By

Wednesday, January 15, 2020

Let’s face it, we are emotional spenders. Few of us are able to make purely logical financial decisions. Instead, we spend based on how we feel, and our feelings are impacted by a lot of internal and external forces. If our relationship with money was a Facebook status, it would be listed as “it’s complicated.” And to make matters more complicated, our financial behavior is set at an earlier age than most of us realize.

Let’s face it, we are emotional spenders. Few of us are able to make purely logical financial decisions. Instead, we spend based on how we feel, and our feelings are impacted by a lot of internal and external forces. If our relationship with money was a Facebook status, it would be listed as “it’s complicated.” And to make matters more complicated, our financial behavior is set at an earlier age than most of us realize.

According to a study from Cambridge University, not only are kids able to grasp basic money concepts as early as age 3, but money habits are set as young as age 7. By the time we reach the age of making major financial decisions, we’re already firmly set in our ways. And that’s why it’s okay if you’re struggling to change. Improving our financial behavior is hard, and it takes much more than some facts and figures on a spreadsheet to make changes.

Pay Yourself First

So how do we begin? Well, I like to start with some of the best financial advice I’ve ever heard: PAY YOURSELF FIRST! When faced with a financial decision, repeat those three words in your head. Each time you buy something new and exciting, you are paying someone else. You are giving them money in exchange for the latest gadget you crave.

Paying YOURSELF means setting aside money for YOUR future. This requires discipline. It also requires you to think beyond your need for immediate gratification. If you find yourself frequently tempted into making impulse buys, look for ways to remind yourself of the things you want months or even years from now. Do you want a new car? What about an awesome vacation? Retirement?

Spending that money now can make us feel good in the short term (remember, we spend with our feelings), but in a few years, when we really want/need something big, the money won’t be there. If you’re still working when you’re in your 80s, you may regret not paying yourself first.

Values

Now let’s talk about some of those intangible things that influence our emotional spending. Things like values. Values are qualities or standards people consider to be worthwhile or desirable. These are the basic and fundamental beliefs that guide or motivate our attitudes and actions. Examples include: accomplishment, community, entertainment, generosity, and so on. You may possess some of these values or different ones. Take a moment to think about what you truly value and write it down. Better yet, prioritize your values. When I give financial fitness presentations, I provide folks with a worksheet, so feel free to print a copy for yourself.

Goals

Now let’s talk about goals. Goals are the specific plans or purposes we have in life. Short-term goals can be accomplished in a few weeks, months, or even a year. Examples include setting up a savings account and using it, building an emergency fund, or saving for a family vacation. Long-term goals require more planning and saving, and they are often not realized for many years. Popular long-term goals include homeownership, a college education, or a comfortable retirement.

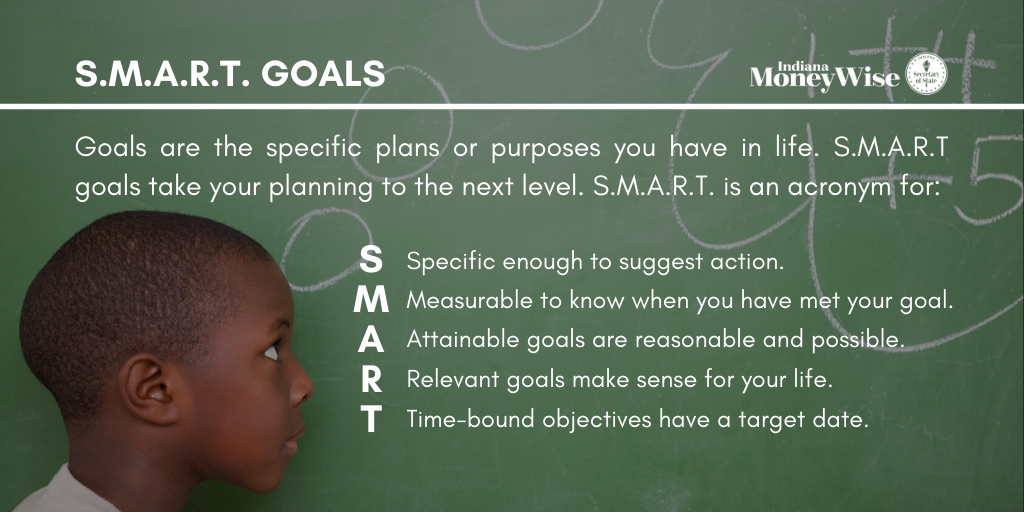

Unfortunately, goals are somewhat meaningless without a plan to achieve them. That’s why I encourage you to create SMART goals. SMART is an acronym.

Unfortunately, goals are somewhat meaningless without a plan to achieve them. That’s why I encourage you to create SMART goals. SMART is an acronym.

- Specific – state exactly what you want to buy or accomplish with the money you save

- Measurable – indicate the exact dollar amount you need in order to reach the goal

- Attainable/Achievable – identify the necessary steps to achieve this goal

- Relevant – the goal needs to be meaningful or you may lose motivation

- Time-Bound – the goal should have a deadline for achievement

Let’s transform a regular goal, such as “I want to buy a car” into a SMART goal. “I plan to save for a down payment on a new car. I need to save $5,000 for the down payment. I will reach my goal of saving $5,000 by setting aside $200 from my paycheck each month. I need a new car because my current car is getting old and repairs will become costly. By saving $200 a month, I will save $5,000 in 25 months (or two years and one month).”

Now that’s a SMART goal! To help you create your own SMART goals, print the worksheet I created.

Wants vs Needs

Now that we’ve established our values and goals, it’s time to buy stuff, right? Not yet. We need to talk about wants versus needs.

As children, we are taught that needs are the stuff that’s necessary for survival: food, water, shelter. Wants are all the stuff we can live without but would enjoy having. Using these simple definitions, we can put things like rent, groceries, and transportation into the needs category, and most of our entertainment options are considered wants. But this whole post is about our complicated relationship with money, and wants and needs are not quite so simple.

A few years ago, I was helping some local Girl Scouts earn their Junior level Savvy Shopper badge. We made collage posters with magazine clippings, with wants on the right side of the poster and needs on the left side. One girl brought up an interesting question: where does deodorant go? It sparked an insightful conversation that helped me realize our wants and needs are more complicated and simply deciding what’s necessary for survival. The girls and I talked about how it might be hard to make friends or get a job if we smell bad. We Googled the history of deodorant (great article can be found here). We even discussed cultural differences related to hygiene. In the end, we decided that wants and needs are complicated. They are also unique and personal. Everyone has different priorities, and so everyone has different wants and needs. Identify your own wants and needs, just as you did with your values and goals. Your spending and saving decisions should be reflective of these choices. To help you determine your own wants and needs, we have another worksheet you can complete. It’s a great activity to do with other members of your family.

A few years ago, I was helping some local Girl Scouts earn their Junior level Savvy Shopper badge. We made collage posters with magazine clippings, with wants on the right side of the poster and needs on the left side. One girl brought up an interesting question: where does deodorant go? It sparked an insightful conversation that helped me realize our wants and needs are more complicated and simply deciding what’s necessary for survival. The girls and I talked about how it might be hard to make friends or get a job if we smell bad. We Googled the history of deodorant (great article can be found here). We even discussed cultural differences related to hygiene. In the end, we decided that wants and needs are complicated. They are also unique and personal. Everyone has different priorities, and so everyone has different wants and needs. Identify your own wants and needs, just as you did with your values and goals. Your spending and saving decisions should be reflective of these choices. To help you determine your own wants and needs, we have another worksheet you can complete. It’s a great activity to do with other members of your family.

So how will all of this critical thinking improve your financial situation? Wants, needs, values, and goals are important parts of every budget. After you have identified the emotional drivers behind your spending and saving decisions, start a spending log. I recommend using it for at least a week, but a month is preferred. Keep track of every last cent! In addition to writing down the date, purchase, and cost of all your expenses, also write whether they satisfy wants or needs.

Blog topics: Budgeting, Credit, Archive

The MoneyWise Matters blog has a wealth of information about managing money and avoiding fraud. You can look through the complete archive here.