By MoneyWise Staff

Wednesday, March 4, 2020

In my last post, I explained how remarkable compound interest is and how its positive effects can really boost your savings. However, compound interest also applies to most of your debt like student loans, mortgages and unpaid credit card balances. For those who pay compound interest on loans, it can dig a deep hole that may be difficult to escape. Here's a few examples of how compound interest can dig financial holes:

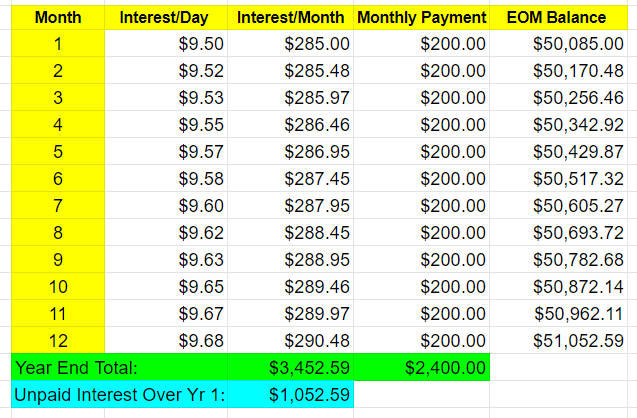

Brandon took out student loans to fund his education, finishing school with $50,000 in student loans at a 7% annual interest rate. Brandon was not able to find a job in his field with a competitive salary, so he entered an income-based repayment program to make ends meet, paying $200 per month. While the repayment program freed up money to help him pay his monthly bills, the payments were not enough to cover the interest on his student loans, much less the principal. After ten years, Brandon’s loan balance grew from $50,000 to $65,866, despite making payments every month. Time and compound interest caused his loan balance to grow. To the right is an example of Brandon’s $50,000 loan with compounding interest creating more debt just over one year.

Brandon’s sister Amanda wanted to go on vacation, but had not saved enough money. Instead of scaling back her plans, she booked a trip to Tahiti on her credit card. Unfortunately, Amanda was unable to pay off her credit card balance, and the interest charges began to compound. Amanda went from owing $10,000 to owing more than $10,786 one year later, even though she paid $150 per month. The credit card’s high 25% interest rate meant that Amanda’s $150 payments didn’t even cover the interest on her debt each month.

What can I do to avoid the pitfalls of compound interest?

- Be discerning about debt. Don’t take on unnecessary debt like Amanda did. Make sure you only take on debt that you can afford to pay back, at an interest rate that won’t hinder your ability to save for your future.

- Pay down high-interest debts. If you already have high-interest debt, refinancing to a lower rate could be a solution for you, but might not make sense for everyone. Do your best to pay off high-interest debts before the compound interest takes its toll on your finances.

Compound interest should be used to your advantage, and to invest for your future. Be cautious in taking on debt and understand how compound interest can derail your finances.

Blog topics: Investing, Budgeting, Archive

The MoneyWise Matters blog has a wealth of information about managing money and avoiding fraud. You can look through the complete archive here.