Search for Keywords

- A

Annual Financial Report Updates 2025

Appropriation of Insurance Claim Proceeds

Appropriations of Federal and State Funds

Assignment of Wages - Wage Deductions

IC 5-3-1-3 provides that each library fiscal officer shall have published an annual report of the receipts and expenditures of such library within 60 days after the close of each calendar year. (link: https://iga.in.gov/laws/2024/ic/titles/5#5-3-1-3 )

IC 5-11-1-4 requires such reports to be filed with the State Examiner, as set forth in the Uniform Compliance Guidelines, which states no later than sixty (60) days after the close of the year. (link: https://iga.in.gov/laws/2024/ic/titles/5#5-11-1-4 )

If the library has a budget of at least $300,000, the “Cash and Investments Combined Statement” of the annual report is to be published one time in two newspapers unless there is only one newspaper in the library territorial limits, in which case publication in the one newspaper is sufficient. If no newspaper is published in the library territorial limits, then publication is to be made in a newspaper published in the county in which the library is located, and that circulates within the library territorial limits.

The “Cash and Investments Combined Statement” to be advertised is located in the Annual Report Outputs section under “Advertising Outputs”.

The Department of Local Government Finance may not approve the budget or a supplemental appropriation of a library until the library files an annual report for the preceding calendar year.

ANNUAL FINANCIAL REPORT UPDATES 2025

As we begin year-end duties and prepare for completion of the 2025 Annual Financial Report (AFR), we want to highlight a few important updates you will notice throughout the report. In the Unit Questions section, questions 12–20 will be automatically prefilled with “Not Applicable.” These items have been inactivated for this year’s reporting, which means the Transfer Schedule, Interfund Loan Schedule, and Tax Abatement Schedule will not be required for the 2025 AFR.

If you encounter any issues or have additional questions regarding the AFR, please contact the Directors for assistance.

APPROPRIATION OF INSURANCE CLAIM PROCEEDS

Insurance proceeds should be receipted back into the fund which originally paid for the asset. These funds would not need to be appropriated if they are being spent within the year of receipt. However, if the repair to the asset exceeds the proceeds from insurance, then you would need to appropriate for the overage. IC 6-1.1-18-7 discusses this topic (link: https://iga.in.gov/laws/2024/ic/titles/6#6-1.1-18-7 )

Pursuant to IC 6-1-1-18-6, the library board may transfer money from one major budget classification to another within a department or office if:

- They determine that the transfer is necessary;

- The transfer does not require the expenditure of more money than the total amount set out in the budget as finally determined under IC 6-1.1; and

- The transfer is made at a regular public meeting and by proper resolution.

A transfer may be made under this section without notice and without the approval of the Department of Local Government Finance.

Unanticipated LIRF expenditures and appropriation of unanticipated revenue require a board resolution, publication of the additional appropriation request, public hearing, and approval by the Department of Local Government Finance.

APPROPRIATIONS OF FEDERAL AND STATE FUNDS

When funds are provided by the federal government either directly to or through a state agency for any program or project, the following procedures should be followed:

Advance Grants. Advance grants should be handled as follows:

- Where funds are “advanced” directly by the federal government for a specific purpose prior to making any disbursements, the money should be placed in a separate project fund and disbursements subsequently made from that fund. No appropriation of the federal funds is required.

- Where federal funds are “advanced” through a state agency or department with no state funds added thereto prior to making any distributions, the money should be placed in a separate project fund and subsequent disbursements made from that fund. No appropriation of the federal funds is required.

- Where federal funds are “advanced” by a state agency or department and state funds are included along with the federal funds in one check or voucher and the funds are for a specific purpose, the money should be placed in a separate project fund and disbursements made from that fund. Appropriation(s) must be obtained for the combined total (i.e., federal and state) prior to any disbursement being made from that project fund.

Reimbursement Grants. Reimbursement grants should be handled as follows:

Where a federal or state grant provides for payments to be made directly on a “reimbursement” basis after payment of expenses, the entire amount of the federal or state reimbursement may be appropriated by the library board without using the additional appropriation procedures under IC 6-1.1-18-5, if the funds are provided or designated by the state or the federal government as a reimbursement of expenditures. [IC 6-1-1.1-18-7.5].

No separate fund for the project or program is required unless the terms of the grant require one.

Matching Grants. Matching Grants should be handled as follows:

When a federal grant or program requires expenditures or “matching” funds to be provided from library funds, an appropriation must be obtained for the amount of such expenditures or local matching funds. Individual program requirements will dictate whether the appropriation should be obtained within the applicable library fund for expenditures there from or whether an appropriation should be obtained within the applicable library fund for a transfer to a required separate fund. This matter should be set out in the terms and conditions entered into between the library officials of the federal agency.

Summary. To summarize, no appropriations of federal funds are necessary:

- when advanced directly from the federal government for a specific purpose prior to making disbursements, and the money is placed in a separate project fund with disbursements made from that fund; or

- when federal funds are received in advance through a state agency for a specific purpose prior to making disbursements and the money is placed in a separate project fund with disbursements made from that fund and there is no state match.

Please keep in mind, if a library wishes to obtain an appropriation for all funds to be spent (i.e., federal, state, and local), there is certainly no prohibition in state statutes.

Depositories used by libraries must be approved as depositories for State funds. The Indiana Board for Depositories' website contains the most recent listing of approved depositories. The list can be accessed at www.in.gov/tos/deposit/.

ASSIGNMENT OF WAGES - WAGE DEDUCTION

IC 22-2-6-1 provides any direction given by an employee to his employer to make a deduction from

wages, shall constitute an assignment such wages subject to the provisions of the act. The term “employer” includes the State of Indiana and any political subdivision thereof. IC 22-2-6-2 outlines the procedures which must be followed and purposes for which deductible assignments may be made.

RECORDING OF AUDIT COSTS

Inquiries have questioned the correct procedure for accounting for city and town audit costs (this does not apply to costs associated with the utility audit).

Indiana Code 5-11-4-3(b) guides this process and states, in part:

“… Immediately upon receipt of the certified statement, the county auditor shall issue a warrant on the county treasurer payable to the treasurer of state out of the general fund of the county for the amount stated in the certificate. The county auditor shall reimburse the county general fund, except for the expense of examination and investigation of county office, out of the money due the taxing units at the next semiannual settlement of the collection of taxes.”

Therefore, counties shall continue to forward Examination of Records (audit costs) payments to the Treasurer of State for city and town audits when billed by the State Board of Accounts. The county general fund shall then be reimbursed from property tax collections of the city or town at the next semiannual settlement.

To properly account for the library’s audit costs the full amount of property and excise taxes (before audit costs) are to be receipted to the appropriate library funds. A disbursement for the Examination of Records is to be posted to library funds.

The Statement of Engagement Costs should be compared to the amount withheld for the Examination of Records to ensure the amounts agree. IC 5-11-4-4 provides that all disbursing offices are authorized to make payments required under this chapter without appropriation. Therefore, the examination of records costs would be considered an unappropriated disbursement.

- B

Budgets

IC 5-1-15 authorizes cities and towns to issue “bonds, notes, evidences of indebtedness, or other written obligations” in fully registered or book entry form.

A question frequently comes up as to whether a depository issuing debt needs to be an approved depository. IC 5-1-15 authorizes political subdivisions to issues “bonds, notes, evidence of indebtedness, or other written obligations” in fully registered or book entry form. Then IC 5-1-15-4 states “The entity may employ any bank or trust company as paying agent or registrar, co-registrar, or depository institution. The bank or trust company need not be a depository bank under IC 5-13, and need not be located within the state of Indiana.

Regardless of any other legal provisions, registrars, registration books, and transfer records related to bonds, notes, debt instruments, or other written financial obligations of any entity are not considered public records. These documents are intended solely for use by the entity itself, as well as any trustee, fiduciary, paying agent, registrar, co-registrar, or transfer agent involved. If a bank’s trust department holds such records, it must not disclose them to the bank’s bond or commercial departments, nor to any of its subsidiaries or those of its parent corporation. (IC 5-1-15-5)

In an effort to facilitate accounting procedures, the State Board of Accounts has issued the following instructions:

- If a bank, trust company, or other financial institution has been employed as a paying agent or registrar, a properly certified listing of bondholders from the paying agent or registrar shall serve as a mailing list for the fiscal officer. There is no requirement for each individual bondholder to file a claim.

- The mailing of the funds for bonds and coupons coming due must be mailed in such a manner to ensure receipt by the bondholder by the due date specific. Personnel of financial institutions state they usually make such mailing by first class mail one to three business days in advance of 4 the due date. They do not mail by certified or registered mail due to costs involved. We suggest you review this with your city or town attorney.

- Since the paying agency or the registrar shall keep a register of ownership of bonds and all bonds and coupons shall be paid when becoming due, we see no reason for the municipality to duplicate those same records maintained by the paying agent or registrar by keeping a bond register. There should be no unpaid outstanding matured bonds or coupons.

- In all instances when employing a bank, trust company, or other financial institutions, be sure to protect the municipality from any liability arising due to any possible errors relating to names and addresses of current bondholders. This protection may be obtained by the financial institution furnishing a bond or insurance in favor of the municipality.

As stated previously, please consult your city or town attorney with questions regarding procedures for registered bonds.

If any reduction is made by the Department of Local Government Finance in the library’s budget and tax levy, the appropriating body should comply with the section of the budget law found in IC 6- 1.1-18-4 which is quoted below:

“Appropriations not to exceed budget – Except as otherwise provided in this chapter, the proper officers of a political subdivision shall appropriate funds in such a manner that the expenditures for a year do not exceed its budget for that year as finally determined under this article.”

- C

Capital Assets

Establishing the Estimated Cost of Capital Assets

Certified Checks for Bonds on Public Contracts

Certified Report of Names, Addresses, Duties, and Compensation of Public Employees

Claims for Payments to State and Federal Agencies

Computing Salaries for Partial Periods

Conflict of Interest Disclosures

Cybersecurity Incidents - Reporting

CAPITAL ASSETS

ESTABLISHING THE ESTIMATED COST OF CAPITAL ASSETS

When it is not possible to determine the historical cost of capital assets owned by a governmental unit, the following procedure should be followed.

Develop an inventory of all capital assets which are significant for which records of the historical costs are not available. Obtain an estimate of the replacement costs of these assets. Through inquiry determine the year or approximate year of acquisition. Then multiply the estimated replacement cost by the factor for the year of acquisition from the Table of Cost Indexes. The resulting amount will be the estimated cost of the asset.

In some cases estimated replacement cost can be obtained from insurance policies; however, if estimated replacement costs are not available from insurance policies, you should obtain or make an estimate of the replacement costs.

If the replacement cost is estimated to be $76,000.00 and the asset was constructed about 1930, then the estimated cost of the asset should be reported as $5,320.00.

Every library should have a complete inventory of all capital assets owned which reflects their acquisition value. Such inventory should be recorded in the Capital Assets Ledger, General Form 369. A complete inventory should be taken at least once a year for good internal control and for verifying account balances carried in the accounting records.

Capitalization Policy

The governing body should establish a capitalization policy that sets a dollar amount as a threshold to be used in determining which items will be recorded.

Land

The records of each library should reflect land owned, its location, its acquisition date and cost (purchase price). Infrastructure A capital asset account for the cost of infrastructure should reflect the location of each road, bridge, tunnel, drainage system, water, wastewater or stormwater system, dam, or lighting system.

Buildings

A capital asset account for buildings should reflect the location of each building and the cost value (being the purchase or construction cost) and, if improvements are made to the building, the cost of such improvements would be included. If a building is acquired by gift, the account would reflect its appraised value at the time of acquisition.

Improvement Other Than Buildings

A capital asset account should reflect the acquisition value of permanent improvements, other than buildings, which have been added to land. Examples of such improvements are fences, retaining walls, parking lots, and most landscaping. The improvements would be valued at the purchase or construction cost.

Equipment

Tangible property of a permanent nature, other than land, buildings and improvements, should be inventoried. Examples include machinery, trucks, cars, furniture, desks, safes, cabinets, etc. The value of such items should be carried in the inventory at the purchase cost.

Construction Work In Progress

Where construction work has not been completed in the current calendar year, the cost of the project should be carried as “construction work in progress.” When the project is completed, it will be placed on the inventory applicable to the assigned asset accounts.

CERTIFIED CHECKS FOR BONDS ON PUBLIC CONTRACTS

Per IC 1-1-7.5-1, whenever state law requires a certified check to accompany bids for public contracts, bidders may instead provide a draft, cashier’s check, or money order, as long as it is issued by a financial institution covered by federal insurance. (link: https://iga.in.gov/laws/2025/ic/titles/1#1-1-7.5-1)

CERTIFIED REPORT OF NAMES, ADDRESSES, DUTIES, AND COMPENSATION OF PUBLIC EMPLOYEES

All libraries must file with the State Examiner on or before January 31, Form 100-R, a Certified Report of Names, Addresses, Duties and Compensation of Public Employees. This report is required by IC 5-11-13 (link: https://iga.in.gov/laws/2024/ic/titles/5#5-11-13 ). Only the business address of each officer or employee listed is to be included on the form.

Such report must indicate whether the library offers a health plan, a pension, and other benefits to full-time and part-time employees.

A change in statute added IC 36-1-30 in 2022 which requires the reporting of donated money used to fund salaries by January 31 each year to the State Examiner. This reporting will be included as part of the 100R reporting. A drop-down box has been added to the right of each individual reported to either select “yes” for donated monies were used or “no” donated monies were not used.

The report is to be filed electronically on the Gateway portal with the State Board of Accounts.

IC 20-33-3 places certain restrictions on work hours for children under 18 years old. For questions regarding child labor laws, please contact the Indiana Department of Labor. The Bureau of Child Labor home page is located at https://www.in.gov/dol/childlabor.htm. The preferred contact information is childlabor@dol.in.gov.

IC 20-33-3-39 through IC 20-33-3-41 list the penalties for violations of the child employment laws which can be as high as $400 per violation.

CLAIMS FOR PAYMENTS TO STATE AND FEDERAL AGENCIES

The State Board of Accounts’ audit position is that when statutory payments are due to state or federal agencies, there is no requirement for the state or federal agency to file an invoice or claim for such payments. This audit position would include payments for social security obligations, public employees’ retirement fund contributions, federal, state, or county taxes withheld, sales tax, and other such amounts due state or federal agencies. The disbursing officer should prepare an accounts payable voucher and attach any copies of payroll deduction reports, federal or state invoices, communications, etc., to document the payment. The accounts payable voucher will provide a posting media indicating to whom paid, fund on which drawn, accounts to be charged, and the approval by the proper boards.

FILING AND DOCKETING CLAIMS

Indiana Code 5-11-10-2 states in part:

“(a) Claims against a political subdivision of the state must be approved by the officer or person receiving the goods or services, be audited for correctness and approved by the disbursing officer of the political subdivision, and, where applicable, be allowed by the governing body having jurisdiction over allowance of such claims before they are paid. If the claim is against a governmental entity as defined in section 1.6 [IC 5-11-10-1.6] of this chapter, the claim must be certified by the fiscal officer.

(b) The state board of accounts shall prescribe a form which will permit claims from two (2) or more claimants to be listed on a single document and, when such list is signed by members of the governing body showing the claims and amounts allowed each claimant and the total claimed and allowed as listed on such document, it shall not be necessary for the members to sign each claim.

(c) Applies to solid waste management districts.

(d) The form prescribed under this section shall be prepared by or filed with the disbursing officer of the political subdivision together with… the supporting invoices or bills...

(e) Where under any law it is provided that each claim be allowed over the signatures of members of a governing body, or a claim docket or accounts payable voucher register be prepared listing claims to be considered for allowance, the form and procedure prescribed in this section shall be in lieu of the provisions of the other law.”

The State Board of Accounts has prescribed General Form No. 364, Accounts Payable Voucher Register, which shall be prepared by, or filed with, the disbursing officer of the library, together with the supporting accounts payable voucher, and all such documents shall be carefully preserved by the disbursing officer as a part of the official records of the office.

If members of the governing body would rather approve and sign each individual accounts payable voucher in lieu of signing the Allowance of Vouchers section of General Form 364, this procedure is acceptable.Indiana Code 5-11-10-1.6 states, in part:

“(c) The fiscal officer of a governmental entity may not draw a warrant or check for payment of a claim unless:

(1) there is a fully itemized invoice or bill for the claim;

(2) the invoice or bill is approved by the officer or person receiving the goods and services;

(3) the invoice or bill is filed with the governmental entity's fiscal officer;

(4) the fiscal officer audits and certifies before payment that the invoice or bill is true and correct; and

(5) payment of the claim is allowed by the governmental entity's legislative body or the board or official having jurisdiction over allowance of payment of the claim…(d) The fiscal officer of a governmental entity shall issue checks or warrants for claims by the governmental entity that meet all of the requirements of this section. The fiscal officer does not incur personal liability for disbursements:

(1) processed in accordance with this section; and

(2) for which funds are appropriated and available.(e) The certification provided for in subsection (c)(4) must be on a form prescribed by the state board of accounts.”

The library fiscal officer has the option of certifying either on each Accounts Payable Voucher or by signing the certification section of the Accounts Payable Voucher Register.

COMPUTING SALARIES FOR PARTIAL PAY PERIODS

A city or town employee on a monthly salary, whose employment with such city or town begins or terminates in the middle of a month, should be paid only for that part of such month that he has worked. If such employee’s work was terminated at the end of the day on January 15, 2015, for example, we believe that he should receive 15/31 of his regular monthly salary for the month of January.

The same procedure should be used for a semimonthly, biweekly, and weekly salaries.

CONFLICT OF INTEREST DISCLOSURES

Indiana Code 35-44.1-1-4 prohibits public servants, their spouses, their minor dependents, and any person who receives more than half of their financial support from a public servant from having a pecuniary interest in contracts or purchases of the government entity for which the public servant works. However, subsection (d) of the statute creates a safe harbor through a conflict-of-interest disclosure. A public servant who completes a disclosure form is protected. The disclosure must be properly filled out, approved in a public meeting, and filed with the State Board of Accounts. There is a link on the Indiana Gateway for Government Units (Gateway) website to upload disclosures (link: https://gateway.ifionline.org/sboa_coi/ ). In order to protect the public servant, the disclosure should be accepted in a public meeting before final action on the contract or purchase and should be uploaded within fifteen days after final action.

We receive a lot of questions asking if certain situations require a conflict-of-interest disclosure. Each situation varies; however, it never hurts to file the disclosure. So, when in doubt, fill it out!

Periodically, we receive questions from units of government wanting to utilize the out-of-state Purchasing Cooperative Sourcewell to make large purchases such as assets without having to advertise for bids. A municipality may only avoid standard procurement procedures and rely on another entity’s purchase price if the original entity’s procurement was fully compliant with the requirements of Indiana Code, in this case Indiana Code 5-22. In general, any cooperative used by an Indiana city or town must comply with Indiana purchasing statutes or public works laws, and we always recommend the local units obtain the written opinion of their city or town attorney. Sourcewell (formerly NJPA) was established under the laws of the State of Minnesota and the SBOA is not aware of any provisions in Minnesota law for a cooperative taking bids for equipment and supplies. Sourcewell’s website notes that their members are able to utilize the cooperative purchasing laws “in their respective jurisdiction.” [ https://www.sourcewellmn.gov/compliance-legal]

Therefore, SBOA would recommend a local unit of Indiana government obtain the written legal opinion of an attorney stating that using a cooperative such as Sourcewell would be in compliance with all Indiana laws. If purchases and/or lease agreements through Sourcewell were identified during an audit of a local governmental unit, we would take an attorney’s written legal opinion into consideration. If items were purchased from an out-of-state cooperative without the support of a written legal opinion, SBOA may take audit exception in the form of a written comment/finding in our Audit Report.

Some of the statutes cited by Sourcewell to support Indiana cities and towns purchases are IC 5- 22-10-5, IC 5-22-10-12, and IC 5-22-10-14, special purchasing laws. If justifying a purchase from Sourcewell or other cooperative as a special purchase, cities and towns should ensure they comply with Indiana Code, including (but not limited to) retaining documentation supporting the special purchase. IC 5-22-10 et seq. For instance, Sourcewell cites IC 5-22-10-5 as providing a special purchase can be made “when there exists a unique opportunity to obtain supplies or services at a substantial savings”. Because some of the terms in this statute, namely “unique opportunity” and “substantial”, are not defined, our position is when an Indiana governmental unit is obtaining supplies using IC 5-22-10-5 as the authority, they should obtain a written legal opinion from their attorney that the purchase complies with this statute. SBOA would take the opinion into consideration during an audit.

Regarding IC 5-22-10-12, this statute provides when the market structure is based on price, a local unit of government can make a purchase when they are able to receive a dollar or percentage discount “of the established price”. In the case of a bid and price offered by Sourcewell, we are unclear as to what the discount of the “established price” would be. Is the bid price the “established price”? Is there a discount off of the bid price? Is the bid price considered the discount – if so, what would the established price be? Our audit position is when an Indiana governmental unit is obtaining supplies using IC 5-22-10- 12 as the authority, they should obtain a written legal opinion from their attorney that the purchase complies with this statute. SBOA would take a written legal opinion into consideration during an audit.

Regarding IC 5-22-10-14, this statute provides the purchasing agent may make a purchase when they determine, in writing, that the supplies can be purchased at prices equal to or less than prices stipulated in current federal supply service schedules established by the federal General Services Admin and it’s advantageous to the government body’s interest in efficiency and economy. Because the purchasing agent at the local government has to make a written determination the prices are equal to or less than federal supply service schedules and that it’s to their advantage because of “efficiency and economy”, we would take the written legal opinion of any attorney that making a purchase under this statute would comply with Indiana’s laws.

The library board shall establish a fee schedule by ordinance for the certification and copying of documents. For questions on fees please see IC 5-14-3-8 (d)

(link: https://iga.in.gov/laws/2025/ic/titles/5#5-14-3-8)

The State Board of Accounts will not take exception to the use of credit cards by a governmental unit provided the following criteria are observed:

- The governing board must authorize credit card use through an ordinance or resolution, which has been approved in the minutes.

- Issuance and use should be handled by an official or employee designated by the board.

- The purposes for which the credit card may be used must be specifically stated in the ordinance or resolution.

- When the purpose for which the credit card has been issued has been accomplished, the card should be returned to the custody of the responsible person.

- The designated responsible official or employee should maintain an accounting system or log which would include the names of individuals requesting usage of the cards, their position, estimated amounts to be charged, fund and account numbers to be charged, date the card is issued and returned, etc.

- Credit cards should not be used to bypass the accounting system. One reason that purchase orders are issued is to provide the fiscal officer with the means to encumber and track appropriations to provide the governing board and other officials with timely and accurate accounting information and monitoring of the accounting system.

- Payment should not be made on the basis of the statement or a credit card slip only. Procedures for payments should be no different than for any other claim. Supporting documents such as paid bills and receipts must be available. Additionally, any interest or penalty incurred due to the late filing or furnishing of documentation by an officer or employee should be the responsibility of that officer or employee.

- If properly authorized, an annual fee may be paid.

- If a vendor charges a convenience fee for use of the card, such fee may be paid to the vendor.

If properly authorized, an annual fee may be paid.

Recent legislative changes allow a taxing unit to deposit distributions of Financial Institutions Tax (FIT) and Commercial Vehicle Excise Tax (CVET) in “any fund maintained by the taxing unit,” and the distributions may be used for any purpose allowed by law. [IC 6-5.5-8-2(c); IC 6-6-5.5-20(h)]. While this broad language benefits taxing units by allowing them to receipt the funds where they will be most effectual, if a unit does not take steps to ensure the distribution is adequately tracked, critical audit findings may result.

During audit, it is imperative that SBOA be able to identify into which fund the distributions are receipted. Therefore, if a unit receipts FIT and CVET distributions into any fund other than the General Fund, the legislative body of the unit must identify into which fund the distributions will be receipted. The fund identification must be made prior to the distribution and may be done through ordinance, resolution, or vote (memorialized in meeting minutes). If the distributions are receipted into the General Fund, the unit need not adopt an ordinance, resolution, or vote.

REPORTING CYBERSECURITY INCIDENTS

House Enrolled Act 1169 (2021) added IC 4-13.1-2-9 as a new section to the Indiana Code which requires political subdivisions, as defined in IC 36-1-2-13, to report any cybersecurity incident using their best professional judgement to the Indiana Office of Technology (IOT) without unreasonable delay and not later than two business days after discovery of the cybersecurity incident. A cybersecurity incident may consist of one or more of the following categories of attack vectors: (1) Ransomware, (2) Business email compromise, (3) Vulnerability Exploitation, (4) Zero-day exploitation, (5) Distributed denial of service, (6) Web site defacement, (7) Other sophisticated attacks as defined by the chief of information officer and that are posted on the officer’s Internet web site. (IC 4-13.1-1-1.5)

Cybersecurity incidents can be reported on IOT’s web site at the following webpage. https://www.in.gov/cybersecurity/report-a-cyber-crime/

- D

Dedicated Fund Transfers To Rainy Day Fund

Deferred Compensation Plans - PERF

DEDICATED FUND TRANSFERS TO RAINY DAY FUND

The term “dedicated fund” has been used throughout the state, and the officials have asked for a meaning of that term as it relates to Rainy Day transfers. Our audit position is as follows:

Dedicated funds are a generic term not defined in statute but is generally construed to mean a fund set aside for a specific purpose. For purposes of transferring to the Rainy Day fund, we are limiting our position to those dedicated funds that result from statutory authority but do not include home rule funds or clearing accounts. Debt service funds are already specifically prohibited from transfer in the Rainy Day statute and so are not considered here either.

In order to determine whether or not monies in a fund may be transferred to the Rainy Day fund, an analysis would need to be made of the authority creating the fund in light of IC 36-1-8-5.1. It would be up to the political subdivision to show SBOA how money transferred to the Rainy Day fund met the criteria for transfer. However, we can provide general guidance based on our position.

Tax levy and LOIT funds have different criteria than other statutorily created funds in regard to transferring to the Rainy Day fund. The key words to tax levy and LOIT funds are whenever the purposes of a tax levy have been fulfilled and unencumbered balance remains in the fund and unless a statute provides that it be transferred otherwise. In general, it will be up to the unit of government to define when the purposes have been fulfilled. There are certain funds that are raised by levy that have very specific language that the balance may not be transferred, such as the assessment fund. For those funds, we would take exception if there were a transfer to Rainy Day fund. Also, for some cumulative funds such as those found under IC 6-1.1-41-1, balances in these funds may only be transferred to the General fund per IC 6-1.1-41-15 and again we would take exception if they were transferred to the Rainy Day fund.

For other funds, the statute allows for the transfer to Rainy Day fund if the funding source is specified in the ordinance or resolution and the transfer is not otherwise prohibited by law. It is our general position that if the statute provides definitive restrictive language on the use of the funds or that the balance is not to be transferred, whether Rainy Day fund is specifically included or not, that the monies are not to be transferred to Rainy Day fund. For example, MVH funds [IC 8-14-1-3(1)] provide that for cities or towns, no part of such sum shall be used for any other purpose than for the purposes defined in this chapter. IC 8-14-1-4 provides similar restrictions for counties. For LRS funds, IC 8-14- 2-5 defines the exclusive uses of the funds, and IC 8-14-2-7 further restricts transfers of certain towns’ LRS to General fund after these monies have not been spent for 24 months. Transfers from MVH and LRS (or any other fund with similar statutory restrictions) to Rainy Day would be prohibited and we would take exception if monies were so transferred. Where there is not such restrictive language or prohibition of transfer, we will consider the unit attorney’s written opinion as to why the other fund would not fall under the category of prohibited and so be transferred.

DEFERRED COMPENSATION PLANS - PUBLIC EMPLOYEES RETIREMENT FUND

IC 5-10-1.1-1 allows cities and towns to contribute amounts before January 1, 1995 and continue or begin to contribute amounts after January 1, 1995, to a nonqualified deferred compensation plan on behalf of eligible employees, subject to any limits and provisions under section 457 of the Internal Revenue Code. IC 5-10-1.1-7 allows cities and towns to offer to their employees both the state deferred compensation plan and another deferred compensation plan that uses private vendors.

IC 5-10.2-2-1 further provides that it does not prohibit a city or town from establishing and providing before January 1, 1995 and continuing to provide after January 1, 1995, retirement, disability, and survivor benefits to the employees of the city or town if the city or town took action before January 1, 1995, and was not a member of the Public Employees’ Retirement Fund (PERF) on January 1, 1995.

A city or town has no authority to establish a local pension plan by ordinance, resolution, or contract after January 1, 1995, without specific statutory authority. PERF, deferred compensation plans, police and fire pension plans, and utility employee pension plans are all authorized by statute.

CONTRIBUTIONS, DONATIONS, GIFTS

Library Gift Funds

Pursuant to IC 36-12-3-11(a)(5), money or securities accepted and secured by the library board as a grant, gift, donation, endowment, bequest or trust may be set aside in a separate fund or funds, and shall be expended, without appropriation, in accordance with the conditions and purposes specified by the donor.

Definitions

The following definitions apply to the gift fund."Restricted" gifts are those to which the donor has attached terms, conditions and purposes. These may be quite specific or very general, such as "books", etc.

"Unrestricted" gifts are those to which the donor has not attached terms, conditions or purposes.

Sources

Grants, gifts, donations, endowments, and bequests (hereinafter required to collectively as "gift"). It is the prerogative of the Board to accept or reject any gift.Income in the form of tax receipts, fees, sale of library property, rental, etc. may not be receipted into the library gift fund.

Accounting

Gifts may be handled in any of the following ways:Operating Fund. If the gift is unrestricted, the library may receipt the gift into the library operating fund.

A. If deposited into the library operating fund, the gift money must be budgeted, appropriated (in the regular budget or by additional appropriation) in the manner prescribed, including advertising and approval by the Department of Local Government Finance. Any gift receipted to the Library Operating Fund must be posted to Columns A-1 and B-1 of the Library Financial and Appropriation Record. Disbursements are to be posted to Columns A-2 and B-2 and also in the applicable appropriation columns.

B. Gift money placed into the library operating fund may be spent as determined by the library board within the scope of its statutory authority. It is to be expended as other funds of the library.

C. Gift money placed in the library operating fund does not accumulate and must be spent or encumbered within the fiscal year or it will revert to the library operating fund balance and must be re-appropriated before the disbursement.

Separate Fund or Funds. A separate fund may be established for each gift; gifts for like purposes may be receipted into separate funds for each purpose; or all gifts may be placed into one "Gift Fund".

Use of Gift Funds

If the library board chooses to receipt any gift (restricted or unrestricted) to a separate fund or funds, the following will apply.1. Gift money may be spent without budgeting or appropriation.

2. If restricted, it must be spent according to the donor's restrictions.

3. If unrestricted, it may be spent as determined by the library board within the scope of its statutory authority.

4. The fund or funds may be accumulated and may be spent at any time the library board determines, unless otherwise required by the terms of the donor.Accounting

If all gifts are placed into a "Gift Fund", the following accounting will be necessary:1. A subsidiary record to keep track of the disbursements relating to each gift must be maintained.

2. The subsidiary record may be kept on any appropriate commercial form or columnar worksheet, such as a cash journal.

3. A separate sheet should be opened in this subsidiary record for each restricted gift. Entries to this separate sheet would include the receipt of the restricted gift and disbursements chargeable to each gift including the date, amount and explanation of each.

4. Income from the interest on gifts may be receipted into the same fund in which the principal of such gift has been receipted provided it is to be used for the same purpose as the principal. However, if, under the terms of the trust, the principal must be held in trust in perpetuity and only the income used by the governmental unit, there should be two accounts established, one designated as "Trust Principal" and the other designated "Trust Income."

5. Unrestricted gift fund monies may be invested as part of the "total monies on deposit," and the interest thereon receipted to the library operating fund.

6. All funds, regardless of source, are deposited by the treasurer in only one bank account in each designated depository.

7. Receipts to and disbursements from a separate gift fund or funds may be posted in columns D-1, D-2, E-1, E-2, and E-3 or F-1, F-2 , and F-3 on the Library Financial and Appropriation Record if such columns are not being used. If space for additional funds is needed, the optional flyleaf sheet (Library Form No. 1C) should be used. This form contains columns for four additional funds.Community Foundation Transfers

Gifts to the library may be set aside in an account with a nonprofit corporation established for the sole purpose of building permanent endowments within a community (referred to as a "community foundation"). The earnings on the funds in the account, either deposited by the library or accepted by the community foundation on behalf of the library, may be distributed back to the library for disbursement, without appropriation, in accordance with the conditions and purposes specified by the donor. A community foundation that distributes earnings under this clause is not required to make more than one (1) distribution of earnings in a calendar year. [IC 36-12-3-11(a)(5)(B)]This action must be authorized by the library board by resolution. Note that the statute does not provide for a return of principal to the library.

- E

Emergency Repairs - Public Works

Establishing the Estimated Cost of Capital Assets

Examination of Records and Statement of Engagement Cost

Indiana Code 36-12-3-16.5 covers the payment of claims via electronic transfer. Note that subdivision (c) requires a unit to utilize the normal claims process, even for electronic funds transactions. Among other limitations, this means that it is impermissible for a third party to “pull” money out of a unit’s bank account. Instead, the fiscal agent must initiate or direct the unit’s financial institution to disburse the funds.

EMERGENCY REPAIRS - PUBLIC WORKS

The Indiana Code includes special purchasing provisions in emergency public work situations. IC 36-1-12-2 provides a definition of public works and IC 36-1-2-4.5 provides a definition of an emergency.

Whether or not the political subdivision can declare a situation an emergency in order to bypass the bidding requirements of the public works statutes is fact specific. IC 36-1-12-9 provides for the governing body to contract for public works without advertising bids or quotes. We would recommend working with an attorney in order to maintain compliance with these statutes.

During an audit we would be looking for the formal declaration of emergency noted within the official board minutes and the names of the persons invited to bid or provide quotes. Documentation should be maintained including the original bids or quotes and the board’s determination of the project award. Any insurance proceeds received should be receipted into the fund the originally paid the cost and per IC 6-1.1-18-7 would be considered appropriated for 12 months after received for the sole purpose of repairing or replacing the property that was insured. Any additional funds above the insurance proceeds would need to follow normal additional appropriation procedures.

As economic conditions fluctuate and budgets tighten, political subdivisions face growing pressure to manage costs with precision and plan audits more strategically. This article takes a closer look at how the Statement of Engagement Costs can serve as a vital tool for forecasting expenses for future audit costs.

Rates

If necessary, our rates are amended annually and submitted to the audit committee for review to ensure the cost of performing an audit does not exceed an amount equal to eighty percent (80%) of the market rate cost. Our rates are not changing for the upcoming fiscal year and can be found on our website: https://www.in.gov/sboa/about-us/our-rates/.

Statement of Engagement Costs

At the end of an audit engagement, the State Board of Accounts sends a Statement of Engagement Costs to each political subdivision, including the County. This statement details a summary of the engagement, including the number of days spent on the audit, the daily/hourly rate, and any report processing fees. This statement is not an invoice that is to be paid by the entities.

The process for the county to pay the examination fees is outlined in statute:

“The state examiner shall certify to the auditor of each county the amount chargeable to each taxing unit within the county for the expense of its examinations as provided in this chapter. Immediately upon receipt of the certified statement, the county auditor shall issue a warrant on the county treasurer payable to the treasurer of state out of the general fund of the county for the amount stated in the certificate. The county auditor shall reimburse the county general fund, except for the expense of examination and investigation of county offices, out of the money due the taxing units at the next semiannual settlement of the collection of taxes.”

[IC 5-11-4-3(b)].

The statute does not specifically restrict the use of any of the funds taken from settlement and a distribution is not viewed the same as a disbursement from the fund so we will not take exception to taking a distribution from a fund other than general. We do however recommend avoiding taking from the debt funds without discussing with the unit first as these funds are levied for the exact amount needed to cover a political subdivisions debt.

If the county knows or reasonably believes that it does not have on hand or will not have collected enough taxes by the next distribution date for a taxing unit included on the examination of records billing, the county auditor will send the certified statement to the taxing unit for payment of costs. The taxing unit should contact the State Board of Accounts to arrange for payment of examination costs directly to the State Board of Accounts. The cost must be paid prior to the next audit. If the audit costs due to the State Board of Accounts are not paid prior to the next audit, the independence of the State Board of Accounts is impaired and future audits are delayed.

When the taxing unit is required to pay audit costs directly, these costs may be allowed to be paid from funds other than General fund. For example, Rainy Day funds could be used if your Rainy Day Ordinance allows for the payment of audit costs. Payment of audit costs does not require an appropriation per IC 5-11-4-4, which states:

“All disbursing officers be and they are hereby authorized to make all disbursements or payments required to be made under the provisions of this chapter without any appropriation being made therefor.”

Planning for Future Audits

For political subdivisions, planning for audit costs is a strategic exercise that ensures transparency, compliance, and fiscal responsibility. Whether preparing for a routine financial audit or a more complex single audit of federal programs, understanding the drivers of audit costs can help entities plan effectively and avoid surprises.

There are a number of key factors to consider when planning for audit costs:

- Amount of federal assistance disbursed during the audit period - If you have expended $1,000,000 or more of federal awards (whether the award is direct or passed through another entity) in a year, the taxing unit is required to have a single audit conducted in accordance with the Federal Office of Management and Budget’s Uniform Guidance. Single audits require an annual audit. If your unit does not need a Single Audit, there may be a longer time between your examinations.

- Tip – Review your Schedule of Expenditures of Federal Awards (SEFA) to identify the amount of federal assistance disbursed over the threshold.

- Tip – If you will not need a single audit, the anticipated audit costs will be less than audit costs for a year that needs a single audit.

- Tip – Review the grant agreement for any large federal grant to determine whether grant funds may be used to pay a portion of the audit costs.

- Number of years in the audit period - Multi-year audits or audits covering extended periods require an increased number of audit days and staff hours needed for the engagement.

- Tip – During the entrance conference, confirm the number of years the audit period covers.

- Prior period audit costs – Past audit costs offer a benchmark for estimating future costs. The prior Statements of Engagement Costs outline the number of years included in the audit, hourly rates, number of days, and fees, which calculate the total cost.

- Tip - Review prior statements of engagement costs to form a baseline for future engagement costs. Current rates and fees are included on our website: https://www.in.gov/sboa/aboutus/our-rates/.

- Entrance and exit conference documentation – Field examiners are required to provide estimates of audit costs at the entrance and exit conference of each engagement. These forms give insight into the estimated time spent on the audit.

- Tip - Use entrance and exit forms to calculate an estimated total cost of the audit. Multiply the number of hours spent by the current daily rate to estimate future costs, plus fees for processing and technology costs. If a federal audit is performed, you will also have to add the number of federal programs audited: multiply the number of hours for each federal program by the full direct cost rate.

- Complexity and Readiness of Financial Records – Well-organized records reduce audit time; disorganized or incomplete records increase it. The more issues and difficulty encountered during the audit increase the length of the engagement.

- Tip - Invest in pre-audit preparation. Clean books and reconciled accounts can reduce audit hours and overall cost.

- Prior period comments and follow-up - Prior period audit comments can significantly impact future audit costs, especially if issues remain unresolved. These comments often lead to followup, the possibility of expanded testing, and increased documentation requirements, all of which increase audit time and costs. Addressing them proactively not only demonstrates a commitment to financial integrity but also reduces the risk profile of the engagement.

- Tip – Prior period comments should be reviewed prior to the next audit and corrected. Clear documentation of corrective actions can streamline the audit process and help control costs.

Planning for audit costs isn’t just about numbers—it’s about understanding your entity’s financial landscape and anticipating changes. By analyzing federal assistance, audit history, and examiner documentation, a political subdivision can plan ahead for realistic audit costs. Please reach out to the Directors if you want additional guidance on planning for audit costs.

ESTABLISHING THE ESTIMATED COST OF CAPITAL ASSETS

When it is not possible to determine the historical cost of capital assets owned by a governmental unit, the following procedure should be followed. Obtain an estimate of the replacement costs of these assets. Through inquiry determine the year or approximate year of acquisition. Then multiply the estimate replacement cost by the factor for the year of acquisition from the Table of Cost Indexes. The resulting amount will be the estimated cost of the asset. In some cases, estimated replacement cost can be obtained from insurance policies; however, if estimated replacement costs are not available from insurance policies, you should obtain or make an estimate of the replacement costs.

If the replacement cost is estimated to be $76,000.00 and the asset was constructed about 1930, then the estimated cost of the asset should be reported as $3,800.00 ($76000 x .05).

EXAMINATION OF RECORDS AND STATEMENT OF ENGAGEMENT COST

At the end of an audit engagement the State Board of Accounts sends a notice of Statement of Engagement Cost to each political subdivision, including the County. This statement details a summary of the engagement including the number of days spent on the audit, the daily/hourly rate, and any report processing fees. We would like to point out that this statement is not an invoice that is to be paid by the entities.

A separate invoice for payment of these audit costs will be sent to the County for payment in accordance with IC 5-11-4. Immediately upon receipt of the certified statement, the county auditor shall issue a warrant on the county treasurer payable to the treasurer of state out of the general fund of the county for the amount stated in the certificate. The county auditor shall reimburse the county general fund, except for the expense of examination and investigation of county offices, out of the money due the taxing units at the next semiannual settlement of the collection of taxes.

If the county reasonably believes or knows that it does not have on hand or will not have collected enough taxes by the next distribution date for a taxing unit included on the examination of records billing, then the county auditor will send the certified statement to the taxing unit. The taxing unit should then contact the State Board of Accounts for directions on paying for the cost of the examination directly to the State Board of Accounts instead of using settlement. It is important that the cost be paid off prior to the next audit. If the audit costs, due the State Board of Accounts, are not paid prior to the subsequent audit, it impairs the independence of the State Board of Accounts. This will delay future audits.

As the amount of federal funding to local governments has increased, so has the need for single audits and more frequent audits, which has helped drive up audit costs. We are now beginning to see this result in semiannual tax distributions that are not sufficient to pay the audit costs. It is important to plan and budget accordingly for these costs. It might be beneficial once an examination of records has been completed for the taxing unit to go directly to the county auditor if sufficient taxes will not be collected to pay the estimated costs of the examination of records. Having this conversation before receiving the certified statement from the county auditor can prepare the taxing unit for the payment of these costs. You can discuss with your field examiner during the exit how you may best meet the costs. This may involve the use of other funds, such as Rainy Day, or if there are ARPA funds remaining under the revenue loss category, those can also be used to pay audit costs. If you have questions after the exit, please feel free to reach out to your State Board of Accounts Director for further assistance in looking for funds that can pay the audit costs.

When determining how these costs will be paid, it is also important to plan for the next year. During this determination, take into consideration the amount of federal assistance that you have disbursed during the year. If you have expended $750,000 or more of federal awards (whether the award is direct or passed-through another entity) in a year the taxing unit is required to have a single audit conducted in accordance with the Federal Office of Management and Budget’s Uniform Guidance. Single audits require an annual audit. If your unit does not need a Single Audit, there may be a longer time between your examinations. Since these costs could become an annual expense for the taxing unit, future budgets would need to be adjusted for those costs.

IC 5-11 4-3(b) is the statute that explains the process of the county paying for exam fees, which states: “The state examiner shall certify to the auditor of each county the amount chargeable to each taxing unit within the county for the expense of its examinations as provided in this chapter. Immediately upon receipt of the certified statement, the county auditor shall issue a warrant on the county treasurer payable to the treasurer of state out of the general fund of the county for the amount stated in the certificate. The county auditor shall reimburse the county general fund, except for the expense of examination and investigation of county offices, out of the money due the taxing units at the next semiannual settlement of the collection of taxes.”

The statute does not specifically restrict the use of any of the funds taken from settlement and a distribution is not viewed the same as a disbursement from the fund so we will not take exception to taking a distribution from a fund other than general. We do, however, recommend avoiding taking from the debt funds without discussing with the unit first, as these funds are levied for the exact amount needed to cover a political subdivisions debt.

As always, we encourage the counties to work with their political subdivisions to keep everyone operating effectively and efficiently

- Amount of federal assistance disbursed during the audit period - If you have expended $1,000,000 or more of federal awards (whether the award is direct or passed through another entity) in a year, the taxing unit is required to have a single audit conducted in accordance with the Federal Office of Management and Budget’s Uniform Guidance. Single audits require an annual audit. If your unit does not need a Single Audit, there may be a longer time between your examinations.

- F

- G

The SBOA GAAP Efficiency Team (GET) serves cities, towns, and special districts that prepare financial statements following generally accepted accounting principles. GET serves as a liaison between local officials and their audit teams to resolve questions and concerns regarding the audit process and GASB and SBOA guidance. Per I.C. 5-1-11.5, municipalities with populations of more than 75,000 are required to file annual financial reports in accordance with GAAP to issue new bonds. This statute currently applies to eight Indiana cities. Five other Indiana cities currently report on the GAAP basis voluntarily.

Local units are reminded that per 2 CFR 200.512, the federal deadline for units to submit audited reports to the Federal Audit Clearinghouse is the earlier of 30 days after receipt of the report or nine months after the end of the audit period. GET anticipates that 11 Indiana cities reporting on the GAAP basis will meet the September 30, 2024, deadline.

Cities required to report in accordance with GAAP: Bloomington, Carmel, Evansville, Fishers, Fort Wayne, Hammond, Indianapolis, South Bend

Cities reporting on GAAP voluntarily: Greenwood, Jeffersonville, Lafayette, Mishawaka, Noblesville

The following cities have already submitted their reports to FAC for 2023: Carmel, Fishers, Fort Wayne, Greenwood, Indianapolis, Noblesville

Anticipated on time: Evansville, Hammond, South Bend, Jeffersonville, Mishawaka

Late: Bloomington, Lafayette

Information Related to Previous LIT Guidance from SBOA Memorandum dated July 12, 2023

We are issuing a change in guidance for preparation of your next GAAP financial statements. Complete SBOA guidance is below. Almost all of the July 12, 2023 Memorandum is unchanged by the information below. The only changes are contained within the text boxes. Therefore, if you are familiar with the Memorandum from last year regarding LIT reporting you will want to concentrate on the areas within the text boxes for the changes. These changes are minor and pertain to reporting LIT Receivable within the fund financial statements. Other reporting recommendations have not changed.

GAAP Reporting of Local Income Tax

Unified Local Income Taxes (LIT) are derived tax revenues. Therefore, a receivable should be recognized in the period when the exchange transaction on which the tax is imposed occurs or when resources are received, whichever occurs first. Revenue net of estimated refunds and estimated uncollectible amounts, is recognized in the same period the receivable is recognized in accrual based financial statements (GASB Cod. N50.113). For modified accrual (governmental fund statements) revenue will be recognized when they become available and measurable. This means the Unified Local Income Taxes recognized as an asset and revenues in the current year are based on wages/income to the taxpayer from the current year.

The way the LIT statute is written and the GAAP standards that must be applied for asset and revenue recognition are difficult to align for this tax as the actual tax amount net of refunds and uncollectible amounts are not known at the time financial statements are prepared. As time passes, additional information about actual taxes imposed and collected continues to become available and can be used to adjust estimates. Therefore, it is important to determine what we know about the timing of state distributions to local governments for LIT as well as the estimated amounts of LIT.

One might think state distributions would be delayed until the tax imposed is collected and returns are processed by the State. However, that is not what is prescribed by Indiana Code. IC 63.6-3 requires the adopting body for LIT to adopt, increase, decrease, or rescind a tax or tax rate by ordinance. The timing of the ordinance passage determines the date of the imposition of the income tax and therefore, the date the asset and revenue should be included in the financial statements of the local government.

Based on IC 6-3.6-9-8, the State is distributing estimated LIT collections either current with the taxable transactions, when the effective date is January 1 of the following year, or within three months, when the effective date of the tax is October 1 of the current year. Per IC 6-3.6-9-16, the county shall allocate and distribute LIT to the appropriate entities upon receipt of each monthly distribution from the State. Therefore, other local governments are also receiving LIT current or within three months of imposition.

Each local government must use the information available to also determine the amount of assets and revenues appropriate to report as financial statements are prepared each year. The State provides much of the information you will find useful for calculating amounts for LIT journal entries and financial statement preparation.

We recommend the modified accrual statements recognize LIT revenue in the amount received during the year in monthly and supplemental distributions. Because of the language in GASB Cod. § N50.108, we believe the Asset recognition in the modified accrual statements would be the same as in the full accrual statement. Our recommendation for the calculation of the LIT Receivable amount is in the following paragraph and is the same for both the modified accrual and full accrual financial statements. Although the underlying derived tax transaction has occurred, revenue recognition in the modified accrual statements for the related LIT Receivable would only occur in these statements if the resources were also available, which we do not believe is the case with LIT. Therefore, the receivable would be posted as an asset with a corresponding deferred inflow of resources-unavailable revenue.

Our recommendation for the full accrual statements is for management to consider the supplemental distribution of LIT for the ensuing year. Because the supplemental distribution equals the amount of the unencumbered balance from two years prior that is determined to be in excess of 15% of the certified distribution minus any supplemental or special distributions that have not yet been accounted for in the last known balance of the county’s trust account, you should also consider the amount that equals 15% of certified distributions in your estimations for booking the appropriate LIT receivable and additional revenue.

If you choose another methodology to estimate and book the LIT receivable, deferred inflows, and revenue in your financial statements, that methodology must have a reasonable basis and be supported by documentation that can be audited.

- H

HEALTH SAVING ACCOUNT PAYMENTS

It has come to our attention that some units are not using payroll withholding funds to account for the employee directed Health Savings Account payments. Instead, the units make direct deposits to the Health Savings Accounts in a similar manner to the process of making net pay direct deposits to the employee’s bank account. Historically, our audit position has been to take exception to this accounting practice because all payroll transactions were not being recorded in the financial records. The State Board of Accounts has revised the audit position on this process and we will not take audit exception to amounts approved by employees being deposited directly into Health Savings Accounts without the use of a payroll withholding fund, provided the following criteria are observed:

- Unit is following state and federal guidelines of Health Savings Accounts;

- Reports of amounts deposited into Health Savings Accounts are produced in detail by employee for each individual payroll period and maintained for audit; and

- Amounts deposited into Health Savings Accounts (employee and employer share) are approved by the governing board.

- I

Interest on Delinquent Accounts

Internal Control Training Materials

During this last quarter, we received an increase in questions relating to insurance proceeds. Insurance proceeds would need to be receipted into the fund which originally paid for the asset. Additionally, these funds would not need to be appropriated if being spent within the year of receipt. However, if the cost to demolish, rebuild, or purchase the new asset exceeds the insurance amount, then you would need to appropriate those funds in excess of the insurance proceeds. Indiana Code 6-1.1-18-7 discusses insurance proceeds.

INTEREST ON DELINQUENT ACCOUNTS

Since existing statutes (and past court decisions) require that funds and appropriations must be available prior to entering into a contract, there is no reason why contractual payments should not be made in a timely fashion unless there is a dispute regarding the services rendered or materials delivered.

Please review your city or town’s purchasing and subsequent claim payment procedures to ensure you are not going to be in a position where you may incur late payment charges.

From the Department of Revenue, Departmental Notice #3 issued in October 2025 effective January 1, 2026:“Pursuant to IC 6-8.1-10-1, the rate of interest for an underpayment of tax and an excess tax payment is the percentage rounded to the nearest whole number that equals two percentage points above the average investment yield on state general fund money for the state’s fiscal year ending June 30, 2025, excluding pension fund investments, as provided by the State Treasurer’s office. The rate of interest for an underpayment of tax and an excess tax payment for calendar year 2026 will be 7%.”

In addition, we have included a historical list of calculated percentages for the last 10 years. This information can be found on the Department of Revenue website (www.in.gov/dor).

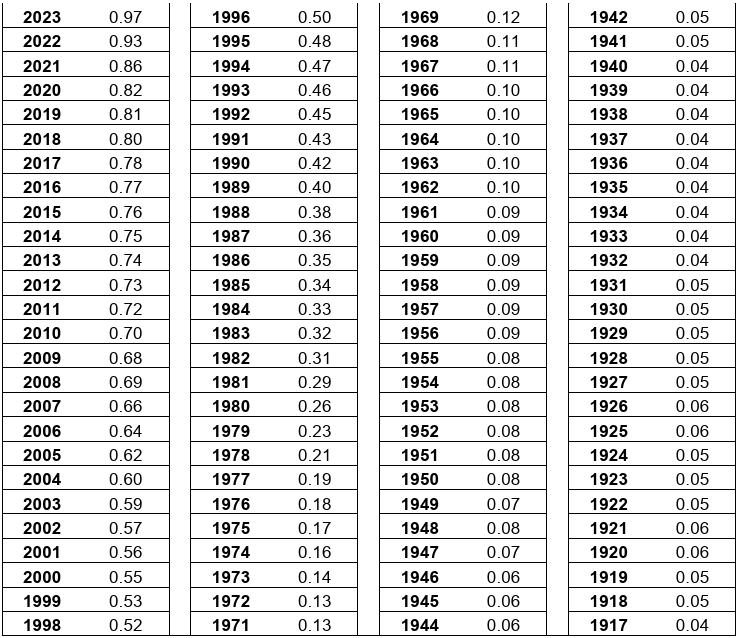

Historical Interest Rate List

Year Overpayments Delinquent Payments 2017

2018

2019

2020

2021

2022

2023

2024

2025

20263%

3%

3%

4%

4%

3%

2%

4%

6%

7%3%

3%

3%

4%

4%

3%

2%

4%

6%

7%INTERNAL CONTROL TRAINING MATERIALS

Internal control training materials

Indiana Code § 5-11-1-27(f) states:

Not later than November 1, 2015, the state board of accounts shall develop or designate approved personnel training materials as approved by the audit committee, to implement this section.

The State Board of Accounts has developed the following training materials on internal controls:

1. Uniform Internal Control Standards for Indiana Political Subdivisions manual by the State Board of Accounts.

2. Numerous webinars containing the phrase “internal control” posted on the SBOA’s website.

3. Live presentations by the SBOA at annual called meetings and conferences around the state.

The State Board of Accounts has designated the following training materials on internal controls:

4. Internal Control – Integrated Framework (2013) by the Committee of Sponsoring Organizations of the Treadway Commission (COSO).

5. Guidance papers, principles, or frameworks on Governance and Operational Performance, Internal Controls, Enterprise Risk Management, or Fraud Deterrence by COSO.

6. Standards for Internal Control in the Federal Government (the “Green Book”) by the Comptroller General of the United States.

- J

- K

- L

Library Improvement Reserve Fund (LIRF)

Each year the Department of Local government Finance will certify to each library figures which show one hundred two percent (100%) of the tax levy for each fund. If the property taxes received exceed one hundred two percent (100%) of the levy, the excess shall be receipted to a levy excess fund. However, if the amount is less than one hundred dollar ($100), no transfer is required. Please see IC 6-1.1-18.5-17 for more information.

LIBRARY IMPROVEMENT RESERVE FUND (LIRF)

Recently we had inquiries from multiple libraries wanting to close out their LIRF fund. The LIRF fund is a statutory fund, so libraries would have to keep these funds. However, libraries could spend the fund down to zero and then not utilize the LIRF fund.

Another question posed was whether libraries could transfer these funds to their Rainy-Day Fund. Libraries are required to use the money in the LIRF for future capital expenses as described in IC 36-12-3-11 (a) (4). Therefore, these funds cannot be transferred to the Rainy-Day fund, since the ordinance establishing the Rainy-Day fund could have a broad list of allowable expenditures and not as narrow as the LIRF requirements.

- M

The following are excerpts from the Amended State Examiner Directive 2015-6 regarding a Materiality Threshold for reporting irregular material variances, losses, shortages, and thefts under IC 5-11-1-27(j). Note that this materiality threshold does not apply to a Report of Misappropriation under IC 5-11-1-27(l) as discussed in the previous article.

Indiana Code § 5-11-1-27(j) states: “All erroneous or irregular material variances, losses, shortages, or thefts of political subdivision funds or property shall be reported immediately to the state board of accounts…“.

In general, each political subdivision must develop their own policy on materiality because the causes of irregular variances, losses, shortages, and thefts are as broad and varied as the political subdivisions in which the incidents occur. For example, a $500 variance in Fort Wayne is not necessarily as concerning as a $500 variance in Pershing Township, Jackson County. On the other hand, a $100 variance in Fort Wayne that occurs every Friday may be material. Moreover, each political subdivision is the best determiner of the qualitative and quantitative factors unique to the unit in arriving at materiality.

Political subdivisions must recognize that variances, losses, shortages, and thefts may occur. If an incident occurs, it is imperative that the political subdivision have a policy in place that outlines the steps to be taken. Such a policy must include a materiality threshold at which point the political subdivision reports incidents to the State Board of Accounts.

The policy must be detailed, and it is essential that materiality thresholds distinguish between incidents involving cash and other types of assets. The policy needs to address maintenance of documentation and resolution of incidents that do not meet the materiality threshold…

If a political subdivision does not develop a policy on materiality, then the threshold is $0.00 and the political subdivision is required to report all irregular variances, losses, shortages, and thefts to the State Board of Accounts…

When an irregular variance, loss, shortage, or theft is determined material pursuant to a political subdivision’s policy on materiality (or, if no policy on materiality is developed, whenever there is any incident of irregular variance, loss, shortage, or theft), the subdivision must report the incident to the State Board of Accounts. On the State Board of Accounts’ website there is a notification link, which allows public officials to report via e-mail material irregular variances, losses, shortages, or thefts. Telephone and in-person reporting is also acceptable. Reports will be followed up with a return e-mail or call to gather additional information as necessary…”

Please review the entire contents of the Amended State Examiner Directive 2015-6.

FEDERAL AND STATE MILEAGE RATES

The Federal business mileage rate is available at www.irs.gov. The State mileage rate can be found on the Indiana Department of Administration’s website.

IC 5-13-6-1(e) states that all local investment officers shall reconcile at least monthly the balance of public funds, as disclosed by the records of local officers, with the balance statements provided by the respective depositories.

In addition to compliance with statute, monthly bank reconcilements provide internal controls to achieve the safeguarding of public assets. We have received numerous reports that bank routing and account information is being used to create false checks that are clearing bank accounts and stealing public funds. If the unauthorized payments from the account are brought to the attention of the bank in a timely manner, the bank will replace the amount that was stolen. However, if you are not reconciling monthly, you would not be aware of these fraudulent transactions and the delay in reporting these fraudulent transaction to the bank may make it more difficult to get the bank to restore the funds to the bank account. Review the bank statement monthly and verify that all of your recorded deposits are credited to your account and all withdrawals from the account are transactions that trace to checks prepared by your office or electronic funds transfers that you have authorized. By doing this, you would catch any bank errors in a timely manner. In addition you would be able to identify any fraudulent activity as early as possible.

- N

Please see June 2025 Libraries Bulletin Page 1-9

- O

OVERDRAWN FUNDS AND APPROPRIATIONS

The overdraft of a fund or appropriation is prohibited by law. Expenditures are limited to the balance in the particular fund and, in the case of budgeted funds, to the balance of the appropriation therefore. Please see IC 6-1.1-18-4. The following Uniform Compliance Guideline is in the Accounting and Uniform Compliance Guidelines for Libraries, Chapter 1:

“The cash balance of any fund may not be reduced below zero. Routinely overdrawn funds could be an indicator of serious financial problems which should be investigated by the unit. In an instance in which a unit receives a reimbursement grant, the unit must be claiming reimbursement in a timely manner. In this case, it would be possible for a fund to be overdrawn for a short period of time.”

- P

Public Work Projects Costing Less than $150,000

The Public Employees’ Retirement System (PERF) Hybrid plan has two components, the defined benefit plan and the member’s annuity savings account. The member’s annuity savings component has been redefined as a “defined contribution” plan effective January 1, 2018. This change in definition will require a change in the disclosure in the notes to the financial statements for pensions. The defined contribution plan must be disclosed in a separate paragraph from the defined benefit plan component. In the past, these plans were presented together.

For the Enhanced Regulatory financial statements for 2019, this information will be shown in the pension note disclosure, however, in reviewing and approving the financial statements and notes to the financial statements, you will need to review that the defined benefit component has been separately identified. On the SBOA website at www.in.gov/sboa under 2019 Gateway-Annual Financial Report (AFR) Changes there are example reports. These reports provide an example of how the note disclosure for the defined benefit component should be reported. If any of your employees are enrolled in the My Choice plan rather than the PERF Hybrid plan, this will also need be disclosed as a defined contribution plan.

Whenever the cost of a public work project is estimated to be:

1. Less than $50,000 then IC 36-1-12-5 applies (link: https://iga.in.gov/laws/2025/ic/titles/36#36-1-12-5)

2. At least $50,000 and less than $300,000 then IC 36-1-12-4.7 applies (link: https://iga.in.gov/laws/2025/ic/titles/36#36-1-12-4.7)

3. At least $300,000 then IC 36-1-12-4 applies (link: https://iga.in.gov/laws/2025/ic/titles/36#36-1-12-4).

A bond or certified check shall be filed with each bid by a bidder in amount determined and specified by the board if the cost of the public work is estimated to be more than $200,000. A bond or certified check may be filed with each bid by a bidder in an amount determined and specified by the board if the cost of the public work is not more than $200,000.