Search for Keywords

- A

Accident Response Service Fees - Prohibition of

Advance Payment of Salaries Prohibited - Exceptions

Annual Financial Report Changes - Enhanced Regulatory

Appropriation of Cumulative Funds

Appropriation of Federal and State Funds

Appropriation Ordinances - Failure to Pass

Assistance to Public Health Nursing Association

Attorneys & Legal Research Assistants

Audit Costs Charged to Federal Grants

Audit Required in Certain Circumstances

Appropriations

ACCIDENT RESPONSE SERVICE FEES – PROHIBITION OF

IC 9-26-9-4 states that a political subdivision or law enforcement agency may not impose

or collect, or enter into a contract for the collection of, an accident response service fee from the driver of a motor vehicle or any other person involved in a motor vehicle accident.ADVANCE PAYMENTS OF SALARIES PROHIBITED – EXCEPTIONS

IC 5-7-3-1 states:

“(a) Public officers may not draw or receive their salaries in advance.

(b) This section does not prohibit a payment under IC 36-4-8-9.”IC 36-4-8-9 states:

“(a) One (1) to three (3) days before the vacation leave period of a city officer or employee

begins, the city may pay the officer or employee the amount of compensation the officer or

employee will earn while on vacation leave.(b) Compensation for services paid to a salaried city officer or employee pursuant to a fixed

schedule set forth in a written contract or salary ordinance shall not be construed as having

been paid in advance. Under such an arrangement, the city shall maintain records to verify that

actual work is performed for all salary paid.”IC 36-5-4-7 states:

“One (1) to three (3) days before the vacation leave period of a town officer or employee begins, the town may pay the officer or employee the amount of compensation the officer or employee will earn while on vacation leave.”

IC 5-3-1-3 provides that each city controller or city and town clerk-treasurer shall have published an annual report of the receipts and expenditures of such city or town within 60 days after the close of each

calendar year.IC 5-11-1-4 requires such reports to be filed electronically on the Gateway portal with the State Board of Accounts no later than sixty (60) days after the close of the year.

Fiscal Officers are no longer required to mail a signed hardcopy of the Attestation Statement of the State Board of Accounts. The Attestation Statement submitted electronically with the AFR is sufficient.

The Cash and Investments Combined Statement of the annual report is to be published one time in two newspapers unless there is only one newspaper in the city or town, in which case publication in the one newspaper is sufficient. If no newspaper is published in the city or town, then publication is to be made in a newspaper published in the county in which the city or town is located and that circulates within the city or town.

The Cash and Investments Combined statement to be advertised is located in the Annual Report Outputs section under Advertising Outputs.

The Department of Local Government Finance may not approve the budget or a supplemental appropriation of a city or town until the city or town files an annual report for the preceding calendar year.

APPROPRIATION OF CUMULATIVE FUNDS

Approval by the Department of Local Government Finance (DLGF) to establish a tax levy for any cumulative fund authorized by law does not carry with it the authority to expend such funds without appropriation.

Prior to obligating these funds, it will be necessary to secure an appropriation in the regular legal manner which requires advertising to the taxpayers and approval of the DLGF.

Specific questions related to the appropriation of cumulative funds should be addressed directly to DLGF at 317-232-3777

APPROPRIATIONS OF FEDERAL AND STATE FUNDS

When funds are provided by the federal government either directly to a city or town or through a state agency for any program or project, the following procedures should be followed:

Advance Grants. Advance grants should be handled as follows:

- Where funds are “advanced” directly to a city or town by the federal government for a specific purpose prior to making any disbursements by the city or town, the money should be placed in a separate project fund and disbursements subsequently made from that fund. No appropriation of the federal funds is required.

- Where federal funds are “advanced” to a city or town through a state agency or department with no state funds added thereto prior to making any distributions, the money should be placed in a separate project fund and subsequent disbursements made from that fund. No appropriation of the federal funds is required.

- Where federal funds are “advanced” to a city or town by a state agency or department and state funds are included along with the federal funds in one check or voucher and the funds are for a specific purpose, the money should be placed in a separate project fund and disbursements made from that fund. Appropriation(s) must be obtained for the combined total (i.e., federal and state) prior to any disbursement being made from that project fund.

Reimbursement Grants. Reimbursement grants should be handled as follows:

Where a federal or state grant provides for payments to be made directly to a city or town on a “reimbursement” basis after payment of expenses by the city or town, the entire amount of the federal or state reimbursement may be appropriated by the city or town council without using the additional appropriation procedures under IC 6-1.1-18-5, if the funds are provided or designated by the state or the federal government as a reimbursement of expenditures. (IC 6-1.1-18-7.5)

No separate fund for the project or program is required unless the terms of the grant require one.

APPROPRIATION ORDINANCES – FAILURE TO PASS

IC 6-1.1-17-5 provides that a town council must fix the budget tax rates and tax levy no later than November 1 each year.

IC 36-4-7-11 provides that a city legislative body must fix the budget tax rates and tax levy before November 2 of each.

If the budget, tax rate, and tax levy of the city or town are not fixed by the date required, the most recent annual appropriations and annual tax levy are continued for the ensuing budget year.

Questions concerning the appropriation ordinances should be directed to the Department of Local

Government Finance at 317-232-3777 or 888-739-9826.Depositories used by cities and towns must be approved as depositories for State funds.

[IC 5-13-6-1(d)]. The Indiana Board for Depositories' website contains the most recent listing of approved depositories. The list can be accessed at www.in.gov/tos/deposit/.ASSISTANCE TO PUBLIC HEALTH NURSING ASSOCIATION

IC 16-20-7 allows cities to appropriate money out of the general fund of the city to assist incorporated public health nursing associations, organized, and operated not-for-profit and solely for the promotion of public health and suppression of disease, in carrying on the work of the public health nursing associations within the city.

The amount appropriated may not exceed the amount that could be collected from annually levying a tax of one and sixty-seven hundredths cents ($0.0167) on each one hundred dollars ($100) valuation of taxable property in the city.

We recommend that if a city assists such organizations that a contract be entered into that lists the services to be provided.

IC 7.1-4-9 requires all license fees paid in connection with the issuance of a beer retailer's permit, a beer dealer's permit, a liquor retailer's permit, a supplemental caterer's permit, a liquor dealer's permit, a wine retailer's permit and a wine dealer's permit that are received by the Alcohol and Tobacco Commission are to be deposited with the treasurer of state for deposit into an excise fund. Thirty-three percent (33%) of the moneys in the excise fund shall be paid into the general fund of the treasury of the city or town in which the retailer's or dealer's licensed premises are located and shall be budgeted according to law.

Distribution of the ATC Excise Tax shall be made by the auditor of state semiannually on the first day of June and first day of December of each year.

IC 7.1-4-7 requires the Alcohol and Tobacco Commission to deposit four cents ($0.04) of the beer excise tax collected on each gallon of beer or flavored malt beverage; one dollar ($1) of the liquor excise tax collected on each gallon of liquor; twenty cents ($0.20) of the wine excise tax collected on each gallon of wine; the entire amount of malt excise tax collected, and the entire amount of hard cider excise tax collected into the state general fund for distribution to the state (50%) and cities and towns (50%).

The sum set aside for cities and towns shall be allocated to a city or town based upon the basis that the population of the city or town bears to the total population of all cities and towns of the state.

The auditor of state shall, on the first day of April of each year and quarterly thereafter, distribute these amounts to the general fund of the treasury of the city or town.

ATTORNEYS AND LEGAL RESEARCH ASSISTANTS – CITY CLERKS AND CITY AND TOWN CLERK-TREASURERS

IC 36-4-10-5.5 and IC 36-5-6-8 state that a Clerk or Clerk-Treasurer may hire or contract with competent attorneys or legal research assistants on terms the Clerk or Clerk-Treasurer considers appropriate. Appropriations for salaries of attorneys and legal on research assistants employed shall be approved in the annual budget and must be allocated to the Clerk or Clerk-Treasurer for payment of attorneys and legal research assistant’s salaries.

Furthermore, IC 36-4-10-5.5 states that employment of an attorney by a City Clerk or City Clerk Treasurer does not affect a city department of law established under IC 36-4-4.

RECORDING OF AUDIT COSTS

Inquiries have questioned the correct procedure for accounting for city and town audit costs (this does not apply to costs associated with the utility audit).Indiana Code 5-11-4-3(b) guides this process and states, in part:

“… Immediately upon receipt of the certified statement, the county auditor shall issue a warrant on the county treasurer payable to the treasurer of state out of the general fund of the county for the amount stated in the certificate. The county auditor shall reimburse the county general fund, except for the expense of examination and investigation of county office, out of the money due the taxing units at the next semiannual settlement of the collection of taxes.”

Therefore, counties shall continue to forward Examination of Records (audit costs) payments to the Treasurer of State for city and town audits when billed by the State Board of Accounts. The county general fund shall then be reimbursed from property tax collections of the city or town at the next semiannual settlement.

To properly account for the city or town’s audit costs (not audit costs associated with the utility audit) the full amount of property and excise taxes (before audit costs) are to be receipted to the appropriate city or town funds. A disbursement for the Examination of Records is to be posted to city or town funds.

The Statement of Engagement Costs should be compared to the amount withheld for the Examination of Records to ensure the amounts agree. IC 5-11-4-4 provides that all disbursing offices are authorized to make payments required under this chapter without appropriation. Therefore, the examination of records costs would be considered an unappropriated disbursement.

AUDIT COSTS CHARGED TO FEDERAL GRANTS

If you receive Federal grants/awards that SBOA audits in accordance with the Office of Management and Budget’s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (commonly called "Uniform Guidance"), a portion of the associated audit costs may be allocated to some or all grants.

Title 2 of the U.S. Code of Federal Regulations, Part 200, Section 200.425 states:

Ҥ200.425 Audit services.

(a) A reasonably proportionate share of the costs of audits required by, and performed in accordance with, the Single Audit Act Amendments of 1996 (31 U.S.C. 7501-7507), as implemented by requirements of this part, are allowable. However, the following audit costs are unallowable:

(1) Any costs when audits required by the Single Audit Act and Subpart F—Audit Requirements of this part have not been conducted or have been conducted but not in accordance therewith; and

(2) Any costs of auditing a non-Federal entity that is exempted from having an audit conducted under the Single Audit Act and Subpart F—Audit Requirements of this part because its expenditures under Federal awards are less than $750,000 during the nonFederal entity's fiscal year.

(b) The costs of a financial statement audit of a non-Federal entity that does not currently have a Federal award may be included in the indirect cost pool for a cost allocation plan or indirect cost proposal.

(c) Pass-through entities may charge Federal awards for the cost of agreed-upon-procedures engagements to monitor subrecipients (in accordance with Subpart D—Post Federal Award Requirements of this part, §§200.330 Subrecipient and contractor determinations through 200.332 Fixed Amount Subawards) who are exempted from the requirements of the Single Audit Act and Subpart F—Audit Requirements of this part. This cost is allowable only if the agreed-upon-procedures engagements are:

(1) Conducted in accordance with GAGAS attestation standards;

(2) Paid for and arranged by the pass-through entity; and

(3) Limited in scope to one or more of the following types of compliance requirements: activities allowed or unhallowed; allowable costs/cost principles; eligibility; and reporting.

We would recommend checking with your grantor agency or agencies during the grant application process to see if any audit costs would be allowable for your specific grants. If allowed, a portion of audit costs may be able to be included into the budget for the grant.

AUDIT REQUIRED IN CERTAIN CIRCUMSTANCES

A city or town that requires an annual audit because of (a) the receipt of federal financial assistance in an amount that subjects the city/town to an annual federal audit, (b) continuing disclosure requirements, or (c) as a condition of a public bond issuance, shall provide notice to the State Examiner not later than 60 days after the close of the fiscal year that the city or town is required to have an annual audit. [IC 5-11-1-25(c)(2)]

APPROPRIATION OF INSURANCE CLAIM PROCEEDS - LIMITATIONS

Indiana Code 6-1.1-18-7 sets forth the procedure that shall be observed when appropriating funds received from a person to replace property, including insurance claim proceeds:

“Notwithstanding the other provisions of this chapter, the fiscal officer of a political subdivision may appropriate funds received from a person (as defined in IC 6-1.1-1-10) if:

(1) the funds are received as a result of damage to property of the political subdivision; and

(2) the funds are appropriated for the purpose of repairing or replacing the damaged property.

However, this section applies only if the funds are in fact expended to repair or replace the property within the twelve (12) month period after they are received.”

Where appropriations are made for such funds received from a person to replace property, including insurance claim proceeds, the appropriations need not be advertised nor approved by the Department of Local Government Finance. The fiscal officer may add the amount appropriated to the current appropriation account from which the expense will be paid.

- B

Bank Deposits By Remote Capture

Board of Public Works and Safety

Bonds of Officers and Employees of the Department of Parks and Recreation

Bonds Forfeited - City and Town Courts

Under prior law (IC 19-7-26), a common council of a city or a town council of a town could make annual appropriations for the purpose of maintaining and employing bands and orchestras to furnish music in public places and parks. Since this statute was repealed in 1981, a city or town should use the following when appropriating money for bands and orchestras.

The audit position of the State Board of Accounts is that if local units wish to provide bands and orchestras they should:

- follow the provisions of IC 36-1-3, the Home Rule statute;

- cite IC 36-10-2-2 and IC 36-10-2-4 in the home rule ordinance enacted; and

- follow the provisions of the ordinance and the cited statutes.

By doing this, cities and towns would not be subjected to exception in our audit reports. IC 36-10-2-2 states:

“A unit may establish, aid, maintain, and operate public parks, playgrounds, and recreation facilities and programs. IC 36-10-2-4 states: “A unit may establish, aid, maintain, and operate libraries and museums, cultural, historical and scientific facilities and programs, and community restitution or service facilities and programs.”

BANK DEPOSITS BY REMOTE CAPTURE

A governmental unit contacted us recently to report that a warrant had cleared their bank account two years ago and then cleared the bank a second time in 2016. From the information we were provided, when the original check was issued two years ago, the citizen receiving the check used a remote capture feature to deposit the check into his personal account – similar to taking a picture with his phone and his bank processed the transaction. In 2016, the citizen found the original paper check from two years ago and did not remember depositing it before. So the citizen took the paper check to the bank and deposited it. The bank processed the check and the transaction again cleared the governmental unit’s bank account. When the unit discovered this check cleared the bank a second time, they contacted the bank and requested their account be reimbursed. The bank reported that they were not liable for the check clearing twice.

We checked with the Treasurer of State’s office and they confirmed that the bank is not responsible if a check clears the bank more than once. The Treasurer of State’s office recommended using positive pay procedures with the local unit’s bank account to prevent such occurrences in the future. If a check does clear the bank twice, the governmental unit would have to pursue collection against the check payee to recover their funds.

With new technology where an individual can use their smartphone to remote deposit checks as well as the increase in remote capture by various vendors, this has become a more prevalent problem. Each unit should have controls in place to safeguard their accounts. Positive pay procedures for warrants, electronic funds transfers, or wire transfers, along with careful monitoring of the unit’s daily bank transactions, would help to mitigate this risk. If you have any questions or concerns regarding this occurring with your bank account, we’d recommend you contact your bank and discuss what options are available. The above information was emailed to local officials in a memo from the State Examiner dated April 29, 2016.

BARRETT LAW FUNDS – OFFICIAL BOND

IC 36-9-37-7 provides that the collecting and disbursing officer of Barrett Law funds in a city or town shall give a separate official bond in an amount to be fixed by the city or town council of such city or town pursuant to the provisions of IC 5-4-1-18(c). Said bond shall be filed and recorded in the office of the county recorder, as required by IC 5-4-1-5.1.

According to IC 5-4-1-18, the fiscal body shall fix the amount of the bond of Barrett Law fund custodians at an amount equal to thirty thousand dollars ($30,000) for each one million dollars ($1,000,000) of receipts of the officer's office during the last complete fiscal year before the purchase of the bond. The amount may not be less than thirty thousand dollars ($30,000) nor more than three hundred thousand dollars ($300,000) unless the fiscal body approves a greater amount for the officer or employee.

BOARD OF PUBLIC WORKS AND SAFETY - SECOND CLASS CITIES

The board of public works and safety may be composed of three (3) members or five (5) members appointed by the executive. A member may hold other appointive positions in city government during the member’s tenure. The executive shall appoint a clerk for the board.

If the board of public works and board of public safety are established as separate boards, each board may be composed of three (3) members or five (5) members who are appointed by the executive. A member may hold other appointive positions in city government during the member’s tenure. The executive shall appoint a clerk for each board.

If the executive:

(1) Increases the number of members of a board of public works and safety, a board of public works, or a board of public safety from three (3) to five (5) members; or

(2) Decreases the number of members of a board of public works and safety, a board of public works, or a board of public safety from five (5) to three (3) members; The city shall publish notice under IC 5-3-1 of the increase or decrease in members and state the total number of members appointed to the board. [IC 36-4-9-6]

BOARD OF PUBLIC WORKS AND SAFETY – THIRD CLASS CITIES

The board of public works and safety consists of three (3) or five (5) members (as determined by executive). The members of the board of public works and safety are:

(1) the city executive; and

(2) two (2) or four (4) persons appointed by the executive.

If the executive increases the number of board members from three (3) to five (5) members or decreases the number of board members from five (5) to three (3) members, the city shall publish notice under IC 5-3-1 of the increase or decrease in members and state the total number of members appointed to the board. IC 36-4-4-2 notwithstanding, a member may hold other appointive or elective positions in city government during the member’s tenure. The city clerk is the clerk of the board.

If the city legislative body adopts an ordinance under IC 36-4-12 to employ a city manager, the executive may appoint the city manager to a position on the board of public works and safety in place of the executive.

The city executive may appoint a public safety director to:

(1) serve as the chief administrative officer of; and

(2) oversee the operations of; the police department and fire department. The city executive shall determine the qualifications of the public safety director. (IC 36-4-9-8)

BONDS OF OFFICERS AND EMPLOYEES OF THE DEPARTMENT OF PARKS AND RECREATION

IC 36-10-3-16 lists the bonding requirements for officers and employees of a department of parks and recreation.

"a. Every officer and employee who handles money in the performance of duties as prescribed by this chapter shall execute an official bond for the term of office or employment before entering upon the duties of the office or employment.

b. The fiscal body of the unit may, under IC 5-4-1-18, authorize a blanket bond or crime insurance policy endorsed to include faithful performance to cover all officers' and employees' faithful performance of duties. The amount of the bond or crime insurance policy shall be fixed by the fiscal body and, in the case of a municipality, must be approved by the executive.

c. All official bonds shall be filed and recorded in the office of the county recorder of the county in which the department is located."

IC 5-1-15 authorizes cities and towns to issue “bonds, notes, evidences of indebtedness, or other written obligations” in fully registered or book entry form.

The entity may employ any bank or trust company as paying agent or registrar, co-registrar, or depository institution. The bank or trust company need not be a depository bank under IC 5-13, and need not be located within the State of Indiana.

Notwithstanding any other provision of law, registrars or registration books or transfer records for bonds, notes, evidence of indebtedness, or other written obligations of any entity are not public records, but are only for the use of the entity, any trustee, fiduciary, paying agent, registrar, co-registrar, or transfer agent. A trust department of a bank having possession of these records shall not disclose them to a bond department, commercial department, subsidiary of the bank, or a subsidiary of the parent corporation of the bank. (IC 5-1-15-5)

Registrars of bond issues shall keep a register of ownership of bonds. (IC 5-1-15-6) In an effort to facilitate accounting procedures, the State Board of Accounts has issued the following instructions:

1. If a bank, trust company, or other financial institution has been employed as a paying agent or registrar, a properly certified listing of bondholders from the paying agent or registrar shall serve as a mailing list for the fiscal officer. There is no requirement for each individual bondholder to file a claim.

2. The mailing of the funds for bonds and coupons coming due must be mailed in such a manner to ensure receipt by the bondholder by the due date specific. Personnel of financial institutions state they usually make such mailing by first class mail one to three business days in advance of the due date. They do not mail by certified or registered mail due to costs involved. We suggest you review this with your city or town attorney.

3. Since the paying agency or the registrar shall keep a register of ownership of bonds and all bonds and coupons shall be paid when becoming due, we see no reason for the municipality to duplicate those same records maintained by the paying agent or registrar by keeping a bond register. There should be no unpaid outstanding matured bonds or coupons.

4. In all instances when employing a bank, trust company, or other financial institutions, be sure to protect the municipality from any liability arising due to any possible errors relating to names and addresses of current bondholders. This protection may be obtained by the financial institution furnishing a bond or insurance in favor of the municipality.

As stated previously, please consult your city or town attorney with questions regarding procedures for registered bonds.

FORFEITED BONDS - CITY AND TOWN COURTS

IC 35-33-8-7 provides that if a defendant was admitted to bail under IC 35-33-8-3.2(a)(2) and has failed to appear before the court as ordered the court shall declare the bond forfeited not earlier than one hundred twenty (120) days or more than 365 days after the defendant’s failure to appear and issue a warrant for the defendant’s arrest.

In a criminal case, if the court having jurisdiction over the criminal case receives written notice of a pending civil action or unsatisfied judgment against the criminal defendant arising out of the same transaction or occurrence forming the basis of the criminal case, funds deposited with the clerk of the court under IC 35-33-8-3.2(a)(2) may not be declared forfeited by the court, and the court shall order the deposited funds to be held by the clerk. If there is an entry of final judgment in favor of the plaintiff in the civil action, and if the deposit and the bond are subject to forfeiture, the criminal court shall order payment of all or any part of the deposit to the plaintiff in the action, as is necessary to satisfy the judgment. The court shall then order the remainder of the deposit, if any, and the bond forfeited.

Any proceedings concerning the bond, or its forfeiture, judgment, or execution of judgment, shall be held in the court that admitted the defendant to bail.

After a bond has been forfeited, the clerk shall mail notice of forfeiture to the defendant. In addition, unless the court finds that there was justification for the defendant’s failure to appear, the court shall immediately enter judgment, without pleadings and without change of judge or change of venue, against the defendant for the amount of the bail bond, and the clerk shall record the judgment.

If a bond is forfeited and the court has entered a judgment, the clerk shall transfer to the state common school fund:

(1) any amount remaining on deposit with the court (less the fees retained by the clerk); and

(2) any amount collected in satisfaction of the judgment.

The clerk shall return a deposit, less the administrative fee, made under IC 35-33-8-3.2(a)(2) to the defendant, if the defendant appeared at trial and the other critical stages of the legal proceedings.

The amount transferred to the State Common School Fund shall be sent to the county auditor on a monthly basis as Bond Forfeitures.

Since there is no statutory requirement that building permit fees be placed in a separate fund, we believe that such fees should be receipted to the General Fund and disbursements for compensation of building inspectors, the cost of building permit forms, and other such expenses should be paid from the General Fund and charged against appropriations properly made therefore.

The following procedures shall be followed if a municipality wishes to obtain an appropriation and make expenditures for buy money or payments to informants:

1. Under IC 36-1-3 an ordinance shall be passed allowing this type of program and associated expenditures;

2. An appropriation for such purpose must be obtained in the manner authorized by state statutes;

3. Petty cash fund procedures are to be followed as authorized by IC 36-1-8-3; and

4. A minimum documentation procedure must be followed, similar to either:

A. “Guidelines for the Expenditure of Confidential Funds,” published by the U.S. Department of Criminal Justice.

B. “Guidelines for Obtaining and Accounting for Confidential Funds Used in Support of Criminal Investigations,” (Revised S.O.P. PR – INV-0017), by the Indiana State Police Department

- C

Cancellation or Rejection of Bids

Certified Report of Names, Addresses, Duties, and Compensation of Public Employees

Child Restraint System Penalties

City and Town Courts - Judgments on Overweight Vehicles

Claims for Payments to State and Federal Agencies

Clerk Treasurer's Notary Powers

Compensation - Employee Time off for Jury Duty or as Subpoenaed Witness

Construction of Sidewalks - Funds and Appropriations

Contracts for Collection or Disposal of Solid Waste

Contributions, Donations, Gifts

County Slot Machine Wagering Fees

Cumulative Capital Development Fund

Cumulative Capital Improvement Fund - Uses (Cigarette Tax)

Cumulative Capital Improvement Fund

Cumulative Firefighting, Building, and Equipment and Police Radio Fund

Cybersecurity Incidents - Reporting

CAPITAL ASSETS – CEMETERIES

City or Town owned cemeteries are considered capital assets and need to be properly recorded on General Form 369 – Capital Assets Ledger. The cemeteries are to be reported on General Form 369 – Capital Assets Ledger at the actual or estimated historical cost based on appraisals or deflated current replacement cost. Contributed or donated assets are reported at estimated fair value at the time received.

An article was published in the June 2019 Cities and Towns Bulletin (Page 27) to assist in determining the estimated historical cost of the capital asset when the actual cost of the capital asset is not known.

General Form 369 – Capital Assets Ledger does not have a separate classification for cemeteries, so the cemetery ground will be recorded on the capital asset ledger under land, any structures on the cemetery grounds under buildings, and roads and drainage systems will be recorded under infrastructure. There will be no effect on the value of the asset as plots are sold. The purchase of a burial plot is a real estate transaction; however, cemetery plot deeds grant burial rights that create an easement for the specific purpose of burial but do not alter the municipality’s ownership of the cemetery as a whole.

Each city or town is required to adopt a capital asset policy that details the threshold at which an item is considered a capital asset. A complete physical inventory must be taken at least every two years, unless more stringent requirements exist, to verify account balances carried in the accounting records.CANCELLATION OR REJECTIONS OF BIDS

IC 5-22-18-2 states that when the purchasing agency determines it is in the best interests of the governmental body:

1. A solicitation may be canceled; or

2. Offers may be rejected; in whole or in part as specified in the solicitation. IC 5-22-7-2 requires this statement to be included in an invitation for bids.

The reason for a cancellation of a solicitation or rejection of offers must be made part of the contract file.

REPORT OF NAMES, ADDRESSES, DUTIES, AND COMPENSATION OF PUBLIC EMPLOYEES

All cities and towns must file with the State Examiner on or before January 31, Form 100-R, a Certified Report of Names, Addresses, Duties and Compensation of Public Employees. This report is required by IC 5-11-13. Only the business address of each officer or employee listed is to be included on the form.

Such report must indicate whether the city or town offers a health plan, a pension, and other benefits to full-time and part-time employees. In addition, as a part of the report, each city or town must upload a copy of the policies adopted under IC 36-1-20.2 (Nepotism) and IC 36-1-21 (Contracting).

The report is to be filed electronically on the Gateway portal with the State Board of Accounts. The Attestation Statement must be signed by the official and mailed within five days of submission on Gateway.

The Department of Local Government Finance may not approve a city or town's budget or any additional appropriations for the ensuing calendar year unless such report is filed and the Nepotism and Contracting policies have been implemented.

IC 20-33-3 places certain restrictions on work hours for children under 18 years old. For questions regarding child labor laws, please contact the Indiana Department of Labor. The Bureau of Child Labor home page is located at https://www.in.gov/dol/childlabor.htm. The preferred contact information is childlabor@dol.in.gov.

IC 20-33-3-39 through IC 20-33-3-41 list the penalties for violations of the child employment laws which can be as high as $400 per violation.

CHILD RESTRAINT SYSTEM PENALTIES

All Class D infraction collections for violations of the child restraint laws under IC 9-19-11 are to be accounted for separately by each city or town court as child restraint system fees. Such fees are to be remitted by the clerk of a city or town court to the county auditor on a monthly basis.

IC 31-16-15-16 requires employers that employ more than fifty (50) employees and that withhold child support from more than one (1) obligor to make payments to the State Central Collection Unit through electronic funds transfer or through electronic or internet access made available by the state central collection unit.

Additional information is available on the Indiana State Central Collection Unit website at www.insccu.com.

CITY AND TOWN COURTS – JUDGMENTS ON OVERWEIGHT VEHICLES

Infraction judgments levied for overweight vehicles should be accounted for in the following manner:

1. All overweight infraction judgments shall be indicated separately as “Overweight Vehicle Fines” on City or Town Form No. 214, City/Town Court Receipt.

2. The receipts shall be posted as “Overweight Vehicle Fines” on City and Town Form No. 213, City/Town Court Cash Book.

3. Monthly, the total of all overweight infraction judgments shall be transmitted to the County Auditor (along with state fines and forfeitures) on City and Town Form No. 217, Report to County Auditor of Fines and Forfeitures Collect in City/Town Court. The total overweight infraction judgments shall be indicated separately on the transmittal as “Overweight Vehicle Fines.” They should not be included as State Fines and Forfeitures.

4. The County Auditor shall quietus the collections reported by the Clerk of the City/Town Court to a separate fund entitled “Overweight Vehicle Fines.” Such collections shall be transmitted to the Auditor of State.

5. Pursuant to IC 9-20-18-12, the Auditor of State will deposit such judgments into the State Highway Fund.

CLAIMS FOR PAYMENTS TO STATE AND FEDERAL AGENCIES

The State Board of Accounts’ audit position is that when statutory payments are due to state or federal agencies, there is no requirement for the state or federal agency to file an invoice or claim for such payments. This audit position would include payments for social security obligations, public employees’ retirement fund contributions, federal, state, or county taxes withheld, sales tax, utility receipts tax, and other such amounts due state or federal agencies.

The disbursing officer should prepare an accounts payable voucher and attach any copies of payroll deduction reports, federal or state invoices, communications, etc., to document the payment. The accounts payable voucher will provide a posting media indicating to whom paid, fund on which drawn, accounts to be charged, and the approval by the proper boards.

CLERK-TREASURER’S NOTARY POWERS

Notaries public, judges of courts, in their respective jurisdictions, mayors, clerks and clerktreasurers of towns and cities, in their respective towns and cities, clerks of circuit courts, master commissioners, in their respective counties, judges of United States district courts of Indiana, in their respective jurisdictions, and United States commissioners appointed for any United States district court of Indiana, in their respective jurisdictions, are authorized to administer oaths and take acknowledgments generally, pertaining to all matters where an oath is required.

Since it appears IC 33-42-9 grants clerks and clerk-treasurers virtually identical powers and authority as notaries public in matters involving acknowledgements and oaths, there would be no need for a clerk or clerk-treasurer to qualify as a notary public.

COMPENSATION – EMPLOYEE TIME OFF FOR JURY DUTY OR AS SUBPOENAED WITNESS

Since there are not any statutory references applying to these situations, the following is the audit position of the State Board of Accounts. Any of the following procedures would be acceptable:

1. The employee could receive the full amount of his/her regular salary and not claim compensation for serving as a juror or a witness.

2. The employee could receive the compensation for serving as a juror or witness and the amount received (excluding mileage reimbursement) could be deducted from his/her regular salary.

3. The employee could receive the full amount of his/her regular salary and then, in turn, turn over the warrant received for serving as a juror or witness to the proper fiscal officer. The fiscal officer would receipt the warrant into the fund from which the regular salary was paid. This procedure would not permit the appropriation to be increased by the amount of the receipt. (This procedure will not be possible if any mileage reimbursement is included in the warrant).

Following is a listing of funds and appropriations from which costs of constructing sidewalks

adjacent to city and town streets may be paid.- Current appropriation in the city or town general fund;

- Voluntary contributions from property owners;

- Current appropriation of proceeds from a general obligation bond issue which will be retired over a period of years by general taxation;

- Current appropriation in the (Municipal) Cumulative Capital Development Fund if approved as one of the fund purposes (IC 36-9-15.5);

- Current appropriation in the Cumulative Capital Improvement Fund (tax levy) [IC 36-9-16];

- Current appropriation in the Cumulative Capital Improvement Fund (cigarette taxes) [IC 6-7-1-31.1];

- Current appropriation in the Cumulative Street Fund (IC 36-9-16.5);

- Special assessment under the General Improvement Fund (IC 36-9-17);

- Special assessment under the Municipal and County Barrett Law Fund (IC 36-9-36);

- Special assessment under the Municipal Barrett Law Fund (IC 36-9-37);

- Barrett Law Revolving Fund established pursuant to IC 36-9-37-46;

- Special Assessment under the Municipal Improvement District Law (IC 36-9-38);

- Current appropriation in the Motor Vehicle Highway Fund (IC 8-14-1-5 and Attorney General Official Opinion No. 64 dated November 22, 1965); and

- Current appropriation in the Local Road and Street Fund (IC 8-14-2-5, IC 9-13-2-167, and Attorney General Official Opinion No. 64 dated November 22, 1965).

CONTRACTS FOR COLLECTION OR DISPOSAL OF SOLID WASTE

A city or town may:

(1) Contract with persons for the collection or disposal of solid waste. The contract may provide that persons contracted with have the exclusive right to collect or dispose of solid waste under IC 36-9-30-4.

(2) Contract with any business or institution for the collection and disposal of industrial, commercial, or institutional sold waste. All fees collected by the city or town shall be deposited in the treasury of the city or town for the administration, operation, and maintenance of the solid waste collection and disposal project.

(3) Contract for the use of privately owned solid waste disposal facilities. If a contract executed under (1) or (2) will yield a gross revenue to a contractor (other than a governmental entity) of at least twenty-five thousand dollars ($25,000) during the time it is in effect, then the city or town must comply with IC 36-1-12-4 in awarding the contract. The city or town shall require the bidder to submit a financial statement, a statement of experience, the bidder’s proposed plan or plans for performing the contract, and the equipment that the bidder has available for the performance of the contract. The statement shall be submitted on forms prescribed by the State Board of Accounts. However, the requirements in IC 36-1-12-4(b)(6) do not apply. A city of town may contract with private persons that operate facilities that combine significant elements of recycling or production of refuse derived fuel. [IC 36-9-30-5]

CONTRIBUTIONS, DONATIONS, GIFTS

Following is a brief list of procedures to be followed by city and town officials in receiving and accounting for monetary contributions, donations, or gifts received by the municipality. (The term "donation" in this article includes donations, contributions and gifts.)

1. Unrestricted donations are defined as those to which the donor has not attached terms, conditions, or purposes.

2. Restricted donations are defined as those to which the donor has attached terms, conditions, or purposes.

3. The governing body of the unit has the option and responsibility to either accept or reject, in writing, any proposed donation.

4. If the donation is a restricted donation, the board must agree, in writing, to the terms, conditions, or purposes attached to the proposed donation.

5. Restricted donations can only be accepted for purposes within the scope of general statutory authority.

6. Income or revenues in the form of tax distributions, tax receipts, fees, rentals, contractual payments, etc., are not to be considered donations.

7. Donations which are accepted must be handled in one of the two following methods:

A. Unrestricted donations shall be receipted into the applicable operating fund of the unit (i.e. city or town operating (general) fund; cemetery operating fund, park and recreation operating fund, airport operating fund, etc.). Expenditure of such donated revenue from the operating fund shall be made only after an appropriation has been provided for the purpose of the expenditure. Claims must be filed and approved in the regular legal manner.

B. A restricted donation shall be placed into a separate fund after such fund is established by the legislative body of the unit. Any appropriate descriptive name may be given the donation fund. The donation can be expended only for the purpose and under the terms and conditions agreed to on accepting the donation.

Pursuant to Attorney General Official Opinion No. 68 of 1961, no further appropriation is required for expenditure of a restricted donation for the designated purpose. Even though no further appropriation is required, claims must be filed and approved in the regular legal manner before disbursements can be made from the fund.

8. If the volume of restricted donations justifies it, a "control" fund may be established for all restricted donations. Separate, individual accounts would then be established to account for each restricted donation or each type of restricted donation. The total activities of the separate accounts -- receipts disbursements, balances – should be reflected on the control fund.

9. Income from investments of restricted donations should be receipted into the same fund in which the principal of the donation has been receipted, provided it is to be used for the same purpose as the principal. However, if under the terms of the trust, the principal must be held in trust in perpetuity and only the income used by the governmental unit, there should be two funds established. One fund should be designated as "trust interest." In this situation, expenditures would only be permitted from the Trust Interest (Income) Fund".

10. The municipality's fiscal officer should be the custodian of the unit's funds and securities.

The fee for copying documents may not exceed the greater of: (1) ten cents per page for copies that are not color copies and twenty-five cents per page for color copies; or (2) the actual cost of copying the document. Actual cost means the cost of paper and the per page cost for use of copying or facsimile equipment and does not include labor costs or overhead costs. A fee established under this subsection must be uniform to all purchasers. (IC 5-14-3-8) These provisions do not apply to copies of accident reports under IC 9-26-9.

COUNTY SLOT MACHINE WAGERING FEES

In those counties (Madison and Shelby) with slot machine wagering at racetracks, a county slot machine wagering fee shall be collected by the State and distributed to each city or town in such counties by the County Auditor pursuant to IC 4-35-8.5-3. IC 4-35-8.5-4 requires such distributions to be deposited in the city or town’s general fund.

The State Board of Accounts will not take exception to the use of credit cards by a governmental unit provided the following criteria are observed:

1. The governing board must authorize credit card use through an ordinance or resolution, which has been approved in the minutes.

2. Issuance and use should be handled by an official or employee designated by the board.

3. The purposes for which the credit card may be used must be specifically stated in the ordinance or resolution.

4. When the purpose for which the credit card has been issued has been accomplished, the card should be returned to the custody of the responsible person.

5. The designated responsible official or employee should maintain an accounting system or log which would include the names of individuals requesting usage of the cards, their position, estimated amounts to be charged, fund and account numbers to be charged, date the card is issued and returned, etc.

6. Credit cards should not be used to bypass the accounting system. One reason that purchase orders are issued is to provide the fiscal officer with the means to encumber and track appropriations to provide the governing board and other officials with timely and accurate accounting information and monitoring of the accounting system.

7. Payment should not be made on the basis of the statement or a credit card slip only. Procedures for payments should be no different than for any other claim. Supporting documents such as paid bills and receipts must be available. Additionally, any interest or penalty incurred due to the late filing or furnishing of documentation by an officer or employee should be the responsibility of that officer or employee.

8. If properly authorized, an annual fee may be paid.

Local law enforcement agencies may, on request for release or inspection of a limited criminal history, do the following:

1. Require a form, provided by them, to be completed. The form shall be maintained for a period of two (2) years and shall be available to the record subject upon request.

2. Collect a three dollar ($3) fee to defray the cost of processing a request for inspection.

3. Collect a seven dollar ($7) fee to defray the cost of processing a request for release.

However, law enforcement agencies may not charge a fee for requests received from the parent locator service of the child support bureau of the Department of Child Services. Local law enforcement agencies shall edit information so that the only information released or inspected is information which has been requested and is limited criminal history information. (IC 10-13-3-30)

A local home rule ordinance would be required to enable a city or town law enforcement agency to collect such fees. All monies should be deposited in the municipality’s general fund unless otherwise stated in the ordinance.

IC 36-9-15.5 allows the legislative body of a municipality to, with the approval of the Department of Local Government Finance (DLGF), establish a cumulative capital development fund to provide money for any purpose for which property taxes may be imposed within the municipality under the authority of:

IC 8-16-3 (Cumulative Bridge Fund)

IC 8-22-3-25 (Cumulative Building Fund-Airports) IC 14-27-6-48 (Cumulative Building Fund-Levees)

IC 14-33-14 (Cumulative Maintenance Fund-Channel Improvement) IC 16-23-1-40 (Cumulative Hospital Building Fund)

IC 36-8-14 (Cumulative Firefighting Fund)

IC 36-9-4-48 (Cumulative Transportation Fund-Buses) IC 36-9-16-2 (Cumulative Building Fund)

IC 36-9-16-3 (Cumulative Capital Improvement Fund) IC 36-9-16.5 (Cumulative Street Fund)

IC 36-9-17 (General Improvement Fund)

IC 36-9-26 (Cumulative Building Fund-Sewers) IC 36-9-27-100 (Cumulative Drainage Fund)

IC 36-10-3-21 (Cumulative Building Fund-Parks) or

IC 36-10-4-36 (Cumulative Sinking and Building Fund-Parks)

A municipality that decides to establish a cumulative capital development fund must follow the procedures of IC 6-1.1-41.

The maximum property tax rate that may be imposed for property taxes first due and payable during a particular year in a municipality that is either wholly or partially located in a county in which the county option income tax or the county adjusted gross income tax is in effect on January 1 of that year depends upon the number of years the municipality has previously imposed a tax and is determined under the table provided in IC 36-9-15.5

The money collected shall be held in a special fund to be known as the cumulative capital development fund. Expenditures from the cumulative capital development fund may be made only after an appropriation made in the manner provided by law for making other appropriations. However, in a consolidated city, money may be transferred from the fund to the fund of a department of the consolidated city responsible for carrying out a purpose for which the cumulative capital development fund was created. The department may not expend any money so transferred until an appropriation is made and the department may not expend any money so transferred for operating costs of the department.

Money held in the cumulative capital development fund may be spent for purposes other than the purposes stated in IC 36-9-15.5-2, if the purpose is to protect the public health, welfare, or safety in an emergency situation that demands immediate action or to make a contribution to an authority established under IC 36-7-23. Money may be spent only after the executive of the municipality: (1) issues a declaration that the public health, welfare, or safety is in immediate danger that requires the expenditure of money in the fund; or (2) certifies in the minutes of the municipal legislative body that the contribution is made to the authority for capital development purposes.

CUMULATIVE CAPITAL IMPROVEMENT FUND (Cigarette Tax Distributions) - USES

IC 6-7-1-31.1 provides that the fiscal body of each city and the fiscal body of each town shall, by ordinance or resolution, establish a cumulative capital improvement fund for the city or town.

The list of permitted uses in IC 6-7-1-31.1 includes “(9) for any other governmental purpose for which money is appropriated by the fiscal body of the city or town.”

The money in the city’s or town’s cumulative capital improvement fund does not revert to its general fund.

A city or town may at any time, by ordinance or resolution, transfer to: (1) its general fund; or (2) an authority established under IC 36-7-23; money derived under this chapter that has been deposited in the city’s or town’s cumulative capital improvement fund.

The Attorney General in Official Opinion No. 15, dated May 25, 1965, held a city or town existing at the time of the last preceding U.S. decennial census continues to share in the cigarette tax distribution on this basis and not on the basis of any subsequent U.S. Census Bureau special census. Official Opinion No. 15 also states a city or town coming into existence after the last preceding U.S. decennial census is entitled to share in the cigarette tax distributions.

CUMULATIVE CAPITAL IMPROVEMENT FUND

IC 36-9-16-2 further authorizes the establishment of a cumulative capital improvement fund which can be used for the same purposes as the cumulative building fund as well as for the purchase of body armor for active members of a police department and any use permitted under IC 6-7-1-31.1, which includes the following:

(1) to purchase land, easement, or rights-of-way;

(2) to purchase buildings;

(3) to construct or improve city owned property;

(4) to design, develop, purchase, lease, upgrade, maintain, or repair:

(A) computer hardware;

(B) computer software;

(C) wiring and computer networks; and

(D) communications access systems used to connect with computer networks or electronic gateways;

(5) to pay for the services of full-time or part-time computer maintenance employees;

(6) to conduct nonrecurring in-service technology training of unit employees;

(7) to undertake Internet application development;

(8) to retire general obligation bonds issued by the city or town for one (1) of the purposes stated in subdivision (1), (2), (3), (4), (5), or (6); or

(9) for any other governmental purpose for which money is appropriated by the fiscal body of the city or town.

In addition, IC 36-9-16-3 lists the following fourteen (14) additional purposes which cumulative capital improvement fund monies could be used for:

(1) To acquire land or rights-of-way to be used for public ways or sidewalks.

(2) To construct and maintain public ways or sidewalks.

(3) To acquire land or rights-of-way for the construction of sanitary or storm sewers, or both.

(4) To construct and maintain sanitary or storm sewers, or both.

(5) To acquire, by purchase or lease, or to pay all or part of the purchase price of a utility.

(6) To purchase or lease land, buildings, or rights-of-way for the use of any utility that is acquired or operated by the unit.

(7) To purchase or acquire land, with or without buildings, for park or recreation purposes.

(8) To purchase, lease, or pay all or part of the purchase price of motor vehicles for the use of any combination of the police, a community corrections program, or the fire department, including ambulances and firefighting vehicles with the necessary equipment, ladders, and hoses.

(9) To purchase, lease, or pay all or part of the cost of electronic monitoring equipment used by a state or local community corrections program.

(10) To retire in whole or in part any general obligation bonds of the unit that were issued for the purpose of acquiring or constructing improvements or properties that would qualify for the use of cumulative capital improvement funds.

(11) To purchase or lease equipment and other nonconsumable personal property needed by the unit for any public transportation use.

(12) In a county or a consolidated city, to purchase or lease equipment to be used to illuminate a public way or sidewalk.

(13) The fund may be used for any of the following purposes:

(A) To purchase, lease, upgrade, maintain, or repair one (1) or more of the following:

(i) Computer hardware.

(ii) Computer software.

(iii) Wiring and computer networks.

(iv) Communication access systems used to connect with computer networks or electronic gateways.

(B) To pay for the services of full-time or part-time computer maintenance employees.

(C) To conduct nonrecurring inservice technology training of unit employees.

(14) To purchase body armor (as defined in IC 35-47-5-13(a)) for active members of a police department under:

(A) IC 36-5-7-7;

(B) IC 36-8-4-4.5;

(C) IC 36-8-9-9; and

(D) IC 36-8-10-4.5.

Such fund should not be confused with the cumulative capital improvement fund which is funded by State cigarette tax distributions under IC 6-7-1.

CUMULATIVE FIREFIGHTING, BUILDING AND EQUIPMENT AND POLICE RADIO FUND

IC 36-8-14 authorizes cities and towns to provide a cumulative building and equipment fund for the purchase, construction, renovation, or addition to buildings, or the purchase of land used by the fire department and for the purchase of firefighting equipment, including making the required payments under a lease rental with option to purchase agreement made to acquire the equipment. A municipality may also use the fund to purchase police radio equipment. The fund may also be used for the purchase, construction, renovation or addition to a building, the purchase of land, or the purchase of equipment for use of a provider of emergency medical services under IC 16-31-5 to the city or town establishing the fund.

The statute limits the tax levy to no more than thirty-three hundredths cents ($0.0333) on each one hundred dollars ($100) of assessed valuation in the taxing district. Any tax collected after establishing this tax levy shall be deposited in a special fund to be known as the "building or remodeling, firefighting, and police radio equipment fund." This fund may not be used for any purpose other than the purpose for which it was raised. Expenditures may be made only after an appropriation has been made available.

Any questions regarding procedures to establish this fund should be directed to the Indiana Department of Local Government Finance, Indiana Government Center North, Room N1058, 100 N. Senate, Indianapolis, Indiana 46204.

REPORTING CYBERSECURITY INCIDENTS

House Enrolled Act 1169 (2021) added IC 4-13.1-2-9 as a new section to the Indiana Code which requires political subdivisions, as defined in IC 36-1-2-13, to report any cybersecurity incident using their best professional judgement to the Indiana Office of Technology (IOT) without unreasonable delay and not later than two business days after discovery of the cybersecurity incident. A cybersecurity incident may consist of one or more of the following categories of attack vectors: (1) Ransomware, (2) Business email compromise, (3) Vulnerability Exploitation, (4) Zero-day exploitation, (5) Distributed denial of service, (6) Web site defacement, (7) Other sophisticated attacks as defined by the chief of information officer and that are posted on the officer’s Internet web site. (IC 4-13.1-1-1.5)

Cybersecurity incidents can be reported on IOT’s web site at the following webpage. https://www.in.gov/cybersecurity/report-a-cyber-crime/

- D

Deferred Compensation Plans - PERF

Diptheria, Tetanus, and Rabies Vaccines

DEFERRED COMPENSATION PLANS – PUBLIC EMPLOYEES RETIREMENT FUND

IC 5-10-1.1-1 allows cities and towns to contribute amounts before January 1, 1995 and continue or begin to contribute amounts after January 1, 1995, to a nonqualified deferred compensation plan on behalf of eligible employees, subject to any limits and provisions under section 457 of the Internal Revenue Code. IC 5-10-1.1-7 allows cities and towns to offer to their employees both the state deferred compensation plan and another deferred compensation plan that uses private vendors.

IC 5-10.2-2-1 further provides that it does not prohibit a city or town from establishing and providing before January 1, 1995 and continuing to provide after January 1, 1995, retirement, disability, and survivor benefits to the employees of the city or town if the city or town took action before January 1, 1995, and was not a member of the Public Employees’ Retirement Fund (PERF) on January 1, 1995.

A city or town has no authority to establish a local pension plan by ordinance, resolution, or contract after January 1, 1995, without specific statutory authority. PERF, deferred compensation plans, police and fire pension plans, and utility employee pension plans are all authorized by statute.

DIPHTHERIA, TETANUS, AND RABIES VACCINES

IC 16-41-19-2 requires all cities and towns to supply without charge diphtheria, scarlet fever, and tetanus (lockjaw) antitoxin and rabies vaccine to persons financially unable to purchase the antitoxin or vaccine, upon the application of a licensed physician.

All costs that are incurred in furnishing the aforementioned antitoxin or vaccines shall be paid by the appropriate city or town against which a physician’s application form is issued from general funds not otherwise appropriated without appropriation.

An Application and Claim for Biologist, State Form No. 43918, will be filed by the physician with the city or town fiscal officer if such antitoxins or vaccines are supplied.

DISASTER RELIEF FUNDS – ACCOUNTING AND BUDGETING

Based upon language contained in IC 10-14-3-17(j)(5) which states that a political subdivision may waive procedures and formalities otherwise required by law pertaining to the appropriation and expenditure of public funds where a national disaster or security emergency has been declared, the following procedures should be followed when disaster relief funds are received.

Money received or expected to be received form the Federal Emergency Management Agency (FEMA), the State Emergency Management Agency, or the State Lottery Commission for tornado, flood, ice storm, or other types of declared disasters should be accounted for in the following manner:

1. If the money is to be used to reimburse funds for expenditures already incurred and paid and the conditions of IC 10-14-3-12 have been met, the amount received may be added back to the appropriation balances from which the expenditures have been previously made.

2. If the money is to be used for future expenditures, a separate fund should be set up entitled “Disaster Relief Fund.” Such fund would not require appropriation or additional appropriation prior to spending the money in the fund.

It is recommended that all related expenditures records (claims, minutes, correspondence, contracts, damage survey report, etc.) be maintained in a separate file for future audits required by State and Federal agencies.

- E

Establishing the Estimated Cost of Capital Assets

Examination of Records and Statement of Engagement Cost

The governing body of a city, town, township, or county by the governing body's action or in any combination may do the following:

1. Establish, operate, and maintain emergency medical services.

2. Levy taxes under and limited by IC 6-3.6 and expend appropriated funds of the political subdivision to pay the costs and expenses of establishing, operating, maintaining, or contracting for emergency medical services.

3. Except as provided in section 2 of this chapter, authorize, franchise, or contract for emergency medical services. However:

A. a county may not provide, authorize, or contract for emergency medical services within the limits of any city without the consent of the city; and

B. a city or town may not provide, authorize, franchise, or contract for emergency medical services outside the limits of the city or town without the approval of the governing body of the area to be served.

4. Apply for, receive, and accept gifts, bequests, grants-in-aid, state, federal, and local aid, and other forms of financial assistance for the support of emergency medical services.

5. Establish and provide for the collection of reasonable fees for emergency ambulance services the governing body provides under this chapter.

6. Pay the fees or dues for individual or group membership in any regularly organized volunteer emergency medical services association on their own behalf or on behalf of the emergency medical services personnel serving that unit of government. [IC 16-31-5-1]

A city, town, or county may not adopt an ordinance that restricts a person from providing emergency ambulance services in the city, town, township, or county if:

1. The person is authorized to provide emergency ambulance services in any part of another county; and

2. The person has been requested to provide emergency ambulance services:

A. To the county in which the person is authorized to provide emergency ambulance services, and those services will originate in another county; or

B. From the county in which the person is authorized to provide emergency ambulance services and those services will terminate in another county. (IC 16-31-5-2)

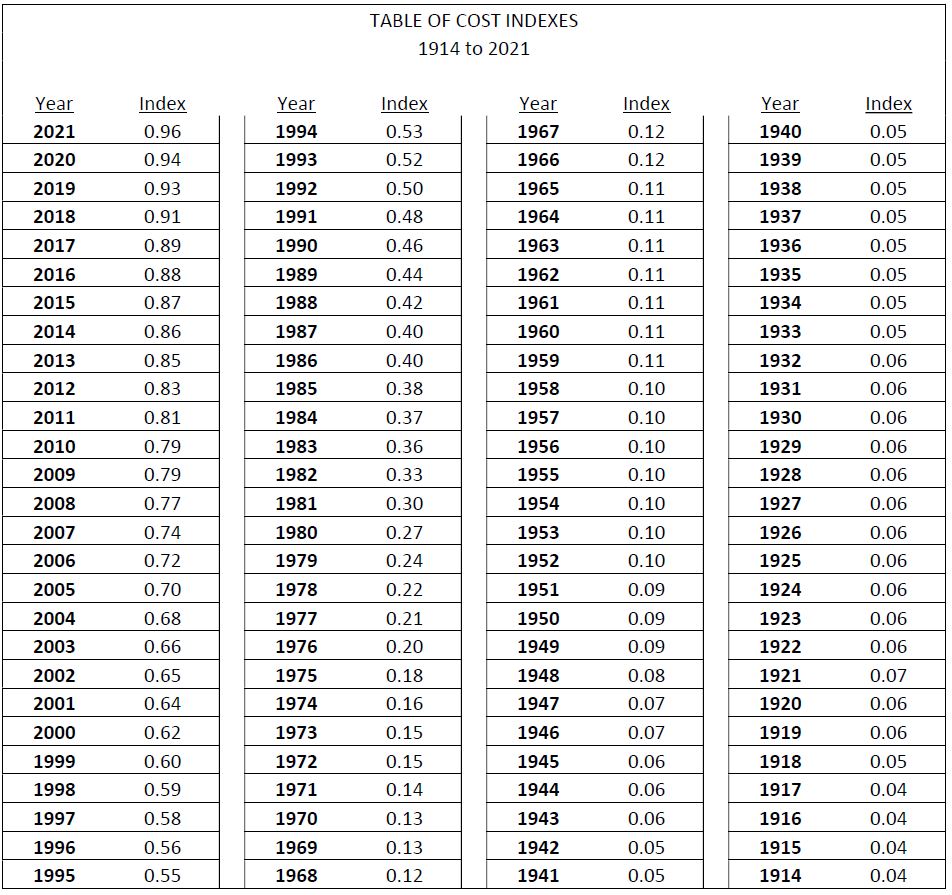

ESTABLISHING THE ESTIMATED COST OF CAPITAL ASSETS

When it is not possible to determine the historical cost of capital assets owned by a governmental unit, the following procedure should be followed.

Develop an inventory of all capital assets which are significant for which records of the historical costs are not available. Obtain an estimate of the replacement costs of these assets. Through inquiry determine the year or approximate year of acquisition. Then multiply the estimated replacement cost by the factor for the year of acquisition from the Table of Cost Indexes. The resulting amount will be the estimated cost of the asset.

In some cases estimated replacement cost can be obtained from insurance policies; however, if estimated replacement costs are not available from insurance policies, you should obtain or make an estimate of the replacement costs.

If the replacement cost is estimated to be $76,000.00 and the asset was constructed about 1930, then the estimated cost of the asset should be reported as $5,320.00.

$76,000.00 X .07 = $5,320.00

(See Table of Cost Indexes)

EXAMNINATION OF RECORDS AND STATEMENT OF ENGAGEMENT COST

At the end of an audit engagement the State Board of Accounts sends a notice of Statement of Engagement Cost to each political subdivision, including the County. This statement details a summary of the engagement including the number of days spent on the audit, the daily/hourly rate, and any report processing fees. We would like to point out that this statement is not an invoice that is to be paid by the entities.

A separate invoice for payment of these audit costs will be sent to the County for payment in accordance with IC 5-11-4. Immediately upon receipt of the certified statement, the county auditor shall issue a warrant on the county treasurer payable to the treasurer of state out of the general fund of the county for the amount stated in the certificate. The county auditor shall reimburse the county general fund, except for the expense of examination and investigation of county offices, out of the money due the taxing units at the next semiannual settlement of the collection of taxes.

If the county reasonably believes or knows that it does not have on hand or will not have collected enough taxes by the next distribution date for a taxing unit included on the examination of records billing, then the county auditor will send the certified statement to the taxing unit. The taxing unit should then contact the State Board of Accounts for directions on paying for the cost of the examination directly to the State Board of Accounts, instead of using settlement. It is important that the cost be paid off prior to the next audit. If the audit costs, due the State Board of Accounts, are not paid prior to the subsequent audit, it impairs the independence of the State Board of Accounts. This will delay future audits.

As the amount of federal funding to local governments has increased so has the need for single audits and more frequent audits which has helped drive up audit costs. We are now beginning to see this result in semiannual tax distributions that are not sufficient to pay the audit costs. It is important to plan and budget accordingly for these costs. It might be beneficial once an examination of records has been completed for the taxing unit to go directly to the county auditor if sufficient taxes will not be collected to pay the estimated costs of the examination of records. Having this conversation before receiving the certified statement from the county auditor can prepare the taxing unit for the payment of these costs. You can discuss with your field examiner during the exit, how you may best meet the costs. This may involve the use of other funds such as Rainy Day or if there are ARPA funds remaining under the revenue loss category, those can also be used to pay audit costs. If you have questions after the exit, please feel free to reach out to your State Board of Accounts Director for further assistance in looking for funds that can pay the audit costs.

When determining how these costs will be paid, it is also important to plan for the next year. During this determination, take into consideration the amount of federal assistance that you have disbursed during the year. If you have expended $750,000 or more of federal awards (whether the award is direct or passed-through another entity) in a year the taxing unit is required to have a single audit conducted in accordance with the Federal Office of Management and Budget’s Uniform Guidance. Single audits require an annual audit. If your unit does not need a Single Audit, there may be a longer time between your examinations. Since these costs could become an annual expense for the taxing unit, future budgets would need to be adjusted for those costs.

Expenses paid from utility funds should be directly related to the operation of the municipally owned utility. Expenditures for city and town operating costs should not be paid from utility funds. Furthermore, utility funds should not be used to pay for personal items. The cost of shared employees and equipment between a city or town and its utilities or between utilities should be prorated in a rational manner.

Establishment of a Cash Reserve Fund permits transfer of surplus utility funds to the city or town general fund. After appropriation, such transferred funds may then be used for any legal general fund purpose.

- F

Federal Assistance - Data Collection Form

Funding and Refunding Indebtedness

Currently, IC 5-14-3-8(d) authorizes the fiscal body to establish a fee schedule for the certification or copying of documents. Prior to July 1, 2007 this subsection allowed for the inclusion of a facsimile machine transmission fee. Effective July 1, 2007 the reference to the inclusion of a fee for facsimile machine transmission was deleted from this subsection and so it is our position that this subsection no longer supports such a fee.

IC 5-14-3-8(f) states in part:

"Notwithstanding subsection…(d)….. a public agency shall collect…. Facsimile machine transmission fee… that is specified by statute or is ordered by a court".

We are not aware of any statute that specifies a facsimile machine transmission fee.

Per State Court Administration, Trial Rule 81(A) does not allow for a standing court order for facsimile fees.

As to the amount of a facsimile machine transmission fee which a court may order on an individual basis, State Court Administration recommends that it should adopt a fee amount that is reasonable and substantially in conformance with those authorized by existing statutes. The parameters specified in IC 5-14-3-8(d) could be used as a guide. A court may decide that a reasonable facsimile fee may be so small as to not be worth collecting.

In an audit, if a facsimile machine transmission fee is collected we would look for either a specific statute authorizing the fee or a court order

FEDERAL ASSISTANCE – DATA COLLECTION FORM

Form SF-SAC, Data Collection Form for Reporting on Audits of States, Local Governments, Indian Tribes, Institutions of High Education, and Nonprofit Organizations is required to be filed with the Federal Audit Clearinghouse for all Single audits.

A part of our service, Field Examiners will complete the form at the time of audit. The fiscal officer will need to certify the form. Instructions on the certification process will be provided.

As a general rule, governmental units are exempt from any federal excise tax. To obtain an exemption, a properly executed exemption certificate must be filed with the vendor from whom the purchase is made. This exemption certificate may be prepared at the time the order is placed or at the time payment is made. The exemption certificate may be a printed or copied form and should be substantially in the form currently used. For information concerning the form of the exemption certificate, contact the Internal Revenue Service.

Claims and invoices should be carefully audited to see that no federal excise taxes are included and paid. Disbursing officers should require that invoices show separately the gross price, the amount of the excise tax, and the final price to the governmental unit.

In some instances, a city or town may have erroneously paid the excise taxes from which they are exempt. In such instances, the city or town has three years from the date the tax was paid to the Federal Government in which to file for a refund.

To obtain a refund, the city or town should submit to the seller an exemption certificate for each item on which excise tax was paid accompanied with documentary evidence that the exemption had not been claimed or received. Such evidence may be copies of invoices, affidavits, records, etc. The Internal Revenue Service will provide forms on which the original taxpayer may claim reimbursement for excise tax erroneously paid by a city or town.

Any questions concerning federal excise tax should be directed to the Internal Revenue Service.

FILING AND DOCKETING CLAIMS

Indiana Code 5-11-10-2 states in part:

“(a) Claims against a political subdivision of the state must be approved by the officer or person receiving the goods or services, be audited for correctness and approved by the disbursing officer of the political subdivision, and, where applicable, be allowed by the governing body having jurisdiction over allowance of such claims before they are paid. If the claim is against a governmental entity as defined in section 1.6 [IC 5-11-10-1.6] of this chapter, the claim must be certified by the fiscal officer.

(b) The state board of accounts shall prescribe a form which will permit claims from two (2) or more claimants to be listed on a single document and, when such list is signed by members of the governing body showing the claims and amounts allowed each claimant and the total claimed and allowed as listed on such document, it shall not be necessary for the members to sign each claim.

(c) Applies to solid waste management districts.

(d) The form prescribed under this section shall be prepared by or filed with the disbursing officer of the political subdivision together with… the supporting invoices or bills...

(e) Where under any law it is provided that each claim be allowed over the signatures of members of a governing body, or a claim docket or accounts payable voucher register be prepared listing claims to be considered for allowance, the form and procedure prescribed in this section shall be in lieu of the provisions of the other law.”

The State Board of Accounts has prescribed General Form No. 364, Accounts Payable Voucher Register, which shall be prepared by, or filed with, the disbursing officer of the city or town, together with the supporting accounts payable voucher, and all such documents shall be carefully preserved by the disbursing officer as a part of the official records of the office.

IC 36-4-8-5(a)(2) applies to cities and IC 36-5-4-4(a)(2) applies to towns. Both statutes require claims to be filed in the manner prescribed by IC 5-11-10-2 at least five (5) days before the meeting of the applicable approving body. However, if the city or town council has passed an ordinance to allow certain claims to be paid by the fiscal officer between board meetings in accordance with IC 36-4-8-14 (cities) or IC 36-5-4-12 (towns), then the five (5) day requirement does not apply for those particular types of claims.

If members of the governing body would rather approve and sign each individual accounts payable voucher in lieu of signing the Allowance of Vouchers section of General Form 364, this procedure is acceptable.

Indiana Code 5-11-10-1.6 states, in part:

“(c) The fiscal officer of a governmental entity may not draw a warrant or check for payment of a claim unless:

(1) there is a fully itemized invoice or bill for the claim;

(2) the invoice or bill is approved by the officer or person receiving the goods and services;

(3) the invoice or bill is filed with the governmental entity's fiscal officer;

(4) the fiscal officer audits and certifies before payment that the invoice or bill is true and correct; and

(5) payment of the claim is allowed by the governmental entity's legislative body or the board or official having jurisdiction over allowance of payment of the claim…(d) The fiscal officer of a governmental entity shall issue checks or warrants for claims by the governmental entity that meet all of the requirements of this section. The fiscal officer does not incur personal liability for disbursements: