other information may be required to be submitted and will be reviewed to determine the proper categorization of funding.

Entities subject to the requirements of IC 5-11-1-9 are required to file an Entity Annual Report (E-1) with the State Board of Accounts annually. The submission is due within sixty days of the entity’s fiscal yearend.

When a township provides financial assistance to non-governmental entities, the township shall communicate the requirement for the entity to file an E-1 through Gateway within sixty days of the entity’s fiscal year-end. The entity may obtain additional information from the State Board of Accounts at notforprofit@sboa.in.gov .

EMERGENCY APPROPRIATIONS PROCEDURE

If the proper officers of any township determine the need for expenditure of more money in the current year than was provided for in the approved annual budget, the following is required:

(1) In all cases of additional appropriations the governing body must meet and determine that they desire to appropriate for the expenditure of more money than was appropriated in the annual budget. When this condition has been determined, notice must be given to taxpayers by publication and posting as required by IC 5-3-1-2(b). Said notice to taxpayers should be made as required by the Department of Local Government Finance.

(2) The governing body determines whether to proceed with the proposal. An approval may not be in excess of the amount advertised, but can be less than requested. The governing body must adopt a resolution of additional appropriations.

(3) If a township proposes an additional appropriation from a fund that receives property tax levied under IC 6-1.1, the additional appropriation must be reported to and approved by the Department of Local Government Finance. A township may make an additional appropriation without the approval of the Department of Local Government Finance if it is from a fund that does not receive property tax, however, those appropriations shall be reported to the Department of Local Government Finance.

After the public hearing, the proper officers of a township shall file a certified copy of the final proposal and any other relevant information to the Department of Local Government Finance.

(4) Upon receipt of the certified copy of a proposal for additional appropriations, the Department of Local Government Finance will, in not less than fifteen (15) days after it receives the certificate, determine (in writing) if sufficient funds are available or will be available. The Department of Local Government Finance shall limit the additional appropriation to revenues available or to be made available, which have not been previously appropriated.

(5) If the Department of Local Government Finance disapproves an additional appropriation under IC 6-1.1-18-5, the Department of Local Government Finance shall specify the reason for its disapproval on the determination sent to the township.

A township may request a reconsideration of a determination of the Department of Local Government Finance under this section by filing a written request for reconsideration. A request for reconsideration must: (1) be filed with the Department of Local Government Finance within fifteen (15) days of the receipt of the determination by the political subdivision; and (2) state with reasonable specificity the reason for the request. The Department of Local Government Finance must act on a request for reconsideration within fifteen (15) days of receiving the request.

EXAMNINATION OF RECORDS AND STATEMENT OF ENGAGEMENT COST

At the end of an audit engagement the State Board of Accounts sends a notice of Statement of Engagement Cost to each political subdivision, including the County. This statement details a summary of the engagement including the number of days spent on the audit, the daily/hourly rate, and any report processing fees. We would like to point out that this statement is not an invoice that is to be paid by the entities.

A separate invoice for payment of these audit costs will be sent to the County for payment in accordance with IC 5-11-4. Immediately upon receipt of the certified statement, the county auditor shall issue a warrant on the county treasurer payable to the treasurer of state out of the general fund of the county for the amount stated in the certificate. The county auditor shall reimburse the county general fund, except for the expense of examination and investigation of county offices, out of the money due the taxing units at the next semiannual settlement of the collection of taxes.

If the county reasonably believes or knows that it does not have on hand or will not have collected enough taxes by the next distribution date for a taxing unit included on the examination of records billing, then the county auditor will send the certified statement to the taxing unit. The taxing unit should then contact the State Board of Accounts for directions on paying for the cost of the examination directly to the State Board of Accounts, instead of using settlement. It is important that the cost be paid off prior to the next audit. If the audit costs, due the State Board of Accounts, are not paid prior to the subsequent audit, it impairs the independence of the State Board of Accounts. This will delay future audits.

As the amount of federal funding to local governments has increased so has the need for single audits and more frequent audits which has helped drive up audit costs. We are now beginning to see this result in semiannual tax distributions that are not sufficient to pay the audit costs. It is important to plan and budget accordingly for these costs. It might be beneficial once an examination of records has been completed for the taxing unit to go directly to the county auditor if sufficient taxes will not be collected to pay the estimated costs of the examination of records. Having this conversation before receiving the certified statement from the county auditor can prepare the taxing unit for the payment of these costs. You can discuss with your field examiner during the exit, how you may best meet the costs. This may involve the use of other funds such as Rainy Day or if there are ARPA funds remaining under the revenue loss category, those can also be used to pay audit costs. If you have questions after the exit, please feel free to reach out to your State Board of Accounts Director for further assistance in looking for funds that can pay the audit costs.

When determining how these costs will be paid, it is also important to plan for the next year. During this determination, take into consideration the amount of federal assistance that you have disbursed during the year. If you have expended $750,000 or more of federal awards (whether the award is direct or passed-through another entity) in a year the taxing unit is required to have a single audit conducted in accordance with the Federal Office of Management and Budget’s Uniform Guidance. Single audits require an annual audit. If your unit does not need a Single Audit, there may be a longer time between your examinations. Since these costs could become an annual expense for the taxing unit, future budgets would need to be adjusted for those costs.

- F

Filing of Annual Report and Vouchers in County Auditor’s Office

Firefighting Fund - Fees and Services Charges

Fire Protection Contracts with Volunteer Fire Departments

Fire Protection Territories (FPT)

FILING OF ANNUAL REPORT AND VOUCHERS IN THE COUNTY AUDITOR'S OFFICE

IC 36-6-6-9(a) requires the township board to meet on or before the third Tuesday after the first Monday in February of each year. At this meeting it shall consider and approve, in whole or in part, the annual report of the executive presented under IC 36-6-4-12.

IC 36-6-4-12(a) requires at the annual meeting of the township board under IC 36-6-6-9 the trustee shall present a complete report of all receipts and expenditures of the preceding calendar year, including the balance to the credit of each fund controlled by the trustee. Most trustees use the State Board of Account's Annual Financial Report required by IC 5-11-1-4 as the report required by IC 36-6-4-12(a) but it is not required.

IC 36-6-4-12(d) requires the trustee to file a copy of the report required by IC 36-6-4-12(a) and its accompanying vouchers, in the county auditor's office within ten (10) days after the township board's action under IC 36-6-6-9.

The township board may, for the benefit of the township, bring a civil action against the trustee if the trustee fails to file the report within ten (10) days after the township board's action. The township board may recover five dollars ($5) for each day beyond the time limit for filing the report, until the report is filed.

IC 36-6-4-13(a) requires that when the trustee prepares the annual report required by IC 36-6-4-12, the trustee shall also prepare, on forms prescribed by the state board of accounts, an abstract of receipts and expenditures. This prescribed abstract of receipts and expenditures is contained in the State Board of Account's Annual Financial Report required by IC 5-11-1-4.

IC 36-6-4-13(b) requires that within four (4) weeks after the third Tuesday following the first Monday in January, the trustee shall publish the abstract prescribed by IC 36-6-4-13(a) in accordance with IC 5-3-1. The abstract must state that a complete and detailed annual report and the accompanying vouchers showing the names of persons paid money by the township have been filed with the county auditor, and that the chairman of the township board has a copy of the report that is available for inspection by any taxpayer of the township.

IC 36-6-4-13(c) states that a trustee who fails to comply with IC 36-6-4-13 commits a Class C infraction.

IC 36-6-4-12(d) requires the filing of the report required by IC 36-6-4-12(a) and the vouchers in the county auditor's office within ten days of the meeting required by IC 36-6-6-9. For 2014, the last day for the meeting required by IC 36-6-6-9 shall be held by February 18, 2014 (on or before the third Tuesday after the first Monday in February) which would require the report and vouchers to be required with the county auditor's office by February 28, 2014. However, IC 36-6-4-13(b) requires the trustee to publish the abstract prescribed by IC 36-6-4-13(a) by February 18, 2014 (within four (4) weeks after the third Tuesday following the first Monday in January). The abstract must state that a complete and detailed annual report and the accompanying vouchers showing the names of persons paid money by the township have been filed with the county auditor.

TOWNSHIP FIREFIGHTING FUND - FEES AND SERVICE CHARGES

IC 36-8-13-4(e) requires all money received for a fee or service charge imposed by the township legislative body to be deposited in the township’s firefighting fund. IC 36-8-13-4.5(d) allows the township trustee to accept donations for the purpose of firefighting and emergency services and requires these donations to be receipted into the township firefighting fund.