Fast Facts:

Legislation passed during the 2023 legislative session changed retirement eligibility rules for long-term employees currently working in the Indiana Public Retirement System's (INPRS) PERF Hybrid and TRF Hybrid plans. Beginning July 1, 2023, active employees age 65 or older with 20 or more years of total service may retire under the Millie Morgan retirement option. Previously, the age requirement for this retirement option was age 70 or older.

Details:

Collecting your pension benefit while you continue to work may sound too good to be true, but it's a benefit that's been available for active, long-term employees in INPRS's PERF or TRF Hybrid plans for years. Known as the Millie Morgan retirement option, active employees who meet age and service requirements may choose to begin receiving their pension benefits while remaining employed in their INPRS-covered position.

Legislation passed by the Indiana General Assembly in 2023 expanded the age eligibility to age 65 (down from age 70) and retained the 20 years of total service credit requirement. This means that more long-term employees can begin collecting their pension benefits, which may help more retirement dreams become possible.

Members considering this option will need to review their situation carefully, as their retirement selection is permanent and will not adjust while they continue to work or after they leave PERF or TRF Hybrid-covered employment.

Details to Consider:

- The decision to retire under the Millie Morgan eligibility rules is permanent.

- All normal retirement options are available to members retiring under the Millie Morgan eligibility rules.

- You'll need to decide whether to continue making contributions to your defined contribution (DC) account. All PERF and TRF Hybrid members pay 3% toward their DC account however, some employers pay this on their employees' behalf. If you choose to continue DC contributions, your account will be funded the same way it is today.**

- Selecting this option is a decision you make with INPRS, not your employer. Individuals choosing the Millie Morgan retirement option will remain active employees with their employer until they decide to separate from employment.

- Questions regarding other employer-provided benefits like health insurance or paid time off should be directed to your employer.

- Eligible members are not required to choose this option, nor is there a limited window of time to submit their applications. INPRS will need time to process the members' retirement, but all benefit payments will be paid to the member in full upon final processing based on the members' chosen retirement date.

** Employers may change their contribution methodology at any time. Check with your employer for more information

How To Apply

- Active PERF and TRF Hybrid employees whose age and service meet the eligibility criteria for the new Millie Morgan retirement option can log into their account at myINPRSretirement.org and complete their retirement application.

- Eligible members wishing to apply for their benefits based on the new rules must choose a retirement date of July 1, 2023, or after. Members wishing to receive their benefits with a July 1, 2023, retirement date must submit their completed application on or before June 30, 2023.

- Applications submitted after June 30, 2023, should select the first of the month following their submission date. For example, an application submitted on Oct. 10, 2023, would choose Nov. 1, 2023, as their retirement date.

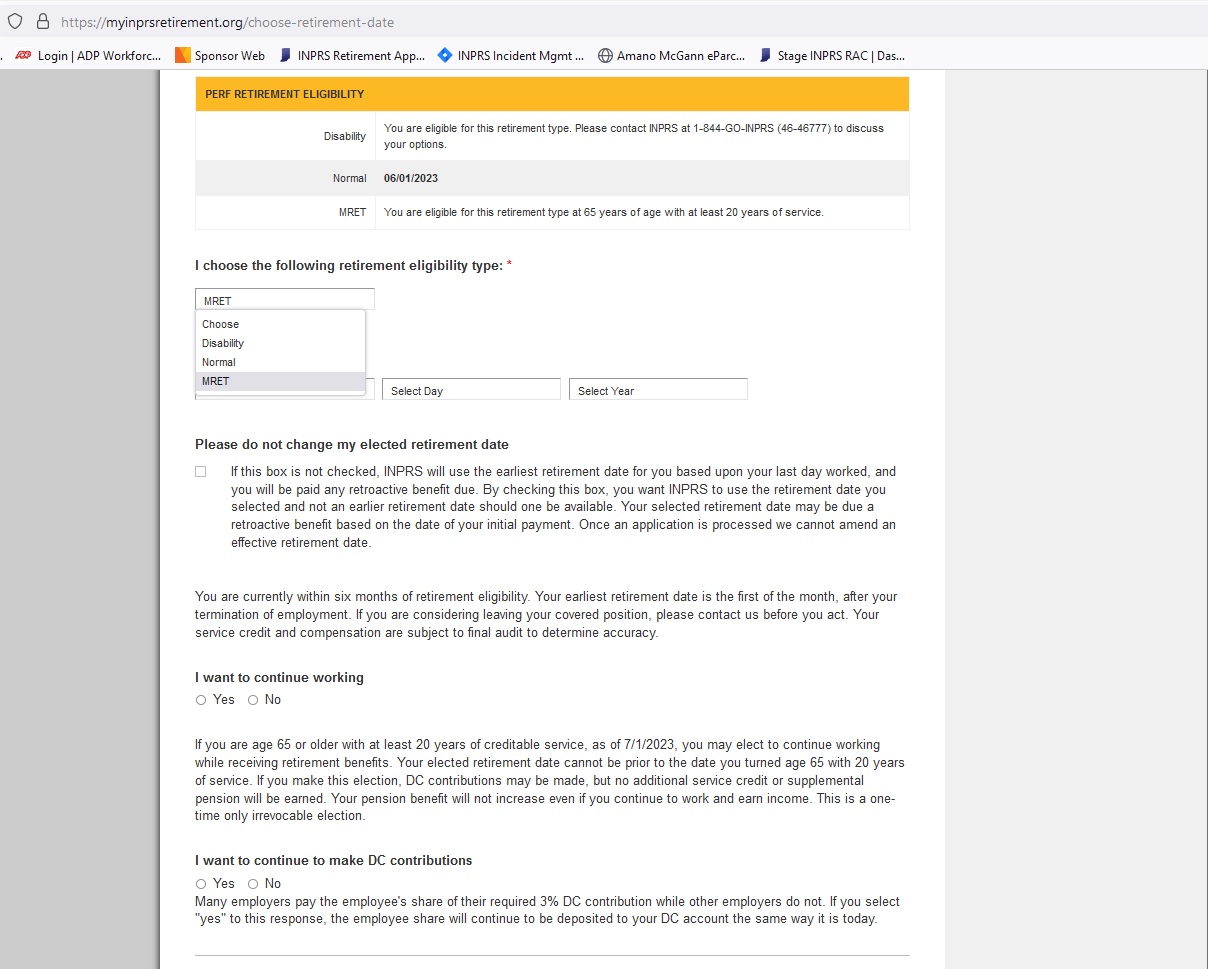

- Within the application, members will select the Retirement Type “MRET” and then members will choose "yes" when the prompt "I want to continue working" is displayed. (As shown in the example screenshot.)

- Next, members will be required to decide whether to continue making contributions to their defined contribution (DC) account. Many employers pay the employee share of 3% while other employers do not. If a member selects "yes" to this response, the employee share will continue to be deposited to the member's DC account the same way it is today.

- Upon submission, INPRS will review the members' eligibility and, if everything is correct, begin paying the member their pension benefits according to their payment selections

- INPRS will need time to process your retirement, but all benefit payments will be paid upon final processing based on your chosen retirement date.

- Get started at myinprsretirement.org

How To Calculate Your Options:

Members considering the benefits of collecting their pension benefits under these new rules may be wondering what will be best in the long run. While there are many factors to consider, every member's unique situation and needs mean that there's no one answer to the question "Should I take my benefits now or later?"

However, there are a few common questions and scenarios worth exploring and calculating on your own. INPRS's retirement benefit calculator, which is pre-filled with the data we have on file for you within your secure online account, is a great place to start. If you don't want to log in, you can also use our generic calculator here.

Below you will find two real-world scenarios to help you have a sense of what the new benefit might look like. These will help you better understand the new changes and guide your own decision about your retirement.

- Scenario 1 - Jean: Take the Money Now or Wait?

Jean is 65 years old and has 20 years of service as of June 30, 2023. She's been planning to retire at age 67 and is looking forward to spending more time with her grandkids. However, she just learned about the new Millie Morgan eligibility rules and she's curious about what that could mean for her.

Her current salary is $50,000 and the average salary that INPRS will use for her pension is $45,000. If she applies for her pension now, she can increase her total income for the last two years that she was already planning on working if she goes ahead and selects the Millie Morgan retirement option. If she does, she’ll be collecting her pension and her regular paycheck from age 65 to 67, when she plans to retire completely. However, she's wondering if this will reduce her overall retirement income by taking her benefit earlier than expected and, if it does, by how much, and when she'd hit a break-even point when she compares taking her pension now or later.

She sat down with INPRS's retirement calculator and here's what she found:

If she takes her Millie Morgan retirement benefit now, she'll get $825 each month when she takes the straight life benefit. Annually, she'll earn $9,900 from her pension and, since she’s still working, her $50,000 salary.

When she retires at age 67, she'll leave her job and the salary that comes with it. However, she’ll have netted $19,800 more since she began collecting her benefit while she completed her final two years of work.

If she waits to take her pension when she retires at age 67, her monthly benefit will be $947.83, which accounts for two more years of service plus the increase in her average salary to $47,000 since she worked to age 67.

The difference between her pension benefit at age 67 compared to the amount it would be if she took it at age 65 is $122.83. If she takes her benefit at age 65, she earns $19,800 for the two years she's collecting and working. While her monthly benefit is $122.83 lower because she began collecting it earlier, it'll take approximately 13 years and five months for her to reach her break-even point.

Jean: Take the money now, or wait? Retire at age 65 and continue working until age 67 Retire at age 67 and stop working Pension Benefit while working (monthly/annually) $825/$9,900 $0 Salary earned year one $50,000 $50,000 Salary earned year two $50,000 $50,000 Total pension payments from age 65 to 67 $19,800 $0 Total earned from age 65 to 67 + monthly pension benefit $119,800 $100,000 Pension Benefit after stopping work (monthly/annually) $825/$9,900 $947.83/$11,373.96 Years to break even on $122.83/mo difference -- 13 years and five months ($19,800/$122.83 = 161.2 months or 13 years and five months) These scenarios assume no increase in annual wages, a Five-year Certain & Life pension, exclude taxes, and are for illustration purposes only. Please request a customized quote and consider your options with a trusted financial provider before making a life-changing financial decision.

- Scenario 2 - Howard: Take the money now, or let my average salary grow?

Howard is 66 years old and has 22 years of service as of June 30, 2023. He's been thinking about retiring, but he received a substantial compensation adjustment recently, so he's been reconsidering his plan.

Before his adjustment, he made $45,000 a year but for the past year, he's earned $60,000. His average salary is now $48,000, meaning that his pension benefit now would be $968. But, if he sticks around for two more years, his average salary would be at least $54,000 without considering any pay-for-performance increases.

He did the math with assistance from our calculator, and this is what he learned:

If he takes his pension benefit now under the new Millie Morgan rules, his monthly benefit would be $968. He's still considering working for a couple more years since his salary has improved so much. If he goes that route, he would be earning his $60,000 salary plus $11,616 through his pension each year.

If Howard decides to wait to retire until age 68, his average salary will grow thanks to his recently adjusted compensation. When he retires at age 68, he'll leave his job and begin to collect his pension, which will be $1,188 each month or $14,256 annually.

Howard's pension benefit will increase if he continues to work and waits to collect it until he retires and leaves his job. The additional two years of service plus the increased average salary make his pension benefit $220 more per month than it would be if he took the Millie Morgan retirement at age 66. However, the two years he'd be collecting his pension while working would add up to $23,232. If he waits to collect his $220 larger pension benefit at age 68, it will take eight years and nine months for Howard to reach his break-even point.

HOWARD: Take the money now, or let my average salary grow? Retire at age 66 and continue working until age 68 Retire at age 68 and stop working Pension Benefit while working (monthly/annually) $968/$11,616 $0 Salary earned year one $60,000 $60,000 Salary earned year two $60,000 $60,000 Total pension payments from age 66 to 68

$23,232 $0 Total earned from age 66 to 68 + monthly pension benefit

$143,232 $120,000 Pension Benefit after stopping work (monthly/annually)

$968/$11,616 $1,188/$14,256 Years to break even on $220/mo difference

-- Eight years and nine months ($23,232/$220 = 105.6 months or eight years and nine months) These scenarios assume no increase in annual wages, a Five-year Certain & Life pension, exclude taxes, and are for illustration purposes only. Please request a customized quote and consider your options with a trusted financial provider before making a life-changing financial decision.

For more information about your pension and navigating to find specifics

For more information about your pension and navigating to find specifics