Search for Keywords

Introduction

- Introduction

The Indiana State Board of Accounts is the state agency, designated by legislation, with responsibility of the audit of public funds received and disbursed by public offices and officers, state offices, state institutions, and any other entities receiving or disbursing public funds. Through the annual reporting process and our involvement in approving requests for proposals and audit contracts with private examiners to perform the audits of the charter schools, we have attempted to ensure charter schools subject to federal or state audit requirements have met these requirements as efficiently and inexpensively as possible.

It is the Indiana State Board of Accounts policy that units of government subject to the audit requirements of Indiana Code 5-11-1 shall have no more than one audit completed annually. Therefore, the auditor selected to perform the annual audit shall be required to complete the financial audit, the compliance audit, and, if applicable, an audit under Title 2 U.S. Code of Federal Regulations Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance) audit. It is therefore imperative that entities and their private examiner exercise diligence in determining applicable audit requirements, prior to commencing the audit process. Through adherence to our Guidelines for the Audits of Charter Schools Performed by Private Examiners (Guidelines), and with the cooperation of all parties involved, one audit can and will satisfy the needs of all interested parties. Subject to the Malfeasance, Misfeasance, and Nonfeasance section of the Guidelines, we reserve the right to audit, examine, investigate, and review records of any charter school at any time as deemed necessary by the State Examiner.

We would like to thank the charter schools and private examiners for the cooperation and assistance they provide. We hope this issue of the Guidelines will assist you in successfully addressing your responsibilities.

Paul D. Joyce, CPA

State Examiner - Guidelines for Audits

Audit Coordination and Administration

Audit Frequency and Completion

Request for Proposal and Contract Requirements

Required State Board of Accounts Language to be Included in the Engagement Letter

Auditing Standards to be Applied

Malfeasance, Misfeasance, or Nonfeasance

Indiana Code (IC) 20-24-8-5 states in part: "The following statutes and rules and guidelines adopted under the following statutes apply to a charter school: (1) IC 5-11-1-9 (required audits by the state board of accounts). . . ." Indiana Code at 5-11-1-9 gives the State Board of Accounts the responsibility for examining all accounts and all financial affairs of every public office and officer, state office, state institution, and entity disbursing public money. The State Examiner, in accordance with Indiana Code 5-11-1-7, may engage or allow private examiners to perform this examination. If so designated, the private examiner must follow the guidelines set out in this document.

If the State Examiner engages or authorizes the engagement of a private examiner to perform an examination under Indiana Code 5-11-1, the examination and report must comply with the uniform compliance guidelines established by the State Board of Accounts. If a person or entity subject to examination under this chapter engages a private examiner, the contract with the private examiner must require the examination and report to comply with the uniform compliance guidelines established (IC 5-11-1-24(d)). These guidelines may be viewed at our website: www.in.gov/sboa.

The state or a municipality, including charter schools, may not enter into a contract with an entity subject to examination under Indiana Code 5-11-1 if the contract does not permit the examinations and require the reports prescribed by this chapter (IC 5-11-1-24(d)) and contain the required elements outlined in the "Contract Requirements" section of these guidelines.

Audit Coordination and Administration

Audits may be performed by the State Board of Accounts or private examiners approved by the State Board of Accounts. Coordination of these audits with the State Board of Accounts is required. We, therefore, require the submission of all charter school audit contracts to us for approval, prior to signing.

The primary responsibility for ensuring the appropriateness, timeliness, and completeness of a charter school's audit rests with the charter school itself. However, successful completion of the audit process cannot be accomplished without the direct cooperation and assistance of funding agencies, private examiners, and the State Board of Accounts. Due to the complexity of government regulations and the uniqueness of existing arrangements and relationships between funding agencies and entities, it is imperative that charter schools and their private examiners confirm in advance, the type and scope of audit necessary to satisfy all parties involved. Audit costs are always the responsibility of the charter school.

Per Indiana Code 5-11-1-7, private examiners allowed engagements by the State Examiner are subject to the direction of the State Examiner. Private examiners allowed engagements for services under Indiana Code 5-11 are agents of the State Examiner and are limited to the following powers unless additional authority is granted in writing by the State Examiner.

Private examiners are entitled to examine any books, papers, documents, or electronically stored information for the purpose of making an examination. Private examiners are entitled access in the presence of the custodian or the custodian's deputy to the cash drawers and cash in the custody of the officer. Private examiners may during business hours, examine the public accounts in any depository that has public funds in its custody.

Indiana Code 5-11-5-1(d) requires a private examiner, acting as an agent of the State Examiner, who determines during an examination under Indiana Code 5-11 that (1) a substantial amount of public funds have been misappropriated or diverted and (2) that the private examiner has a reasonable belief that the malfeasance or misfeasance that resulted in the misappropriations or diversion of the public funds was committed by the officer or an employee of the office, to report the determination to the State Examiner. These reports shall be sent by email to charterschools@sboa.in.gov immediately upon the conclusion by the private examiner that these conditions have been met.

If a private examiner is experiencing difficulties in obtaining audit documents needed to complete the audit, communication and coordination with the State Board of Accounts must be made. The State Board of Accounts can utilize its subpoena authority to assist the private examiner in obtaining the documents needed to complete the audit. Delay in the completion of an audit should not be allowed to continue without notification to the State Board of Accounts. The State Board of Accounts will make the determination when to utilize a subpoena to compel the delivery of the documents needed.

Except as required by Indiana Code 5-11-5-1(b) and Indiana Code 5-11-5-1(d), it is unlawful for any private examiner, before an examination report is made public by the State Examiner's filing, to make any disclosure of the result of any examination of any public account, except to the State Examiner or if directed to give publicity to the examination report by the State Examiner or by any court.

Communication of audit status, findings, Audit Results and Comments, financial statements, and notes between the private examiner and charter school management (executive director and those running the charter school on a day-to-day basis), and governance (charter school board and organizer) is appropriate and necessary. It is important for the private examiner to remind management and governance that any discussions between the private examiner and management or governance is not public information or for public disclosure until the report has been filed and publicly released.

Audit Frequency and CompletionAudit frequency of charter schools is subject to requirements set forth by the Indiana Department of Education, the charter school's authorizer, the needs of the charter school, and in accordance with Indiana Code 5-11-1-25. In order to comply with U.S. Department of Education requirements for states that administer the federal Public Charter School Program (PCSP) grant, the Indiana Department of Education requires all Indiana charter schools to undergo an independent audit on an annual basis.

Audits performed by private examiners are to be completed and all required reports issued within 180 days after the close of the audit period. Any requests for an extension of time must be made by emailing the State Board of Accounts at charterschools@sboa.in.gov. The request shall include the reason an extension is needed and the amount of extra time being requested. Extensions may be granted by the State Board of Accounts for up to an additional 60 days. Requests for extension must be received no later than 30 days prior to the report deadline indicated above to be considered for approval. Extensions are not automatic; any request for an extension may be rejected by the State Board of Accounts. Any extension approval shall be in the form of a written response. Any charter school that does not have an audit completed and reports submitted by the deadline, or request an extension as indicated above, may have their audit completed by the State Board of Accounts, or by a private examiner selected by the State Board of Accounts. It will be the sole determination of the State Board of Accounts that an audit has not been engaged for timely in order to meet the deadline and will be performed by, or private examiner selected by, the State Board of Accounts to complete the audit. Audit costs are always the responsibility of the charter school.

Request for Proposal and Contract Requirements

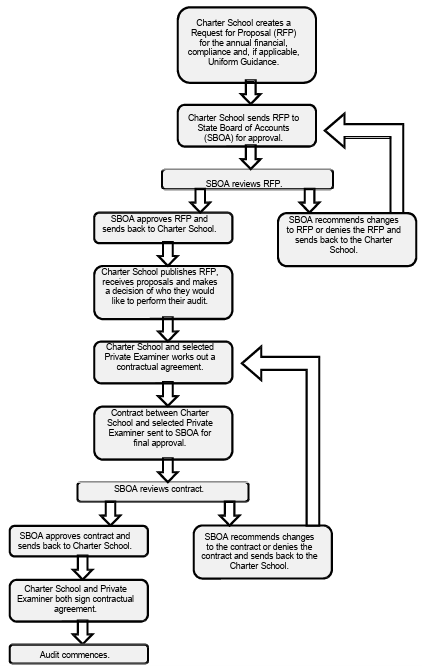

Per Indiana Code 5-11-1-24, the charter school may not request proposals for performing an examination unless the request for proposals has been submitted to and approved, by the State Board of Accounts. Request for proposals must contain at least the required wording for contracts stated below and shall be submitted by email to charterschools@sboa.in.gov.

The request for proposal must include all of the following:

To be considered for the audit services, the private examiner selected must meet the following qualifications:

Be a certified public accountant (CPA) and licensed to practice in the State of Indiana or have a CPA license from a state that has been determined to be in substantial equivalence with the CPA licensure requirements of the State of Indiana in accordance with Indiana Code 25-2.1-4-10(a);

1. Meet independence requirements of the American Institute of Certified Public Accountants (AICPA) and the Generally Accepted Government Auditing Standards (GAGAS) issued by the Comptroller General of the United States, as applicable;

2. If performing audits under GAGAS, meet continuing professional education requirements in accordance with Government Auditing Standards issued by the Comptroller General of the United States;

3. Obtain an external peer review at least once every three years and attain a rating of Pass, or Pass with Deficiencies;

4. Have no record of performing substandard audits;

5. Understand and comply with applicable uniform compliance guidelines, policies, and directives established by the State Board of Accounts;

6. Understand the role of the State Board of Accounts in the audit process and that the IPA is acting as an agent for the State Examiner;

Upon completion of our review of the request for proposal, we will issue a written approval or rejection of the request for proposal and our reason for any modifications or rejection.

If the charter school is using the same private examiner used in the prior audit, a request for proposal is not required unless the scope of the examination has changed. The examiner is still required to submit audit contracts and draft reports prior to audit finalization for our review.

To obtain approval for a private examiner to audit under Indiana Code 5-11, the audit contract must be submitted to the State Board of Accounts, prior to signing. Contracts with no reference to or acknowledgment of the responsibility of the State Board of Accounts in this process via reference to State Examiner Directive 2015-2 will be rejected. Similarly, contracts without the required State Board of Accounts additional language will be rejected.

The approval of the audit contract by the State Board of Accounts is not an assertion that the audit will satisfy federal funding agencies or other reporting requirements. The approval is based on limited knowledge of the overall audit requirements and is not to be used as a substitute for thorough planning by the private examiner and charter school. The State Examiner does not take any responsibility for the audit work completed by the private examiner or the opinion issued. We will work with the private examiner to provide appropriate audit services, but the ultimate responsibility for audit work remains with the private examiner.

Required State Board of Accounts language to be included in the Engagement Letter:1. We acknowledge the oversight responsibilities of the State Board of Accounts for the audits of charter schools. We will follow the minimum audit requirements and required compliance testing as presented in the "Guidelines for the Audit of Charter Schools Performed by Private Examiners" and the requirements of Directive 2015-2.

2. The State Examiner will be notified immediately if there is a misappropriation of funds that is suspected to be the result of malfeasance, misfeasance, or nonfeasance discovered during the course of the private examiner's work.

3. The State Examiner will be notified immediately if the books and records are not in a sufficiently satisfactory condition for performing the audit or if a modified opinion is being contemplated.

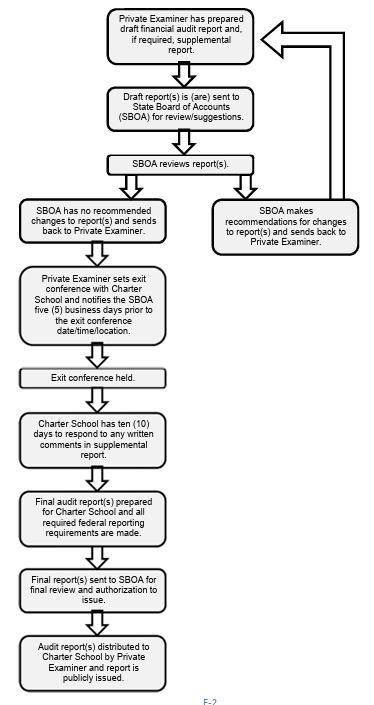

4. The State Board of Accounts will receive a draft copy of the audit report for review at least 5 business days prior to finalization of the audit report, as well as any separate communication to the entity's management, such as a management letter or governance communication letter.

5. The State Board of Accounts will also be provided the names, email addresses, and postal addresses of the governing board president, chief financial officer, and chief executive officer of the entity and the entity's private examiner contact.

6. Upon approval of the draft report and finalization of the audit report, a copy of the audit report will be provided to the State Board of Accounts in an unlocked pdf or Microsoft Word file. These files will be provided within 10 business days of the report being issued by the private examiner.

7. The State Board of Accounts will be notified of the date, time, and location the results of the audit will be discussed with entity officials (exit conference) at least 5 business days prior to the meeting by email.

8. All documentation used to support the audit report as well as any separate communication to the entity's management will be available for review by the State Board of Accounts at the State Examiner's discretion.

9. All correspondence with be via the following email address: charterschools@sboa.in.gov.

Auditing Standards to be AppliedAudits performed in compliance with these guidelines must be conducted in accordance with auditing standards generally accepted in the United States of America (GAAS). Revisions to these standards are to be incorporated at their earliest effective date, as established by the AICPA.

Charter schools that receive and expend federal awards are subject to the provisions of the Uniform Guidance and, if meet the Single Audit thresholds, must also be performed in accordance with Government Auditing Standards, issued by the Comptroller General of the United States. Revisions to these standards are to be incorporated at their earliest effective date, as established by the Comptroller General of the United States.Financial Audit Report

The financial report must contain the financial statements of the charter school and the private examiner's opinion thereon. The financial statements may be prepared on the GAAP basis. If the charter school is required to have a Single Audit, the report must include a Schedule of Expenditures of Federal Awards (SEFA).

If a Uniform Guidance audit is required, two additional reports must be issued:

1. Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of the Financial Statements Performed in Accordance with Government Auditing Standards.

2. Report on Compliance with Requirements That Could Have a Direct and Material Effect on Each Major Program and on Internal Control Over Compliance in Accordance with the Uniform Guidance.

The private examiner is required to comply with all other applicable reporting requirements in accordance with the Uniform Guidance. The Schedule of Expenditures of Federal Awards and notes shall be presented in the format provided in Exhibit D.

For a charter school organizer operating more than one charter school, a consolidated financial audit report may be presented. If a consolidated audit report is presented, it is required that supplementary schedules including a Schedule of Financial Position, by school or location, and a Schedule of Activities and Changes in Net Assets, by school or location, be presented. The private examiner shall provide an “in relation to” opinion on the Supplementary Information.

The financial audit report shall include a reference to any other reports issued by the private examiner for the charter school.

In addition to the findings required to be included in the financial audit report for compliance with Government Auditing Standards and the Uniform Guidance, a supplemental report is required to be issued to identify noncompliance with laws, regulations, and the Accounting and Uniform Compliance Guidelines Manual for Indiana Charter Schools established by the State Board of Accounts.

Indiana Code 5-1-11-9(d) states that on every examination performed, inquiry shall be made as to:

(1) The financial condition and resources of each municipality, office, institution, or entity;

(2) Whether the laws of the State of Indiana and the Accounting and Uniform Compliance Guidelines Manual for Indiana Charter Schools issued by State Board of Accounts established under the authority of IC 5-11-1-24 have been complied with. Exhibit A identifies the required minimum compliance testing. In addition to the required minimum compliance testing, the audit shall include additional compliance testing as deemed necessary for the risks identified during the examination process; and

(3) The methods of preparation and accuracy of the accounts and reports of the charter school.

For audits not required to be conducted in accordance with Government Auditing Standards and the Uniform Guidance, internal control issues that rise to the level of a significant deficiency or material weakness must be included as an Audit Result and Comment in the Supplemental Report.

If a compliance issue is identified during the compliance review and the noncompliance is deemed by the private examiner to be in excess of the parameters set out in Exhibits A and B, a written comment must be included in a supplemental report. The written comment shall be written in accordance with Exhibit B.

The supplemental report is not required to be issued for charter schools where no instances of noncompliance were found.

A supplemental report shall include a transmittal letter, which references the financial audit report, any findings of noncompliance, any internal control findings that are deemed significant deficiencies or material weaknesses, which were not reported in the financial audit report in an audited conducted in accordance with Government Auditing Standards and the Uniform Guidance, a schedule of officials examined, and documentation of the exit conference.

The supplemental report shall also include any official response from the school officials concerning the audit. Per Indiana Code 5-11-5-1, before an examination report is signed, verified, and filed, the officer of the state office, municipality, or entity examined must have an opportunity to review the supplemental report and to file a written response to that report. If a written response is filed, it shall be submitted by the entity to the private examiner and become a part of the supplement report. An example of this supplemental report is presented in Exhibit C.

Malfeasance, Misfeasance, or Nonfeasance

Any fraud identified or brought to the attention of the private examiner, such as misappropriation, embezzlement or other illegal acts shall be reported by the private examiner, immediately upon discovery, to the State Board of Accounts via email to charterschools@sboa.in.gov. The State Examiner retains the authority to and shall investigate any malfeasance, misfeasance, or nonfeasance identified by the private examiner. If the circumstances indicate that a more detailed investigation is needed than necessary under ordinary circumstances, the private examiner shall inform the organization's management and those charged with governance in writing of the need for such additional investigation and the additional compensation required as a result of the additional work needed. An amendment to the audit contract may be made by the charter school and private examiner for such additional investigation, with the written approval of the State Examiner.

Audits performed under the Uniform Guidance must have a completed Data Collection Form included in the reporting package that will be prepared by the charter school and private examiner. The private examiner is responsible for uploading the reporting package and completing all auditor certification emails after the State Board of Accounts approves the financial audit report and supplemental report for issuance.

Upon completion of the audit, the draft financial report, and supplemental report, if applicable, shall be emailed to the charterschools@sboa.in.gov email address prior to report finalization. The reports will be reviewed and any review comments deemed necessary will be returned to the private examiner via email. The reports shall not be issued until reviewed by the State Board of Accounts and approval for audit finalization granted. Therefore, the private examiner cannot disclose any information gained from the audit process prior to this approval, except as allowed under Indiana Code 5-11-5-1(b) and Indiana Code 5-11-51(d). When approval is received from the State Board of Accounts, the private examiner shall issue the reports to the charter school. Additionally, the private examiner is responsible, after the State Board of Accounts approval, to file the report with federal awarding agencies and pass-through entities when an audit is performed in accordance with Government Auditing Standards and/or the Single Audit Act.

The financial audit report and supplemental compliance report will be posted to the State Board of Accounts public website and distributed as required by Indiana Code 5-11-5-1(a) after approval of the reports has been given to the private examiner.

Private examiners are responsible for providing copies of all separate communications containing results of work performed being communicated to the charter school's management, such as management letters and governance communication letters, to the State Board of Accounts. If a management letter or any other reports or correspondence relating to other matters involving internal controls or noncompliance are issued in connection with this audit, a copy shall be submitted with the draft report with the State Board of Accounts. Such management letters, reports, or correspondence shall be consistent with the findings published in the financial audit report or supplemental report (i.e., they shall not include any items that shall be disclosed in the findings found in the published financial audit report or supplemental report, but were not). Submission of these separate communications shall be submitted in the form, time, and process specified above. These items will not be posted or distributed as specified above. There shall be no written communication between the private examiner and the charter school that is not shared with the State Examiner. The private examiner is serving as an agent of the State Examiner and approval of the charter school is not required in order to share any written communication, including work papers, with the State Board of Accounts.

Due to our oversight responsibility for audits performed in accordance with Indiana Code 5-11-1-9, a quality control review of a private examiner's work for sufficiency in scope and adequacy in quality may be performed at the State Examiner's discretion. This review will be performed at the discretion of the State Examiner and prior approval from the charter school for release of the workpapers to the State Board of Accounts is not required. In addition to a quality control review of the audit, we will evaluate findings of noncompliance for further action required of this department. The auditee will be responsible for any cost related to any review performed by the State Board of Accounts. Any reports submitted to the State Board of Accounts shall be at no cost to the State Board of Accounts.

- Required Compliance Testing

Compliance Steps

Verify Submission and Accuracy of Required Reports

Curricular Materials (Textbooks)

Internal Controls (Management Company)

The State Board of Accounts is charged by law with the responsibility of prescribing and installing a system of accounting and reporting which shall be uniform for every public office and every public account of the same class and contain written standards that an entity that is subject to audit must observe. The system must exhibit true accounts and detailed statements of funds collected, received, obligated and expended for or on account of the public for any and every purpose. It must show the receipt, use and disposition of all public property and the income, if any, derived from the property. It must show all sources of public income and the amounts due and received form each source. Finally it must show all receipts, vouchers, contracts, obligations, and other documents kept, or that may be required to be kept, to prove the validity of every transaction. [IC 5-11-1-2]

The system of accounting prescribed is made up of the uniform compliance guidelines and the prescribed forms. A prescribed form is one which is put into general use for all offices of the same class.

Computer hardware, software and application systems can now produce exact replicas of the forms prescribed by the State Board of Accounts. An exact replica of a prescribed form is a computerized form that incorporates all of the same information as the manual prescribed form. Prescribed form replication is the preferred approach from the State Board of Accounts' position. These exact replicas are the equivalent of the prescribed form and require no further action for the charter school to install the form within their accounting system.

The use of computer-generated prescribed forms shall be brought to the attention of the private examiner during the next regularly scheduled audit. The forms and computer system generating the forms are subject to a technical computer audit based upon the results of the risk assessment.

Units are required by law to use the forms prescribed by this department. However, if it is desirable to use a form other than the prescribed manual form, that is not an exact replica; the new form must be approved by State Board of Accounts.

All forms previously approved by sending copies to State Board of Accounts and receiving a form approval letter are approved with the conditions contained within this section.

After April 1, 2014, if a unit implements, consistent with the provisions of Indiana Code and Uniform Compliance Guidelines, an automated accounting system that is to be considered for approval, the responsible official is not required to maintain the prescribed forms replaced by the automated system while awaiting the approval. New forms must be in place during at least one (1) State Board of Accounts audit and must not be an element of an audit finding or audit result and comment that is responsible or partially responsible for an exception found during an audit to be considered approved. The unit is responsible for placing on new forms the year of installation in the upper right corner. This reference should be similar to "Installed in ______________ Charter School, (Year)." The charter school must maintain and present for audit a log of forms installed after April 1, 2014 with the year installed for all forms that replace forms prescribed by State Board of Accounts.

The unit agrees to comply with the following conditions, if applicable, for any new forms installed.

1. The forms and system installed are subject to review and/or recommendations during audits of the unit to ensure compliance with current statutes and uniform compliance guidelines.

2. The unit shall continue to maintain all prescribed forms not otherwise covered by an approval.

3. All transactions that occur in the accounting system must be recorded and accessible upon proper request. Transactions can be maintained electronically, with proper backups, microfilmed, or printed on hardcopy. These transactions include, but are not limited to, all input transactions, transactions that generate receipts, transactions that generate checks, master file updates, and all transactions that affect the ledgers in any way. The system must be designed so that changes to a transaction file cannot occur without being processed through an application.

4. The ability must not exist to change data after it is posted. If an error is discovered after the entry has been posted, then a separate correcting entry must be made. Both the correcting entry and the original entry must be maintained.

5. If the unit owns the source code, sufficient controls must exist to prevent unauthorized modification. If the unit does not own the source code, the vendor shall provide representatives of the State Board of Accounts with access to all computer source codes for the system upon request for audit purposes. In addition, the vendor shall provide representatives of the State Board of Accounts with a document describing the operating system used, the language that the source code is written in, the name of the compiler used, and the structure of the data files including data file names, data file descriptions, field names, and field descriptions for the system.

6. Any receipts, checks, purchase orders, or other forms that require numbering shall be either prenumbered by an outside printing supplier or numbered by the units computer system with sufficient controls installed in the system to prevent unauthorized generation of the form or duplication of numbers.

7. All receipts must be either in duplicate or recorded in a prescribed or approved register of receipts.

8. All checks must be either in duplicate or recorded in a register of checks generated by the computer.

9. Recap sheets for each deposit for deposit advices, if applicable, will be maintained indicating direct deposits. Individual wage assignment agreements will be kept on file to support direct deposit.

10. "Installed by __________ Charter School, (Year)" shall be printed, in the upper right corner, on each approved form furnished by a printing supplier and, when practical, on those printed from accounting systems at the unit. Upon the installation of a new form the form will be entered on a log for this purpose with the date of installation; and the name and number of the prescribed form replaced. The log must be available for audit.

11. The unit officials are responsible to ensure that forms and accounting systems installed comply with the uniform compliance guidelines for information technology services published in the Charter School Administrator and accounting manuals. This includes ensuring that customization of the system done by the vendor for implementation at the government is done in such a manner that the system remains compliant.

12. In the event a change is required due to the passage of a State or Federal law, the unit agrees to implement the change in a timely manner.

Although the State Board of Accounts prescribes forms, copies of the forms must be purchased from a public printer or other source.

Use of Prescribed Forms

Officials and employees are required to use State Board of Accounts prescribed or approved forms in the manner prescribed.

Audit Procedures:Review prescribed form usage to determine that the charter school is using prescribed or approved forms.

Determine that alternate computer forms include at a minimum, the information on the prescribed form.

The organizer shall designate employees who are responsible for handling a majority of the cash, receipts, and disbursements for the school. The designated employees must have either a cash bond or an insurance policy on their behalf that protects the charter school from employee theft, fraud, errors, and omissions. The cash bond or insurance policy shall be established at an amount approved by the board.

Audit Procedures:Verify that the organizer has designated an employee or employees who are responsible for handling the majority of the cash, receipts, and disbursements for the school.

Determine that the designated employees have either a cash bond or an insurance policy on their behalf. Retain a copy of the bond or insurance policy for inclusion in the audit documentation. If there is no cash bond or insurance policy on the individual designated, which protects the charter school from theft, fraud, errors, and omissions, an Audit Result and Comment (ARC) must be written.

VERIFY SUBMISSION AND ACCURACY OF REQUIRED REPORTSAVERAGE DAILY MEMBERSHIP (ADM)

Officials shall maintain records (enrollment applications, attendance records, reporting forms, etc.) which substantiate the number of students claimed for ADM. A student claimed for ADM must be an "eligible pupil". An eligible pupil is a student that is enrolled and attending.

IC 20-43-1-11: "'Eligible pupil' refers to an individual who qualifies as an eligible pupil under IC 20-43-4-1".

IC 20-43-1-11.5 defines "Enrolled" as registered with a school corporation to attend educational programs offered by or through the school corporation; and attending these educational programs or receiving education services.

IC 20-43-1-7.5 defines "Attending" as physical or virtual presence of a student with the expectation of continued services in the education programs for which the student is registered.

The Organizer is responsible for reporting ADM to the Indiana Department of Education (IDOE). The ADM Summary Report shall provide a written certification of ADM to properly document responsibility. The ADM Summary Report must be signed by the Superintendent/Principal/Director of Schools and the Trustee/Corporate Treasurer and be uploaded to IDOE for each reporting period in the fiscal year. Supporting documentation of enrollment and attendance/engagement information by grade and school must be maintained for audit.

ANNUAL REPORTAnnual Financial Report (AFR) - SBOA

Charter schools are required to file an annual report with the State Examiner not later than sixty (60) days after the close of each fiscal year, IC 5-11-1-4.

Certified Report (100R) - SBOA

Indiana Code 5-11-13-1(a) states in part:

"Every state, county, city, town, township, or school official . . . shall during the month of January of each year prepare, make, and sign a certified report, correctly and completely showing the names and business addresses of each and all officers, employees, and agents . . . and the respective duties and compensation of each, and shall forthwith file said report in the office of the state examiner of the state board of accounts . . . The certification must be filed electronically in the manner prescribed under IC 5-14-3.8-7."Form 9 - IDOE

Charter schools are required to submit a Form 9 Biannual Financial Report two times per year during the months of January and July. The financial information in the Form 9 shall reflect cash basis information and shall be reported utilizing the State Board of Accounts prescribed chart of accounts. The January report must include previous calendar year financial and other required information for the period of July 1 to December 31 financial data. The July report must include current calendar year financial and other required information for the period of January 1 to June 30.

Charter schools must file Form 9 information electronically with the Office of School Finance. Questions related to Form 9 filing and other requirements can be directed to staff in the Office of School Finance by emailing form9@doe.in.gov.

Audit Procedures:ADM Reporting:

1. Gain and document an understanding of the charter school's procedures to ensure accurate reporting of ADM.

2. Assess overall Risk of Material Noncompliance for ADM reporting. If the school is a virtual school, the inherent risk must be established as high.

3. Obtain the ADM Summary Report for each count date as submitted to IDOE and determine that it was signed by the appropriate officials (the Superintendent/Principal/Director of Schools and the Trustee/Corporate Treasurer).

4. Obtain the ME Roster Download from the school and compare in total to the Summary Reports.

5. Verify that the ADM counts reported were proper by selecting a sample of students and test that each student claimed was:

a) properly enrolled;

b) attending;

c) within the minimum/maximum age requirements;

d) in Indiana at count date.

Required Amount of Testing:The auditor should determine an appropriate sample size based on assessed risk; however, a minimum sample size of 10% of students or 60, whichever is less, shall be tested for a school with a low assessed risk. Sample sizes should be increased for an assessment other than low.

For an organizer that has more than one school, a separate sample from each school is required.

Samples should include students from both count dates in the school year.

If a school is not fully virtual, but does have some virtual students, the sample must be stratified to include both virtual and non-virtual students.

Auditor Considerations:Properly Enrolled

Enrollment documents required to be maintained on file by the school have not been defined by IDOE. Records, such as paper or electronic enrollment applications, as well as copies of birth certificates and proof of residency, etc. as determined by policy or normal practice of the school should be reviewed. Ensure that for each student sampled that the records maintained are consistently applied across students. Lack of records for certain students could be an indicator that a student was not properly enrolled.

Attending

The auditor should review attendance/engagement records for the sampled students. A student should be physically present on the official count date unless officially marked absent (for brick and mortar schools). For any student absent on the count date, attendance records for the student should be reviewed.

For virtual schools, IDOE has not defined what constitutes sufficient engagement. Ensure that for each sampled student, documentation presented by the school demonstrates that the student had evidence of engagement within the two (2) weeks prior to the official count date. Records such as class schedules, login records for learning management systems showing login dates and times and completion of course assignments, and teacher logs for students showing engagement with a student could be acceptable support demonstrating student engagement. If there was no evidence of student engagement for the sampled student within the two (2) week period prior to the count date, the auditor should review the school's engagement policy to determine if the school was in compliance with its engagement policy for progressive student and parent contact during the period of no student engagement, up to and including removal of the student for lack of engagement.

Lack of records that the student was in attendance on the count date or was engaged (logging in, completing assignments in a learning management system) is an indicator that the student did not meet the definition of attending.

Age Requirement

The student should be age 5 by the appropriate date and under age 22 to be considered an eligible pupil. It is acceptable to only test those students selected in the sample from the Kindergarten class for the age 5 requirement, and those students in the 12th grade for the maximum age requirement (NA for students selected not at those grade levels).

Indiana Residency

The student must have Indiana residency. Schools may accept students who do not have legal settlement in Indiana; however, these students cannot be counted for ADM.

Each school corporation’s governing body or charter school board must annually adopt or readopt a policy that specifies documentation, not to exceed three items, required to verify Indiana residency.

If a student enrolls in a different school corporation or charter school during the school year, proof of Indiana residency must be filed with the new school corporation or charter school. If a student has a change of address from one school year to another, the prior residency documents should be maintained in the student’s file. For audit purposes, a school should be able to produce a physical or scanned copy of residency proof for current and prior residency of each student.

Reporting Requirements:If there are ANY exceptions to the properly enrolled or attending attributes, an ARC is mandatory.

In the condition paragraph of the ARC, include the sample size and number of exceptions found. If a student was not in attendance on the count date (brick and mortar school) or either not in attendance on count date or not engaged in the two weeks prior to the count date (virtual schools), consider the student an exception to the attending/engaged attribute. Include in the condition paragraph the number of exceptions and detail describing the nature of the exception such as lack of indication of student engagement, lack of supporting records maintained, etc.

For the students considered exceptions to the attending/engaged attribute, also include in the condition paragraph whether the school was in compliance with its engagement policy (virtual schools) for progressive student and parent contact during the period of no student engagement up to and including removal of the student for lack of engagement.

All ARCs will be reviewed by SBOA prior to approval for exit. During the audit, a firm may communicate any testing concerns or questions to the charter school email address (charterschools@sboa.in.gov).

Annual Financial Report (AFR) - SBOA

1. Verify that the charter school filed the AFR with the SBOA within 60 days following its fiscal year end.

Certified Report (100R) - SBOA

1. Verify that the charter school filed the 100R with the SBOA by January 31st. Scan to ensure 100R appears complete.

Reporting Requirements (applicable to both AFR and 100R):Submission of the 100R and AFR are to be made via the Indiana Gateway for Governmental Units (Gateway).

If the AFR or 100R was filed between 1 and 6 days late, make this a discussion only issue (verbal comment). If it was filed between 7 and 59 days late, a comment must be reported in a Management Letter to the school. If the AFR was filed 60 or more days late, a mandatory ARC must be written.

Form 9 (IDOE)

1. Verify that the Form 9 Financial Information agrees to the cash records of the charter school.

a. Obtain management's schedule or reconciliation between the Form 9 summary data and the general ledger.

b. Trace the fund balance report activity from the accounting system to the Form 9 report.

2. Verify that the financial information is reported utilizing the Chart of Accounts prescribed by the State Board of Accounts.

a. Did the financial information utilize the prescribed funds, per Part 3, Uniform Compliance Guidelines for Indiana Charter Schools. Document how auditor determined proper funds usage.

b. Did the financial information utilize the prescribed receipt codes, per Part 4, Uniform Compliance Guidelines for Indiana Charter Schools. Document how auditor determined proper receipt code usage.

c. Did the financial information utilize the prescribed expenditure codes, per Part 5, Uniform Compliance Guidelines for Indiana Charter Schools. Document how auditor determined proper expenditure code usage.

Reporting Requirements:

If the Form 9 Financial Information does not agree to the cash records of the school an ARC is mandatory unless clearly trivial.

If the charter school does not utilize the State Board of Accounts Chart of Accounts to maintain and report the school's financial activity an ARC is mandatory.

MEETINGS OF THE CHARTER SCHOOL'S BOARD

The Charter School's charter must specify that the charter school is subject to the requirements of IC 5-14-1.5, Public Meetings (Open door) Law. IC 20-24-4-1(a)(15)

Indiana Open Door Law

Board meetings are governed by the Open Door Law, IC 5-14-1.5. Under the Open Door Law all meetings of governing boards must be open to the public except for executive sessions.

Audit Procedures:Verify that the school's charter specifies that the charter school is subject to the requirements of the Open Door Law.

Verify that the Open Door Law was observed for applicable meetings.

CONSULTANTS - STATUTORY CONFLICT OF INTEREST [IC 5-16-11]

Audit Procedures:Review Part 13 of the charter school manual as well as IC 5-16-11 and determine that the appropriate conflict of interest statements have been filed. Conflict of Interest statements shall also be provided to the State Board of Accounts.

MONTHLY RECONCILEMENTS MAINTAINED

All financial records must be kept up-to-date and reconciled monthly.

Audit Procedure:Determine if the charter school is reconciling their accounts monthly. Failure to comply with this requirement results in a mandatory ARC.

CAPITAL ASSETS

Every charter school must have a capital assets policy that details the threshold at which an item is considered a capital asset. Every charter school must have a complete detail listing of all capital assets owned which reflects their acquisition value. A complete physical inventory must be taken at least every two (2) years, unless more stringent requirements exist, to verify account balances carried in the accounting records.

The list of capital assets should include the following categories:

Land

The records of each charter school must include a description of land owned by the charter school, its location amount of acreage (if relevant), its acquisition date and the purchase price. If the purchase price is not available, appraised value may be used.

Infrastructure

A capital asset account for the cost of infrastructure must reflect the location and brief description identifying each road, bridge, tunnel, drainage system, storm water system, dam, or lighting system owned by the charter school.

Buildings

A capital asset account for buildings must reflect the location of each building and the purchase price or construction cost and the cost of improvements, if applicable. If a building is acquired by gift, the account must reflect its appraised value at the time of acquisition.

Improvements Other than Buildings

A capital asset account must reflect the acquisition value of permanent improvements, other than buildings, which have been added to the land. Examples of such improvements are fences, retaining walls, sidewalks, and gutters. The improvements must be valued at the purchase or construction cost.

Equipment

Tangible property of a permanent nature (other than land, buildings, and improvements) must be inventoried. Examples include machinery, trucks, cars, furniture, office equipment including but not limited to computers and data processing equipment, and desks, safes, cabinets, books, cell phones, etc. The value of such items must be carried in the inventory at the purchase cost.

Construction Work in Progress

Where construction work has not been completed in the current reporting fiscal year, the cost of the project must be carried as "construction work in progress." When the project is completed, it must be placed on the inventory applicable to the assigned asset account.

Asset Ownership

Assets purchased by a charter school must be titled appropriately in the name of the charter school.

Audit Procedures:Determine that the charter school has maintained an up to date capital asset inventory.

Verify that the charter school has conducted a physical inventory within the last two (2) years.

Verify that all assets purchased by the charter school were titled in the name of the charter school.

RECEIPTS AND DEPOSIT

Receipts shall be issued and recorded at the time of the transaction; for example, when cash or a check is received, a receipt is to be immediately prepared and given to the person making payment.

All charter school money must be deposited in the designated depository not later than the business day following the receipt of funds on business days of the depository in the same form in which the funds were received. Charter schools are not required to deposit funds on the next business day if the amount on hand does not exceed $500. However, the funds must be deposited by the school following the day they exceed $500. Timely receipts and deposits are required to provide the organizer and charter school administration with current information necessary for all financial decisions.

Fees

Fees shall only be collected as specifically authorized by statute or properly authorized resolutions or ordinances, as applicable, which are not contrary to statutory or Constitutional provisions.

Fund Sources and Uses

Sources and uses of funds shall be limited to those authorized by the enabling statute, ordinance, resolution, or grant agreement.

Audit Procedures:Select receipts of public funds (See Required Amount Testing) and perform the following:

- Were receipts issued at the time of transaction, when cash or check was received?

- Were timely deposits made?

- Were receipts properly secured prior to deposit?

Determine if the classification on the receipt (i.e., cash, check, etc.) agrees with the actual amounts of cash, checks, etc., shown on the deposit slip to insure deposits are made in the same form received. Further review is required if discrepancies exist (i.e., check for cash substitution).

Determine that the collection is properly receipted into the proper fund based on the source of the collection in accordance with the prescribed chart of accounts.

If any receipts selected are fees established by the charter school board, determine that the fees are collected in accordance with a fee schedule adopted by the charter school board.

PURCHASING AND EXPENDITURES

The charter school must establish procedures for the initiation, approval, and use of purchase requisitions and purchase orders. The procedures must include limits on approval of purchase orders after the purchase to emergency situations and all blanket purchases must have a fixed monetary limit. Upon receipt of the goods or services a charter school employee must verify the condition, quantity, and quality of the goods or services prior to payment of the invoice/bill/contract. Supporting documentation, such as invoices, shall be compared to purchase orders to ensure the prices, quantities, etc. are correct prior to payment.

ACCOUNTS PAYABLE VOUCHER (FORM 523)

The Accounts Payable Voucher (Form 523) is designed to replace Claim Form 505. The form must be used in accordance with the following conditions: Charter schools may not draw a warrant or check for payment of a claim unless; (1) there is a fully itemized invoice or bill for the claim; (2) the invoice or bill is approved by the officer or person receiving the goods and services; (3) the invoice or bill is filed with the fiscal officer; (4) the fiscal officer audits and certifies before payment that the invoice or bill is true and correct; and (5) payment of the claim is allowed by the board having jurisdiction over the allowance of the payment of the claim.

Advance Payments

Compensation and any other payments for goods and services shall not be paid in advance of receipt of the goods or services unless specifically authorized by statute. Payments made for goods or services which are not received may be the personal obligation of the responsible official or employee.

Cash Disbursements

Disbursements, other than properly authorized petty cash disbursements, shall be by check or warrant, not by cash or other methods unless specifically authorized by statute, federal or state rule.

Contracts

Payments made or received for contractual services must be supported by a written contract. Each charter school is responsible for complying with the provisions of its contracts.

Donations

Public funds must not be donated or given to other organizations, individuals, or charter schools unless specifically authorized by statute.

Expense Reimbursement Itemization

All claims, invoices, receipts, and accounts payable vouchers shall contain adequate detailed documentation. All claims, invoices, receipts, and accounts payable vouchers regarding reimbursement for meals and expenses for individuals must have specific detailed information of the names of all individuals for which amounts are claimed, including the nature, name, and purpose of the business meeting, to enable payment. Payments which do not have proper itemization showing the business nature of the claim may be the personal obligation of the responsible employee or other person for whom the claim is made.

Personal Expenses

Public funds shall not be used to pay for personal items or for expenses which do not relate to the functions and purposes of the charter school. Any personal expenses paid by the charter school may be the personal obligation of the responsible employee.

Penalties, Interest, and Other Charges

Officials and employees have the duty to pay claims and remit taxes in a timely fashion. Additionally, officials and employees have a responsibility to perform duties in a manner which would not result in any unreasonable fees being assessed against the governmental unit. Any penalties, interest or other charges paid by the governmental unit may be the personal obligation of the responsible official or employee.

Sales Tax

Charter schools are eligible for an exemption from the state sales tax on purchases. To obtain the exemption for a Sales Tax Exemption Certificate, application shall be made to the Sales Tax Division of the Department of Revenue. This certificate must be presented at the time a purchase is made to avoid paying sales tax. If sales tax is paid erroneously, a refund application may be obtained from the Sales Tax Division.

Lodging for individuals in hotels and motels is not exempt from state sales tax. Therefore, reim- bursements for lodging in approved travel status may include state sales tax. However, it shall be kept in mind that claims for all such reimbursements must be supported by a fully itemized receipt showing date(s) of lodging, the name(s) of the person(s) occupying the room and the amount paid.

Governmental funds generally are exempt from the payment of sales tax on qualifying purchases. Respective tax agencies shall always be contacted concerning tax exemptions and payments.

Audit Procedures:For selected vendor checks or Electronic Fund Transfers (EFTs) (see required minimum testing) perform the following:

- Determine if the voucher or attached invoice is adequately itemized.

- Check math accuracy.

- Determine if certified by the employee designated.

- Determine if approved by the approving board.

- If payment for a contractual service, is there a written contract? Compare to contract price, if applicable.

- Compare accounts payable voucher amount to supporting documentation and check amount, if applicable. Supporting documentation must be detailed, not just a statement or credit card slip.

- Determine that sales tax was not paid inappropriately; note that sales tax can be reimbursed for nonexempt purchases, including lodging.

- Verify that payment was not made in advance.

- Verify that payment was made timely, not incurring any late fees. If any penalties or interest are paid due to untimely payment, an ARC is required to be written detailing the amount of penalties and interest paid.

- Verify that payment was not made by cash.

- Determine that payment was not a donation.

- Determine that expense was not a personal expense, but was attributable to the operation of the charter school.

Required Amount of Testing:A minimum of 25 vendor disbursements shall be tested when no deviations are expected to be found. This would be a charter school with a planned or supported assessed level of control risk as low.

A minimum of 40 disbursements shall be tested when 1 deviation is expected to be found. This would be a charter school with a planned or supported assessed level of control risk as moderate.

A minimum of 60 receipts disbursements shall be tested when three or more deviations are expected to be found. This would be a charter school with a planned or supported assessed level of control risk as high.

An ARC is mandatory if there is a 10 percent or greater error rate with any one of the attributes tested.

An ARC is mandatory if disbursements are not approved by the Board. Approval of disbursements can be made at a subsequent Board meeting.

SPECIFIC TESTING ON TRAVEL CLAIMS

TRAVEL AND MEETINGS

The charter school must establish a travel policy that details the procedures for an employee to get approval to attend meetings and conferences; must detail when an employee is in travel status; must detail the procedures for employees to get reimbursement for travel expenses; and the policy must establish a reasonable mileage reimbursement rate.

If the charter school authorizes travel advances, it must have a policy identifying the individual who may receive an advance, the use and purpose of the advance, the information that is required to account for the advance, a reconciliation of actual expenses (upon return for the trip) versus amounts advanced, and the refunding of any excess money that was in advanced in a timely manner.

The charter school shall only reimburse employees for travel expenses when appropriate claims are submitted. The claims must be in writing, itemized, and supported with original receipts, and documentation that the trip was for charter school business.

The charter school must establish a policy which describes the circumstances when it is appropriate for providing food and beverages at meetings, training, and conferences sponsored by the charter school.

Commuting Mileage

Reimbursed mileage shall not include travel to and from the employee's home and the charter school building in which he works, unless otherwise authorized by statute.

Audit Procedures:Determine if the charter school has adopted a travel policy. Obtain a copy of the travel policy in the audit documentation.

If the travel policy allows for advances, test advances provided (number to be determined by examiner) for proper handling.

Perform a test (number to be determined by examiner) of travel reimbursements to determine that appropriate claims have been submitted.

- Claims are in writing.

- Claims are properly itemized.

- Claims are supported by original receipts.

- Proper documentation was provided that the trip was for charter school business.

For mileage reimbursements, if applicable, determine that mileage does not include travel to and from the employee's home or building of employment. Also determine that the mileage rate of pay agrees to the charter school's travel policy.

REVIEW CREDIT CARD POLICY, PROCEDURES, AND DISBURSEMENTS

Credit Cards

The State Board of Accounts will not take exception to the use of credit cards by a charter school provided the following criteria are observed:

1. The charter school must authorize credit card use through an appropriate policy.

2. Issuance and use shall be handled by an employee designated by the charter school.

3. The purposes for which the credit card may be used must be specifically stated in the policy.

4. When the purpose for which the credit card has been issued has been accomplished, the card must be returned to the custody of the designated employee.

5. The designated employee must maintain an accounting system or log which would include the names of individuals requesting usage of the cards, their position, estimated amounts to be charged, fund and account numbers to be charged, date the card is issued and returned, etc.

6. Credit cards shall not be used to bypass the accounting system. One reason that purchase orders are issued is to provide the fiscal officer with the means to encumber and track expenses to provide the charter school and other administration with timely and accurate accounting information and monitoring of the accounting system.

7. Payment shall not be made on the basis of a statement or a credit card slip only. Procedures for payments shall be no different than for any other claim. Supporting documents such as paid bills and receipts must be available. Additionally, any interest or penalty incurred due to late filing or furnishing of documentation by an officer or employee shall be the responsibility of that officer or employee.

8. If properly authorized, an annual fee may be paid.

Audit Procedures:Determine if the following criteria for the use of credit cards have been observed:

a. Charter School has appropriately adopted a credit card policy. Retain a copy of the policy in the audit documentation.

b. Issuance and use is handled by an official or employee designated by the charter school.

c. The purpose for which the credit card may be used is specifically stated in the policy

d. When the purpose for which the card has been issued has been accomplished, the card is returned to the custody of the responsible official.

e. The designated responsible official or employee maintains an accounting system or log which includes the names of individuals requesting usage of the cards, their position, estimated amounts to be charged, fund and account numbers to be charged, and the date the card is issued and returned.

f. Credit cards are not used to bypass the accounting system.

g. Payment is not made on the basis of a statement or a credit card slip only. Procedures for payments are processed the same as for any other claim. Supporting documents such as paid bills and receipts are available. Any interest or penalty incurred due to late filing or furnishing of documentation by an officer or employee is the responsibility of that officer or employee.

h. Annual fees, if applicable, must be authorized by the management of the charter school and/or organizer.

i. Required minimum testing, select a minimum of 5 credit card payments for testing, if any interest or penalties are paid due to untimely payment, an ARC is required to be written detailing the amount of penalties and interest paid.

REVIEW COMPLIANCE WITH PUBLIC WORKS LAWSGENERAL PROVISIONS

When a charter school uses public funds for the construction, reconstruction, alteration, or renovation of a public building, bidding and wage determination laws and all other statutes and rules apply, IC 20-24-7-7.

Audit Procedures:

For projects that meet the definition of public works (IC 36-1-12), test the following:

- Were Specifications for the project appropriately prepared?

- Was the bid sought through the proper advertisement?

- Was the bid Form 96 used?

- Was contract awarded pursuant to IC 36-1-12?

- Were financial statements provided with the bid?

- Escrow contract for retainage per IC 36-1-12-14 is intact?

- A performance bond was included with the bid documents?

- A non-collusion affidavit was provided with the bid documents?

- Any change orders were approved and not greater than 20 percent of the original contract amount?

An ARC is required to be written if there is any noncompliance identified with the public works laws.

REVIEW PAYROLL POLICIES AND TEST FOR PAYROLL COMPLIANCE

PAYROLL PROCEDURES

The charter school must establish a payroll schedule that details amounts paid annually, biweekly, hourly, etc. for all employees that are not included on a labor contract. The charter school must establish written employment policies that cover all aspects of benefits provided including sick days, vacation days, personal days, etc. The policy must cover how many days are accrued, when the days are accrued, when any unused days are lost, etc.

The charter school shall maintain adequate supporting documentation for payroll to ensure that payments are made only for services rendered. Supporting documentation, such as time cards, must show signs of supervisory approval. The organizer must designate an employee to review supporting documentation to ensure payments are accurate and due the employee for services rendered.

The charter school must establish a system to document and track paid leave activity. The system must be able to track the accrual of earned leave time and the use of leave time each pay period and throughout the year. The charter school must document and provide the organizer in writing all changes to pay amounts or benefits provided prior to the changes going in effect.

Advance Payments

Compensation and any other payments for goods and services shall not be paid in advance of receipt of the goods or services unless specifically authorized by statute. Payments made for goods or services which are not received may be the personal obligation of the responsible official or employee.

Compensation

All compensation and benefits paid to employees must be included in the at-will employment agreement or letter, or labor contract or salary schedule, unless otherwise authorized by statute. All compensation and benefits paid to employees must be included in the labor contract or salary schedule unless otherwise authorized by statute. Compensation must be made in a manner that will facilitate compliance with state and federal reporting requirements.

Payments for services provided by an organization shall go directly to the organization and not to an individual employee of the organization. All payments for services must be supported by a written contract.

Fund Sources and Uses

Sources and uses of funds shall be limited to those authorized by the enabling statute, ordinance, resolution, or grant agreement.

Leave and Overtime Policy

Each charter school must adopt a written policy regarding the accrual and use of leave time and compensatory time and the payment of overtime. Negotiated labor contracts approved by the charter school would be considered as written policy. The policy must conform to the requirements of all state and federal regulatory agencies.

Severance Pay

Unless specifically authorized by statute, severance pay, or other payments to employees upon separation from employment, must be supported by the written opinion of the attorney for the charter school stating that the payments are in accordance with all federal laws and regulations and state laws, as applicable.

Suspension with Pay

Suspension with pay must be supported by the written opinion of the attorney for the charter school stating that the suspension is in accordance with all federal laws and regulations, and state laws, as applicable.

Audit Procedures:1. Verify that the charter school organizer and/or management of the charter school has appropriately established a payroll schedule or has labor contracts on file for employees.

2. Review employment policies, including leave and overtime policy; retain policies as audit documentation in the working papers.

3. For those charters that transfer money to an Education Management Organization (EMO) for employees which are paid by the EMO, verify that the charter school has adequate supporting documentation for the payroll transfer that ensures that payments are made only for services rendered at the charter school.

4. Select employees (See Required Minimum Testing) and test for the following:

a. The amount and rate of pay paid for the employee agrees with the payroll schedule and/or labor contract.

b. Attendance/Time Records were maintained for the employee.

c. Pay has been properly posted to the employee's earnings record.

d. Employee's earnings record agrees to the Form W-2 for the year.

e. Payment was made from the proper fund. In the case where an employee's salary is paid from multiple funds, the charter school shall keep records to ensure that the employee's time is allocated appropriately across funds for payment.

f. Verify that the employee is not being paid in advance of hours worked.

5. Inquire to school officials if anyone has received any severance pay or suspension with pay.

If applicable, verify that a written opinion was received by the charter school attorney, stating that the payments are in accordance with all federal laws and regulations, and state laws, as applicable. This written opinion shall be received prior to providing the pay.

Required Amount of Testing:A minimum of 15 employees shall be tested when no deviations are expected to be found. This would be a charter school with a planned or supported assessed level of control risk as low.

A minimum of 25 employees shall be tested when 1 deviation is expected to be found. This would be a charter school with a planned or supported assessed level of control risk as moderate.

A minimum of 40 employees shall be tested when three or more deviations are expected to be found. This would be a charter school with a planned or supported assessed level of control risk as high.

An ARC is mandatory if there is a 10 percent or greater error rate with any one of the attributes tested.Federal and State Regulations

Each charter school is responsible for compliance with all rules, regulations, guidelines, and directives of the Internal Revenue Service and the Indiana Department of Revenue. All questions concerning taxes shall be directed to these agencies.

Penalties, Interest, and Other Charges

Officials and employees have the duty to pay claims and remit taxes in a timely fashion. Additionally, officials and employees have a responsibility to perform duties in a manner which would not result in any unreasonable fees being assessed against the governmental unit. Any penalties, interest or other charges paid by the governmental unit may be the personal obligation of the responsible official or employee.

Audit Procedures:For amounts withheld perform the following:

Determine that disbursements of withholdings were submitted to the proper authority.

For late payments and/or interest assessed:

Determine if any late payments and/or interest charges were assessed on obligations of the charter school. If late payments and/or interest charges were assessed an ARC is required to be written detailing the amount of penalties and interest paid.

REVIEW INTERNAL CONTROLS OVER EDUCATIONAL MANAGEMENT COMPANY CONTRACT AND PROCEDURES

INTRODUCTION

Charter schools shall have internal controls in place to provide reasonable assurance that their goals and objectives are accomplished; laws, regulations, and good business practices are complied with; assets are safeguarded; and accurate and reliable data are maintained. Internal control touches all activities of the school, extending beyond the accounting and financial functions. It is important to note that even the best internal controls may breakdown due to management override, collusion, mistake, faulty judgment, or cost constraints. The following internal control related compliance guidelines provide required controls that a charter school must implement and maintain.

ADMINISTRATION

The charter school must establish minimum policies and procedures concerning operations.

The charter school must engage in active oversight by routinely receiving and discussing financial reports from the organizer.

The charter school administrators must be cognizant of their duties of care, loyalty, and obedience. The duty of care requires administrators to be familiar with the charter school's finances and activities and to participate regularly in its operations. Duty of loyalty requires that any conflict of interest, real or possible, always be disclosed in advance of being employed and when they arise. A charter school has a duty of obedience to insure that the school complies with applicable laws and regulations and its internal policies and procedures.

Internal Controls

Charter schools shall have internal controls in effect which provide reasonable assurance regarding the reliability of financial information and records, effectiveness and efficiency of operations, proper execution of management's objectives, and compliance with laws and regulations. Among other things, segregation of duties, safeguarding controls over cash and all other assets and all forms of information processing are necessary for proper internal control. Controls over the receipting, disbursing, recording, and accounting for the financial activities are necessary to avoid substantial risk of invalid transactions, inaccurate records and financial statements and incorrect decision making.

Audit Procedures:Does the charter school organizer contract with an Educational Management Company? If so, retain the contract in the audit documentation.

Review and describe in a narrative form the relationship between the Education Management Company and the charter school.

Review controls in place by the organizer and/or charter school that provides assurance that the management company is completing the duties as outlined in the contract and that the charter school is only paying for services in which the management company is providing for their specific school. Determine that the controls are effective and that the organizer has maintained control over the fiscal duties.

REVIEW EXTRACURRICULAR ACTIVITIESIC 20-41 does not allow for charter schools to create extra-curricular accounts. All monies received and disbursed for extracurricular activities would need to be included and processed through the charter school records.

Audit Procedures:If the charter school has extracurricular activities ensure that the money received and disbursed for those activities are accounted for in the funds of the charter school. If extracurricular activities are accounted for in separate accounts that are not maintained on the charter school's financial records, an ARC shall be written.

ATHLETIC AND SOCIAL EVENTS

Serially pre-numbered tickets by the printing supplier shall be used for all athletic and other social activities and events for which admission is charged. Part of the pre-numbered ticket must be given to the person paying for the ticket upon admission to the event. The other part of the ticket (which shall also be pre-numbered, referred to as the stub) must be retained. All tickets (unused tickets and stubs) shall be retained for audit.

Tickets for each price group must be different colors and/or different in their series number.

Ticket sales conducted by any activity shall be accounted for as follows:

The designated charter school employee shall be responsible for the proper accounting for all tickets and must keep a record of the number purchased, the number issued for sale, and the number returned. The designee must see that proper accounting is made for the cash received from those sold. All tickets shall be pre-numbered, with a different ticket color and numerical series for each price group. When cash for ticket sales is deposited with the charter school, the charter school's receipt issued therefore must show the number of tickets issued to the seller, the number returned unsold and the balance remitted in cash. All tickets (including free or reduced) must be listed and accounted for on the SA-4 Ticket Sales Form.

Deposit of Accountable Items

Tickets, goods for sale, billings, and other collections, are considered accountable items for which a corresponding deposit must be made in the bank accounts of the charter school.

The deposit ticket or attached documentation must provide a detailed listing of the deposit, which includes at a minimum, check numbers and corresponding names of the payors.

Audit Procedures:If extracurricular events are held, verify that pre-numbered tickets and ticket sale reports (Form SA-4) are used.

Ticket sale reports shall be tested (number to be determined by examiner) to ensure the following:

1. The charter school's receipt of monies agrees to the ticket sales reports.

2. Monies were deposited daily.

3. All tickets are accounted for on the SA-4 Ticket Sales Form.

- Audit Results and Comments