Search for Keywords

For additional compliance guidelines issued through SBOA Bulletins, please see this page.

Preface

- Preface

Pursuant to Indiana Code (IC) 5-11-1-24, the State Board of Accounts is required to “establish in writing uniform compliance guidelines… [that] include the standards that an entity must observe to avoid a finding that is critical of the audited entity for a reason other than the audited entity’s failure to comply with a specific law.” Currently, these guidelines are found in SBOA Accounting and Uniform Compliance Guidelines Manuals (Manual), Bulletins, and State Examiner Directives. All guidelines are published on our website with the pertinent guidelines for a particular unit type identified through links.

The Manuals provide the most comprehensive uniform compliance guidelines, including audit positions general to all units, minimum requirements specific to particular units, and topical general standards.

The Bulletins are designed to supplement certain Manuals. Bulletins are published quarterly for Cities & Towns, County, Non-Governmental Entities, Schools, and Townships. The Bulletins typically supply a schedule of upcoming deadlines, new or updated audit positions, and information that local officials needs to be aware of. The Manuals are updated annually for new or updated positions that were included in the Bulletins through the course of the year.

A Directive is a pronouncement by the State Board of Accounts (the Board) that sets forth a policy or procedure that the Board will use to enforce a law or Uniform Compliance Guideline (UCG) to conduct audits, and to carry out its duties as set forth by the Indiana legislature. A Directive is based on the general authority of the Board to carry out its responsibilities under IC 5-11-1 and other laws, and may be a form of the UCGs authorized by IC 5-11-1-24. The Board has the authority to direct public officers in keeping the accounts of their offices, including the use of forms, records, and systems of accounting and reporting adopted by the Board. A person who refuses to follow a Directive is subject to a civil action for an infraction.

If you have any questions for our office, whether it be about these UCGs, or otherwise, please don’t hesitate to call our office at (317) 232-2513 or send an email to one of the following:

Cities.Towns@sboa.in.gov

Communications@sboa.in.gov

Counties@sboa.in.gov

Libraries@sboa.in.gov

NotForProfit@sboa.in.gov

Schools.Townships@sboa.in.gov

SpecialDistricts@sboa.in.govPaul D. Joyce, CPA, State Examiner

Beth Kelley, CPA, Deputy State Examiner

Tammy R. White, CPA, Deputy State Examiner

General Information and Appendix

Chart of Accounts

- Libraries - Chart of Accounts

Fund Type Fund Number Fund Name General 100 Operating 101-110 Reserved for cash change and/or petty cash Special Revenue 200 Gift 201 Rainy Day 202 Contractual Services 203 Levy Excess 204-225 Reserved - future statutory funds 226-275 Reserved - other special revenue 276-299 Grants - federal and/or state Debt Service 300 Bond and interest redemption 301-399 Reserved - other debt service Capital Projects 400 Library Improvement Reserve (LIRF) 401 Construction 402 Capital Projects 403-410 Reserved - other capital projects 411-420 Gift (restricted to capital uses only) 421 Rainy Day (restricted to capital uses only) Permanent 500-599 Reserved for permanent funds Proprietary Enterprise 600-699 Reserved for enterprise funds Internal Service 700-799 Reserved for internal service funds Fiduciary Clearing 800 Public Library Access Card (PLAC) 801 Evergreen 802 Payroll 803-850 Reserved - other clearing funds Trust 900-999 Reserved for trust funds

Library Board of Trustees

- Board Members

Compensation

All members of the board serve without compensation and may not serve as paid employees of the public library. [IC 36-12-2-21] The only exception is the treasurer, who may receive compensation. [IC 36-12-2-22] This compensation should be set by board policy.

Liability

IC 34-6-2-127 and IC 34-30-4 provide that board members are immune from civil liability arising from negligent performance of duties. "Performance" is defined as acts pertaining to the setting of policy and the controlling or overseeing of the activities or functional responsibilities of the library.

Oaths of Office

IC 5-4-1 and IC 36-12-2-19 require each board member to take an oath of office before entering on the member’s duties and to file such oath with the circuit court clerk in the county containing the greatest percentage of the population of the library not later than thirty (30) days after beginning the term of office.

- Board Meetings

The library board shall meet at least monthly and at any other time a meeting is necessary. Meetings may be called by the president or any two board members. A majority of the members is necessary to establish a quorum for the transaction of business. All meetings, except executive sessions, are open to the public. [IC 36-12-2-23 and IC 5-14-1.5-3]

The secretary of the library board shall keep a record of the proceedings of the meetings of the library board. The proceedings and determinations of the board shall be recorded in a book to be kept for that purpose. This book is a public record of the library.

Indiana Open Door Law

Public library board meetings are governed by the Open Door Law, IC 5-14-1.5, as well as by general provisions in the Public Library Law. Under the open door law all meetings of governing boards must be open to the public except for executive sessions. See other sections below for more information on executive sessions, public notice, and minutes of board meetings.

- Treasurer

Elected by Library Board

The "library board shall annually elect a treasurer of the public library. The treasurer may be either a member of the library board or an employee of the library. However, the library director may not also be treasurer." The library board may fix the rate of compensation for the treasurer.

Duties

The following duties are assigned to the treasurer. The treasurer:

- is the official custodian of all library funds;

- is responsible for the proper safeguarding and accounting for all library funds;

- shall issue warrants approved by the library board in payment of expenses lawfully incurred in behalf of the public library; and,

- shall make financial reports of library funds and present the reports to the library board every month.

Other powers and duties may be prescribed by the library board. [IC 36-12-2-22]

- Official Bond of Treasurer and Employees

Treasurer

The Treasurer shall give a surety bond for the faithful performance of duty and for the accurate accounting of all money coming into the treasurer's custody. The bond must be:

- written by an insurance company licensed to do business in Indiana;

- for the term of office of the treasurer; (The term of office is one year)

- in an amount determined by the library board; (It is recommended that the minimum amount of a Treasurer’s bond be at least $15,000)

- paid for with the money from the library fund;

- payable to the State of Indiana;

- approved by the library board; and

- deposited in the office of the recorder of the county in which the library district is located. [IC 36-12-2-22]

Other Employees

It is recommended that employees of the library who handle money also be bonded. Bonds of employees must also be payable to the State of Indiana and be filed in the county recorder's office.

Amount of Coverage

The amount of bond coverage should be determined by the library board and recorded in the minutes. 2013 2-3

Payment of Premium and Other Fees

The general statutes on bonding provide that the bond may be paid from funds of the municipal corporation "without an appropriation having been previously made therefore, in such amount as may be necessary to pay the cost of such bond or obligation." [IC 5-4-5-3] However, it is recommended that a provision for payment of such premium be included in the annual budget.

No charge shall be made by the county recorder for the filing and recording of official bonds. [IC 36-2-7-10]

- Annual Library Reports

Public libraries are required to file electronically an annual financial report with the State Board of Accounts pursuant to IC 5-11-1-4 not later than sixty (60) days after the end of each year. In addition, public libraries are required to file electronically Form 100R, Report of Names, Addresses, Duties and Compensation of Public Employees, in accordance with IC 5-11-13-1 during the month of January.

IC 5-3-1-3.5 requires all libraries with a total annual budget of at least three hundred thousand dollars ($300,000) to publish the Cash and Investments Combined Statement of the annual financial report within sixty (60) days after the expiration of each calendar year.

Annual statistics of public libraries are required by the Indiana State Library under the provisions of the Indiana Library and Historical Board. [IC 4-23-7.1-22] Report forms are provided by the State Library to be submitted by January 31 of each year.

- Fines and Fees

Use of Library Facilities and Services

Residents or property taxpayers of the library district may use the facilities and services of the public library without charge for library or related purposes. However, the library board may fix and collect fees and rental charges, and assess fines, penalties, and damages for the loss of, injury to, or failure to return any library property or material. [IC 36-12-2-25(a)]

Library Cards

The board may issue local library cards to residents and real property taxpayers of the library district, Indiana residents who are not residents of the library district, and individuals who reside out of state and who are being served through an agreement under IC 36-12-13. [IC 36-12-2-25(b)]

The library board must set and charge a fee for a local library card issued to an Indiana resident who is not a resident of the library district (unless that resident is a student in a public school corporation or nonpublic school that is located at least in part in the library district and in which students in any grade preschool through grade 12 are educated, or a library employee of the district). The minimum fee that the board may set under this subsection is the greater of the following:

- The library district's operating fund expenditure per capita in the most recent year for which that information is available in the Indiana State Library's annual "Statistics of Indiana Libraries."

- Twenty-five dollars ($25). [IC 36-12-2-25(c)]

A library board may issue a local library card without charge or for a reduced fee to an individual who is not a resident of the library district and who is:

1. a student enrolled in or a teacher in a public school corporation or nonpublic school:

A. that is located at least in part in the library district; and

B. in which students in any grade from preschool through grade 12 are educated;

2. a child receiving foster care services;

3. a library employee of the district; or

4. a student enrolled in a college or university that is located at least in part of the library district;

The board may assess a fee for the issuance of a statewide library card. [IC 4-23-7.1-5.1(a)(2)]

Written Policy

All fees, fines, and other charges should be set in a written policy of the board and adopted at an official meeting of the board.

Method of Collection

Pursuant to IC 36-1-8-11, any payments to a library may be made by any of the following financial instruments that the library board authorizes, by resolution, for use:

- Cash.

- Check.

- Bank draft.

- Money order.

- Bank card or credit card.

- Electronic funds transfer.

- Any other financial instrument authorized by the fiscal body.

As used in this section "credit card" means a credit card, debit card, charge card or stored value card.

If there is a charge to the library for the use of a financial instrument, the library may collect a sum equal to the amount of the charge from the person who uses the financial instrument.

If authorized by the library board, the library may accept payments with a bank card or credit card under the procedures set forth in IC 36-1-8-11(e). However, the procedure authorized for a particular type of payment must be uniformly applied to all payments of the same type.

The library may contract with a bank card or credit card vendor for acceptance of bank cards or credit cards.

However, if there is a vendor transaction charge or discount fee, whether billed to the library or charged directly to the library's account, the library may collect from the person using the card either or both of the following:

- An official fee that may not exceed the transaction charge or discount fee charged to the political subdivision or municipally owned utility by bank or credit card vendors.

- A reasonable convenience fee:

- that may not exceed three dollars ($3); and

- that must be uniform regardless of the bank card or credit card used.

The fees described in subdivisions 1. and 2. may be collected regardless of retail merchant agreements between the bank and credit card vendors that may prohibit such fees. These fees are permitted additional charges under IC 24-4.5-3-202.

The library may pay any applicable bank card or credit card service charge associated with the use of a bank card or credit card.

- Statewide Library Card Program

Participation

IC 36-12-3-2 requires the library board to comply with and participate in the statewide library card program described in IC 4-23-7.1-5.1. However, the library board may enter into a reciprocal borrowing agreement with another library board under IC 36-12-3-7 or IC 36-1-7 to provide library service to or receive library service from the other library board.

Program

The state library shall develop and implement a statewide library card program to enable individuals 2013 2-5 who hold a valid statewide library card to present the statewide library card to borrow:

- library books; or

- other items available for public borrowing from public libraries as established by rules adopted by the Indiana Library and Historical Board under subsection 4-23-7.1-5.1(d);

from any public library in Indiana. The statewide library card program is in addition to any reciprocal borrowing agreement entered into between public libraries under IC 36-12-3-7 or IC 36-1-7.

Requirements

The statewide library card program must provide for at least the following:

- To be an eligible cardholder of a statewide library card or to renew a statewide library card, the individual must:

- be a resident of Indiana;

- ask to receive or renew the statewide library card; and

- hold a valid resident or nonresident local library card issued to an individual by a public library under IC 36-12-2-25.

- The individual's public library shall pay a fee to be established by rules adopted by the Indiana library and historical board under subsection (d) based on not less than forty percent (40%) of the current average operating fund expenditure per borrower by all eligible public libraries as reported annually by the state library in the state library's manual "Statistics of Indiana Libraries." The individual's public library may assess the individual a fee to cover all or part of the costs attributable to the fee required from the public library and the amount charged to all individuals by a public library under this subdivision may not exceed the amount the public library is required to pay under this subdivision.

- Each statewide library card expires one year after issuance to an eligible cardholder.

- Statewide library cards are renewable for additional one year periods to eligible cardholders.

- Statewide library cards shall be available to eligible cardholders at all public libraries.

- Each eligible cardholder using a statewide library card is responsible for the return of any borrowed item directly to the public library from which the cardholder borrowed the item.

- All public libraries shall participate in the Statewide Library Card Program and shall permit an individual who holds a valid statewide library card to borrow items available for borrowing as established by rules adopted by the board.

- A nonresident of a public library taxing district who requests a statewide library card shall pay a fee for that card that includes, but is not limited to, the sum of the following:

- the statewide library card fee that a public library is required to pay.

- The library taxing district's operating fund expenditure per capita in the most recent year for which that information is available in the state library's annual "Statistics of Indiana Libraries." This subdivision does not limit a library district's fee making ability or a library district's ability to enter into township contractual arrangements.

- The Indiana library and historical board shall adopt rules under IC 4-22-2 to implement this section, including rules governing the following:

- the amount and manner in which the public libraries shall remit the fee to the state library for the state library's use in conducting the statewide library card program.

- The manner of distribution and payment to each eligible public library district of the funds generated by the statewide library card program based upon the loans made by each eligible public library. To be eligible for a payment, the public library district must also comply with the standards and rules established under IC 4-23-7.1-11 (library operating and automation standards).

- The manner in which fines, penalties, or other damage assessments may be charged to eligible cardholders for items:

- borrowed but not returned;

- returned to the inappropriate public library;

- returned after the items were otherwise due; or

- damaged.

- The dissemination of the statewide library cards to the public libraries.

- Record keeping procedures for the statewide library card program.

- Any other pertinent matter.

Distributions

A public library is eligible for a distribution of money from the fund if the State Library and Historical Board determines that the public library:

- meets the standards for public libraries established by rules of the board or the board has granted the public library a waiver from these standards; and

- charges a fee in the amount required under IC 36-12-2-25 for issuing a local library card to a nonresident of the public library district.

The State Library and Historical Board shall adopt rules under IC 4-22-2 to establish a formula for the distribution of money in the fund to eligible public libraries. The formula must base the amount of money paid to an eligible public library upon the number of net loans made by the eligible public library under the statewide library card program.

The Indiana State Library shall make distributions no later than August 1 of each year. [IC 4-23-7.1-29]

Distributions are to be deposited as a miscellaneous receipt to the general fund. After appropriation, funds may be used to cover library materials or expenses associated with the sharing of resources.

- Calendar of Financial Reports and Activities

General Duties of All Months

- Post and balance ledgers.

- Prepare monthly financial statement.

- File Monthly Uploads in Gateway per State Examiner Directive 2018-1

- Receive claims; review statutory authority for payment; and record approval or allowance by board.

- Issue warrants for claims properly payable; verify that funds and appropriations are available before issuing warrants.

- Make remittances of federal and state withholding taxes, Social Security taxes and other payroll deductions to appropriate agencies.

January

- Prepare Employer's Quarterly Federal Tax Return for fourth quarter of the preceding year to Internal Revenue Service - Due by January 31.

Note: State withholding tax is required to be reported and paid by the 15th of each month for preceding calendar month; no quarterly report is required. - Prepare withholding statements for employees (W-2) and make annual reports to Internal Revenue Service and Indiana Department of Revenue.

- The local officers designated as members of the board of finance shall meet after the first Monday and on or before the last day of January for the following reasons:

- to elect a president and secretary. [IC 5-13-7-6]

- to receive and review the investment officer's report on investments, which is required under IC 5-13-7-7 and to review the overall investment policy of the library. [IC 5-13-7-7]

- File Report of Names and Compensation of Officers and Employees (Form 100R) electronically on the Gateway. [IC 5-11-13-1]

- File Annual Report with Indiana State Library, 140 North Senate Avenue, Indianapolis, In 46204. [IC 4-23-7.1-22]

February

- Publish Cash and Investments Combined Statement of the Library Annual Financial Report not later than sixty (60) days after the end of the year if the library has a total annual budget of at least three hundred thousand dollars ($300,000). [IC 5-3-1-3.5]

- File Gateway Annual Financial Report.

- File Annual Uploads in Gateway per State Examiner Directive 2018-1

April

- Prepare Employer's Quarterly Federal Tax Return for first quarter of year to Internal Revenue Service - Due by April 30.

May

- Deadline for application for state funds distribution - May 1.

- Deadline for application for PLAC Funds distribution - May 1. [IC 4-23-7.1-29(b)]

- Period for filing application for deductions and exemptions from assessments and/or taxation expires June 10.

- First installment of taxes due County Treasurer May 10. [IC 6-1.1-22-9] County Auditor verifies collections with Treasurer's Certificate of Collections and makes settlement and distribution to governmental units including public libraries. [IC 6-1.1-27-2]

- Annual Budget Workshops for Library Directors and Trustees sponsored by Department of Local Government Finance, State Board of Accounts, and Indiana State Library.

June

- Deadline for certifying names and addresses of every library employee to the county treasurer for the county where the employee works. - Due by June 1. [IC 6-1.1-22-14]

- Any tax exempt organization which failed to file an application for exemption on property for which an exemption was effective for the preceding year may file application on or before June 15. [IC 6-1.1-11-5] Applicant may file the application within fifteen days after receiving notice from the County Auditor.

- Distribution of funds due library made by County Auditor on or before June 30. [IC 6-1.1-27-1]

- Begin preparation of public library's budget for ensuing year.

July

- Prepare Employer's Quarterly Federal Tax Return for second quarter of year to Internal Revenue Service - Due by July 31.

August

- Distribution of state funds must be made to libraries by August 1 by the State Auditor. [IC 4-23-7-28]

- Distribution of PLAC funds must be made to libraries by August 1 by Indiana State Library [IC 4-23-7.1-29(a)].

October

- Prepare Employer Quarterly Federal Tax Return for third quarter of year to Internal Revenue Services – Due by October 31.

November

- Second installment of property taxes is due by November 10. [IC 6-1.1-22-9] After the County Treasurer has entered all credits for collection in the tax duplicate and special assessment duplicated County Auditor makes settlement and distribution.

December

- Deadline for certifying names and addresses of every library employee to the County Treasurer for the county where the employee works - Due by December 1. [IC 6-1.1-22-14]

- County Auditor makes distribution of funds to library - Due by December 31. [IC 6-1.1-27-3]

- Other Administrative Responsibilities

New Hire Reporting

Pursuant to the federal Work Opportunity Reconciliation Act of 1996, all employees must report "new hires" to the Indiana Department of Workforce Development. The report must be filed within twenty (20) days after the hire date and contain the employee's name, address, and social security number.

All questions should be directed to 1-800-437-9130. Information regarding requirements, procedures, and submission methods may be obtained on the Indiana Department of Workforce Development's web page at http://www.dwd.state.in.us.

Filing of Mining Inspection Reports

IC 14-34-15-4 requires that mine inspection reports be filed at a public library in the county in which the surface mining operation is located rather than with the county recorder. These reports should be treated as public records and retained for a minimum of three (3) years.

IC 14-34-3-6 requires a copy of a surface coal mine permit application to be filed in the main public library in the county in which the proposed mining will take place or in an appropriate public office in that county as approved by the Director of the Department Natural Resources. IAC 25-4-109 requires the applicant for the permit to pay the library a fifty dollar ($50) nonrefundable fee.

Audit Reports

IC 5-11-5-8 allows one public library in each county to receive copies of audit reports from the State Board of Accounts of all public entities located in the same county upon written request. Copies of reports are to be open to public inspection. A library may continue to receive the audit reports by filing an annual renewal request in writing with the State Board of Accounts before January 15 of each year.

Voter Registration Forms

IC 3-7-24-5 designates each public library or county contractual library established under IC 36-12 as a distribution site for registration by mail forms.

Each office with a distribution site for registration forms under this chapter shall post a notice in a prominent location easily visible to members of the public. The notice must state substantially the following:

"VOTER REGISTRATION FORMS AVAILABLE HERE

This office has forms that you can fill out to register to vote in Indiana.

If you live in Indiana and are not registered to vote where you live now, and you want to register (or change your registration record), please take one of the forms.

If you cannot find a blank voter registration form in this office, ask us to give you a form.

You must take the form with you and mail or deliver the form to the voter registration office.

Applying to register or declining to register to vote will not affect the assistance or service that you will be provided by this office"

A library with a distribution site for registration forms under this chapter is not required to do the following:

- Accept registration forms when completed.

- Mail or deliver the forms to a circuit court clerk or board of registration. [IC 3-7-24-16]

Child Support Withholdings

IC 31-16-15-16 requires an employer who is required to withhold child support from more than one (1) obligor and employs more than fifty (50) employees to make payments of such withholdings to the State Central Collection Unit through electronic funds transfer or through electronic or Internet access made available by the State Central Collection Unit. All questions should be directed to the Department of Child Services, Indiana Child Support Bureau, at (317) 232-0327 or 1-800-292-0403.

Budgets and Appropriations

- Expenditure Classifications

Personal Services

Personal Services. Personal service is the direct labor of persons in the employment of the library and all related employee benefits.

- Salary of Director - Compensation of the library director.

- Salary of Assistants - Compensation of all assistant library directors, part or full-time employees.

- Salary of Treasurer - Compensation of treasurer when so established by board resolution.

- Wages of Custodians - Compensation of regular employed custodians.

Employee Benefits. Employee Benefits includes only the employer's or library's share of the cost of health insurance, life insurance, retirement and social security payments made to the Public Employees' Retirement Fund and other approved retirement plans. The employee's share is handled through the payroll deduction columns on the Financial and Appropriation Record and, therefore, requires no appropriation.

Supplies

Supplies include commodities which, after use, are either entirely consumed or show a definite impairment of their physical condition and rapid depreciation after use for a short period of time.

Office Supplies. All articles necessary to the proper operation of an office, other than equipment. Examples of office supplies are: prescribed forms and records, letterheads, envelopes, typewriter ribbons, paper clips, pencils, scotch tape, stencils, adding machine tape, carbon paper, and stationery.

Operating Supplies. Supplies used in cleaning, fuel, oil, bottled gas, coal, lubricants, etc.

Repair and Maintenance Supplies. Materials used in repairing buildings, paint, motor vehicle repair supplies, repair parts, plumbing and electrical supplies, etc.

Other Services and Charges

This classification includes all services performed for the library, under express or implied contract, by other than employees of the library. Also included are all expenditures for insurance, premiums on official surety bonds of the designated treasurer or other employees, licenses, refunds, awards, indemnities, rents, tax assessments, dues to organizations, subscriptions to a service, and all other charges of a similar nature. (Subscriptions to magazines, newspapers, and periodicals should be charged to "Capital Outlays".)

Professional Services. Services provided by professionals to the library, such as architectural services, legal services, accounting services, consulting services, etc.

Communications and Transportation. Include costs of freight and express (when such expenses cannot be charged as part of the original cost of the commodity), postage, telephone, traveling expenses, professional meetings.

Printing and Advertising. Charges for advertising and publication of notices in newspapers and periodicals, expenditures for photographing and blue printing and expenditures for printing other than office supplies. Printing of stationery, forms and other office supplies is chargeable to Major Classification 2, Office Supplies.

Insurance. Includes expenditures for any insurance policies covering injury or loss of property. Annual premiums on official surety bonds are also charged to this account.

Utility Services. Includes charges for heat, light, power and water furnished by public utilities. (Also, if applicable, sewage services furnished by a public utility would be charged to this account.) Coal, fuel, oil and bottled gas used for heating should be charged to Major Classification 2, Operating Supplies.

Repairs and Maintenance. All expenditures of a contractual nature for repairs of buildings, structures and equipment, except extensive repairs which would constitute additions or betterments to properties. If repair is performed by regular employees of the library, labor should be charged to Major Classification 1, Personal Services. Repair parts and materials should be charged to Major Classification 2, Repair and Maintenance Supplies.

Rents. All expenditures for the use of properties not owned by the library, such as temporary or emergency office rooms, store rooms, post office box, safety deposit box, rental of equipment, etc.

Debt Service. Expenditures for the reduction of the principal of the library's general obligation bonds and the interest on such bond.

Other. All expenditures for memberships (in the name of the library) in state and national associations of a civic, educational, professional, or governmental nature that have as their purpose the betterment and improvement of library operations. Also, interest on temporary loans; taxes and assessments for streets, sidewalks, sewers and similar improvements; transfers to the Library Improvement Reserve Fund; and all other services not included in other classifications.

Capital Outlays

Capital Outlays include all outlays which result in the acquisition of or addition to capital assets.

Land. All land owned by the library.

Buildings. All permanent buildings owned by the library.

Improvements Other Than Buildings. All other improvements to land owned by the library.

Furniture and Equipment. Consists of machinery, implements, tools, furniture, motor vehicles, typewriters, calculators, microfilm readers, photocopy machines, projectors, and other equipment that may be used repeatedly without material impairment of its physical condition and which has a calculable period of service.

Other Capital Outlays. This classification includes all expenditures for books, periodicals, newspapers, audio-visual materials used for educational purposes and similar items or materials used as basic materials furnished by a library. LIBRARY BUDGET FORMS

IC 6-1.1-17-3 requires that officers of a political subdivision formulate the estimated budget and proposed tax rate using forms prescribed by the Department of Local Government Finance and approved by the State Board of Accounts. These are submitted through the online Gateway system.

Any questions regarding the completion of these forms or the advertising of budgets should be addressed to the:

Department of Local Government Finance

Indiana Government Center North

Room N1058, 100 North Senate Avenue

Indianapolis, Indiana 46204

(317) 232-3777

http://www.in.gov/dlgf - Advance Tax Draws

Pursuant to IC 5-13-6-3 libraries have the power to request an advance on tax money collected for distribution to the various units within the county. Such advance draws can help alleviate cash flow problems caused by a lack of an operating balance. The following procedures must be followed:

- The advanced draw request must be authorized by formal board resolution.

- The request must be made in writing to the County Treasurer. In some counties, it is customary to also send the request to the County Auditor.

- Every County Treasurer shall, not later than thirty (30) days after receipt of written request for the funds, advance such taxes collected before the semiannual distribution.

- The amount of the advance may not exceed 95% of the total amount collected at the time of the advance or 95% of the amount to be distributed at the next semiannual distribution.

At the semiannual distribution, all the advances made to the library shall be deducted from the total amount due the library as shown by the distribution.

If a County Auditor fails to make a distribution of tax collections or an advance tax draw by the deadline for distribution, the library that was to receive a distribution may recover interest on the undistributed tax collections under IC 6-1.1-27-1.

- Library Capital Projects Funds

Purpose of the Capital Projects Fund

A library district may establish a capital projects fund with respect to a facility used or to be used by the library district. The fund may be used to pay for the following:

- planned construction, repair, replacement, or remodeling;

- site acquisition;

- site development;

- repair, replacement, or site acquisition that is necessitated by an emergency. [IC 36-12-12-2]

Definitions

"Emergency" means: (1) when used with respect to repair or replacement, a fire, flood, windstorm, mechanical failure of any part of a structure, or other unforeseeable circumstance; and (2) when used with respect to site acquisition, the unforeseeable availability of real property for purchase.

- "Library Board" means the fiscal and administrative body of a public library.

- "Library District" means the territory within the corporate boundaries of a public library.

Permitted Uses

Money in the fund may be used to pay for the purchase, lease, or repair of equipment to be used by the library district. Also, the fund may be used to pay for the purchase, lease, upgrading, maintenance, or repair of computer hardware or software. [IC 36-12-12-2]

Plan of Revenues and Expenses

Before a library board may collect property taxes for a capital projects fund in a particular year, the library board must, after January 1 and before May 15 of the immediately preceding year, hold a public hearing on a proposed plan, pass a resolution to adopt a plan, and submit the plan for approval or rejection by the fiscal body designated in IC 36-12-12-4. [IC 36-12-12-3(a)]

The property tax levy for this fund is considered part of the Library's maximum levy.

The Department of Local Government Finance shall prescribe the format of the plan. The plan must apply to at least the three years immediately following the year the plan is adopted. A plan must estimate for each year to which it applies the nature and amount of proposed expenditures from the capital projects fund. A plan must estimate:

- the source of all revenue to be dedicated to the proposed expenditures in the upcoming budget year; and

- the amount of property taxes to be collected in that year and retained in the fund for expenditures proposed for a later year. [IC 36-12-12-3(b)]

If a hearing is scheduled on a proposed plan, the library board shall publish the proposed plan and a notice of the hearing in accordance with IC 5-3-1-2(b). [IC 36-12-12-3(c)]

Approval or Rejection of Plan by Appropriate Fiscal Body

If a library board passes a resolution to adopt a plan, within ten days after passing the resolution the board shall transmit a certified copy of the plan to the appropriate fiscal body or fiscal bodies, whichever applies. The appropriate fiscal body is determined as follows:

- If the library district is located entirely within the corporate boundaries of a municipality, the appropriate fiscal body is the fiscal body of the municipality.

- If the library district is not located entirely within the corporate boundaries of a municipality and the district is located entirely within the boundaries of a township, the appropriate fiscal body is the fiscal body of the township.

- If the library district is not located entirely within the corporate boundaries of a municipality or within the boundaries of a township, the appropriate fiscal body is the fiscal body of each county in which the library district is located.

The appropriate fiscal body shall hold a public hearing on the plan within thirty days after receiving a certified copy of the plan and either reject or approve the plan before August 1 of the year that the plan is received. If the plan is approved by the fiscal body, the library board shall publish a Notice of Adoption as required by IC 36-12-12-5 within thirty (30) days of the adoption. [IC 36-12-12-4]

Petition of Objections by Affected Taxpayers

Ten or more taxpayers who will be affected by the adopted plan may file a petition with the County Auditor of a county in which the library district is located no later than ten days after the publication, setting forth their objections to the proposed plan. The County Auditor shall immediately certify the petition to the Department of Local Government Finance. [IC 36-12-12-5(b)]

Notice and Hearing on Taxpayer Objection Petition

The Department of Local Government Finance shall, within a reasonable time, fix a date for a hearing on the petition filed under IC 36-12-12-5(b). The hearing shall be held in a county in which the library district is located. The Department of Local Government Finance shall notify the library board and the first ten taxpayers whose names appear upon the petition at least five days before the date fixed for the hearing. [IC 36-12-12-6]

Determination by Department of Local Government Finance

After a hearing upon the petition under IC 36-12-12-6, the Department of Local Government Finance shall certify its approval, disapproval, or modification of the plan to the library board and the County Auditor. A taxpayer or the library district may petition for judicial review of the final determination of the Department of Local Government Finance. The petition must be filed in the tax court not more than forty-five (45) days after the Department of Local Government Finance’s action [IC 36-12-12].

Appropriations

The Department of Local Government Finance may approve appropriations from the capital projects fund only if the appropriations conform to a plan that has been adopted and approved in compliance with IC 36-12-12. [IC 36-12-12-8]

Amendments

A library board may amend an adopted and approved plan to provide money for the following purposes:

- with respect to a facility used or to be used by the library district, for repair, replacement, or site acquisition that is necessitated by an emergency; or

- supplement money accumulated in the capital projects fund for those purposes. [IC 36-12-12-9(a)]

When an emergency arises that results in costs that exceed the amount accumulated in the fund for the purposes described in number 1 above, the library board must immediately apply to the Department of Local Government Finance for a determination that an emergency exists. If the Department of Local Government Finance determines that an emergency exists, the library board may adopt a resolution to amend the plan. The amendment is not subject to the deadline and the procedures for adoption described in IC 36-12-12-3. However, the amendment is subject to modification by the Department of Local Government Finance. [IC 36-12-12-9(b)]

An amendment adopted under this section may require the payment of eligible emergency costs from money accumulated in the capital projects fund for other purposes or money to be borrowed from other funds of the library board or from a financial institution. [IC 36-12-12-9(c)]

The amendment may also provide for an increase in the property tax rate for the capital projects fund to restore money to the fund or to pay principal and interest on a loan. However, before the property tax rate for the fund may be increased, the library board must submit and obtain the approval of the appropriate fiscal body or bodies, as provided in IC 36-12-12-4. An increase to the property tax rate for the capital projects fund is effective for property taxes first due and payable for the year next certified by the Department of Local Government Finance under IC 6-1.1-17-16. However, the property tax rate may not exceed the maximum rate established under IC 36-12-12-10. [IC 36-12-12-9(c)]

Limitation and Advertisement of Tax Rate

To provide for the capital projects fund, the library board may, for each year in which a plan adopted under IC 36-12-12-3 is in effect, impose a property tax rate that does not exceed one and sixty-seven hundredths cents ($0.0167) on each one hundred dollars ($100) of assessed valuation of the library district and within the maximum levy limits. The rate must be advertised in the same manner as other property tax rates. [IC 36-12-12-10]

Interest

Interest on the capital projects fund, including the fund's pro rata share of interest earned on the investment of total money on deposit, shall be deposited in the fund. The library board may allocate the interest among the accounts within the fund. [IC 36-12-12-11]

Administrative Rules

The Department of Local Government Finance may adopt rules under IC 4-22-2 to implement this chapter. [IC 36-12-12-12]

- Appropriations

The library board shall appropriate funds in such a manner that the disbursements for a year do not exceed the library's budget as finally determined under IC 6-1.1. [IC 6-1.1-18-4]

A contract entered into without a sufficient appropriation balance is void.

Additional Appropriations

IC 6-1.1-18-5 contains the required procedures for requesting additional appropriations, as follows:

- If the library board desires to appropriate more money for a particular year than the amount prescribed in the budget for that year, they shall give notice of their proposed additional appropriation. The notice shall state the time and place at which a public hearing will be held on the proposal. The notice shall be given once in accordance with IC 5-3-1-2(b).

- If the additional appropriation by the library is made from a fund that receives revenue from property taxes levied under IC 6-1.1; the library must report the additional appropriation to the department of local government finance. If the additional appropriation is made from a fund that receives revenue from property taxes levied under IC 6-1.1, subsections (f), (g), (h), and (i), apply to the library.

- However, if the additional appropriation is not made from a fund that receives revenue from property taxes levied under IC 6-1.1, subsections, (f), (g), (h), and (i) do not apply to the library.

- A library may make an additional appropriation without approval of the department of local government finance if the additional appropriation is made from a fund that does not receive revenue from property taxes under IC 6-1.1. However, the fiscal officer of the library board shall report the additional appropriation to the department of local government finance.

- After the public hearing, the library board shall file a certified copy of their final proposal and any other relevant information with the department of local government finance.

- When the department of local government finance receives a certified copy of a proposal for an additional appropriation under subsection (e) the department shall determine whether sufficient funds are available or will be available for the proposal. The determination shall be in writing and sent to the library not more than fifteen days after the department of local government finance receives the proposal.

- In making the determination under subsection (f), the board shall limit the amount of the additional appropriation to revenues available, or to be made available, which have not been previously appropriated.

- If the department of local government finance disapproves any additional appropriation under subsection (f), the department shall specify the reason for its disapproval on the determination sent to the library.

- The library board may request a reconsideration of a determination of the department of local government finance under this section by filing a written request for reconsideration. A request for reconsideration must:

- be filed with the department of local government finance within fifteen (15) days of the receipt of the determination by the library; and

- state with reasonable specificity the reason for the request. The department of local government finance must act on a request for reconsideration within fifteen (15) days of receiving the request.

- A public library that:

- is required to submit the public library’s budgets, tax rates, and tax levies for nonbinding review under IC 6-1.1-17-3.5; and

- is not required to submit the public library’s budgets, tax rates, and tax levies for binding review for approval under IC 6-1.1-17-20 and the library proposes to make an additional appropriation for a year, and the additional appropriation would result in the budget for the library for that year increasing (as compared to the previous year) by a percentage that is greater than the result of the assessed value growth quotient determined under IC 6-1.1-18.5-2 for the calendar year minus one (1), the additional appropriation must first be approved by the city, town , or county fiscal body described in IC 6-1.1-17-20.3(c) or IC 6-1.1-17-20(d), as appropriate.

Forms and formats pertaining to the additional appropriation process are available from the Department of Local Government Finance at the following location:

Department of Local Government Finance

Indiana Government Center North

Room N1058, 100 North Senate Avenue

Indianapolis, Indiana 46204

(317) 232-3777

http://www.in.gov/dlgfAppropriation Transfers

Pursuant to IC 6-1.1-18-6, the library board may transfer money from one major budget classification to another within a department or office if:

- they determine that the transfer is necessary;

- the transfer does not require the expenditure of more money than the total amount set out in the budget as finally determined under IC 6-1.1; and

- the transfer is made at regular public meeting and by proper resolution.

A transfer may be made under this section without notice and without the approval of the Department of Local Government Finance.

Unanticipated LIRF expenditures and appropriation of unanticipated revenue require a board resolution, publication of the additional appropriation request, public hearing and approval by the Department of Local Government Finance.

Temporary Fund Transfers

Pursuant to IC 36-1-8-4(a), a library, by resolution, may transfer a prescribed amount for a prescribed period to a depleted fund from another fund of the library if the following conditions are met:

- It must be necessary to borrow money to enhance the depleted fund;

- There must be sufficient money on deposit to the credit of the other fund that can be temporarily transferred.

- Except as provided in IC 36-1-8-4(b), the prescribed period must end during the budget year of the year in which the transfer occurs.

- The amounts transferred must be returned to the other fund at the end of the prescribed period.

- Only the revenues derived from the levying and collection of property taxes or special taxes or from operation of the political subdivision may be included in the amount transferred.

IC 36-1-8-4(b) states: If the fiscal body of a political subdivision determines that an emergency exists that requires an extension of the prescribed period of a transfer under this section, the prescribed period may be extended for not more than six (6) months beyond the budget year of the year in which the transfer occurs if the fiscal body does the following:

- Passes an ordinance or a resolution that contains the following:

- a statement that the fiscal body has determined that an emergency exists.

- A brief description of the grounds for the emergency.

- The date the loan will be repaid that is not more than six (6) months beyond the budget year in which the transfer occurs.

- Immediately forwards the ordinance or resolution to the State Board of Accounts and the Department of Local Government Finance.

Loans, Bond Issues, and Notes

IC 36-12-3-10 allows the library board to do the following:

- Adopt a resolution to make loans or issue notes for the purpose of refunding those loans in anticipation of revenues of the library that are expected to be levied and collected during the term of the loans. The term of a loan may not be more than five (5) years. Loans must be made in the following manner:

- The resolution authorizing the loans must appropriate and pledge to payment of the loans a sufficient amount of the revenues in anticipation of which the loans are issued and out of which the loans are payable.

- The loans must be evidenced by warrants or tax anticipation notes of the library in terms designating:

- the nature of the consideration;

- the time and place payable; and

- the revenues in anticipation of which the loans are issued and out of which the loans are payable.

- Borrow money from other persons.

- Issue, negotiate, and sell negotiable notes and bonds of the public library.

- Levy, assess, and collect, at the same time and in the same manner as other taxes of the public library are levied, assessed, and collected, a special tax in addition to the tax authorized by IC 36-12-3-12, sufficient to pay all yearly interest on the bonded and note indebtedness of the public library.

- Provide a sinking fund for the liquidation of the principal of the bond when it becomes due.

- IC 36-9-41 allows libraries to issue a note with a financial institution to finance public works projects of not more than two million dollars ($2,000,000). Such note is payable over a period of not more than six years.

Lapsing of Current Appropriations

Unexpended or unobligated appropriations shall lapse at the close of the year. Every effort should be made to have bills and claims presented before the end of the year, so that such items may be charged to the appropriation and disbursement account of the year in which the service or commodity was supplied.

A claim of a prior year may be paid in the following year if the prior year's appropriation is properly encumbered and sufficient funds are available.

Encumbrance of Appropriation Balances

Appropriations may be encumbered only through a contract or purchase order dated on or before December 31 of that year.

Balances should be carried to the succeeding year only to the extent of unpaid balances due on contracts or purchase orders.

The library board of trustees should make a listing of all encumbered items and make it a part of the minutes of the last business meeting of the year.

Appropriations that are carried forward should be shown as separate amounts on the corresponding appropriation ledger sheets of the previous year with an explanation and then added to the succeeding year's appropriations. The disbursements charged to the appropriations of the previous year should be identified as such on the succeeding year's appropriation ledger sheets.

Appropriations for Federal Programs

When funds are provided by the federal government either directly to a library or through a state agency for any program or project, the following procedures should be followed:

Advance Grants. Advance grants should be handled as follows:

- Where funds are "advanced" directly to the library by the federal government for a specific purpose prior to making any disbursements by the library, the money should be placed in a separate project fund and disbursements subsequently made from that fund. No appropriation of the federal funds is required.

- Where federal funds are "advanced" to the library through a state agency or department with no state funds added thereto prior to making any distributions, the money should be placed in a separate project fund and subsequent disbursements made from that fund. No appropriation of the federal funds is required. Library Services and Technology Act (LSTA) grants are in this category.

- Where federal funds are "advanced" to the library by a state agency or department and state funds are included along with the federal funds in one check or voucher and the funds are for a specific purpose, the money should be placed in a separate project fund and disbursements made from that fund. Appropriation(s) must be obtained for the combined total (i.e., federal and state) prior to any disbursement being made from that project fund.

Reimbursement Grants. Reimbursement grants should be handled as follows:

Where a federal or state grant provides for payments to be made directly to a library on a "reimbursement" basis after payment of expenses by the library, the entire amount of the federal or state reimbursement may be appropriated by the library board without using the additional appropriation procedures under IC 6-1.1-18-5, if the funds are provided or designated by the state or federal government as a reimbursement of expenditures. [IC 6-1.1-18-7.5]. No separate fund for the project or program is required unless the terms of the grant require one.

Matching Grants. Matching Grants should be handled as follows:

When a federal grant or program requires expenditures or "matching" funds to be provided from library funds, an appropriation must be obtained for the amount of such expenditures or local matching funds. Individual program requirements will dictate whether the appropriation should be obtained within the applicable library fund for expenditures there from or whether an appropriation should be obtained within the applicable library fund for a transfer to a required separate fund. This matter should be set out in the terms and conditions entered into between the library board and officials of the federal agency.

Summary. To summarize, no appropriations of federal funds are necessary: (1) when advanced directly from the federal government for a specific purpose prior to making disbursements, and the money is placed in a separate project fund with disbursements made from that fund; or, (2) when federal funds are received in advance through a state agency for a specific purpose prior to making disbursements and the money is placed in a separate project fund with disbursements made from that fund and there is no state match.

Please keep in mind, if the library board wishes to obtain an appropriation for all funds to be spent (i.e., federal, state, and local), there is certainly no prohibition in state statutes.

Loans – Tax Anticipation Warrants and Notes

IC 36-12-3-10 requires loans to be evidenced by a tax anticipation warrant bearing a specified rate of interest from date of loan to maturity date. IC 6-1.1-20-7 has removed the maximum interest rate but requires if the rate of interest is greater than eight percent (8%), the approval of the Department of Local Government Finance must be secured.

A loan must be repaid from the fund to which the loan was receipted. The principal of a loan may be repaid without an appropriation, but an appropriation is required for payment of the interest on the temporary loan.

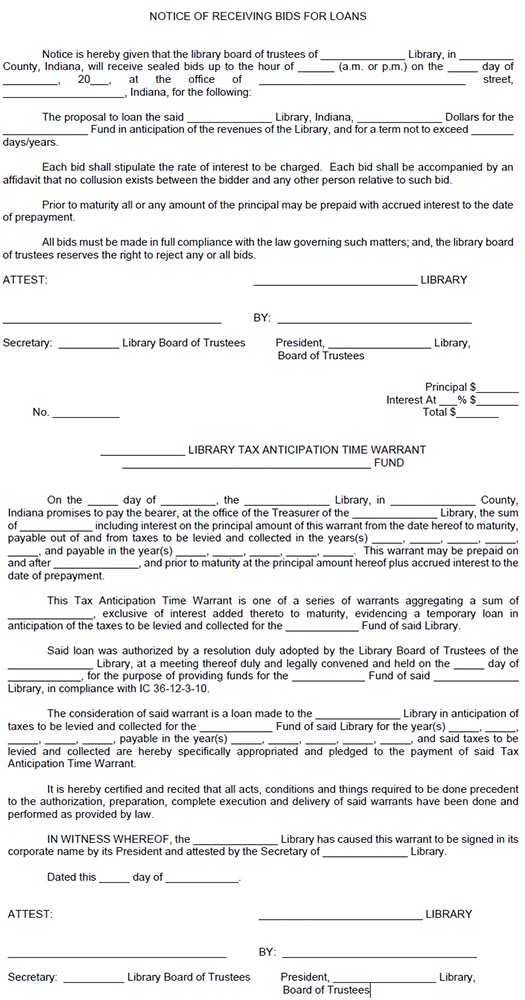

Suggested forms of “Notice of Receiving Bids for Loans” and “Tax Anticipation Time Warrant” which are similar to those now being used in some political subdivisions follow. Please consult your library attorney for advice in this matter.

Notice must be published two (2) times at least one (1) week apart, with the first publication made at least fifteen (15) days before the date of sale, and the second publication must be made at least three (3) days before the date of the sale.

- Public Works Borrowing

This chapter applies to a public work project that will cost the political subdivision not more than two million dollars ($2,000,000) or an eligible efficiency project that will cost not more than three million dollars ($3,000,000). [IC 36-9-41-1]

As used in this chapter, “public work” means a project for the construction of any public building, highway, street, alley, bridge, sewer, drain, or any other public facility that is paid for out of public funds. [IC 36-9-41-2]

Notwithstanding any other statute, a political subdivision may borrow the money necessary to finance a public work project from a financial institution in Indiana by executing a negotiable note under section 4 of this chapter. The political subdivision shall provide notice of its determination to issue the note under IC 5-3-1. Money borrowed under this chapter is chargeable against the political subdivision’s constitutional debt limitation. [IC 36-9-41-3]

A political subdivision borrowing money under section 3 of this chapter shall execute and deliver to the financial institution the negotiable note of the political subdivision for the sum borrowed. The note must bear interest, with both principal and interest payable in equal or approximately equal installments on January 1 and July 1 each year over a period not exceeding ten (10) years. [IC 36-9-41-4]

Financial Accounting and Record Keeping Procedures

- Library Funds

Pursuant to IC 36-12-3-11, the library board may establish funds for money and securities of the public library. All money from whatever source derived is to be receipted into funds established by the library board under authority of law. The authorized funds of public libraries are as follows.

- Library Operating Fund

"All money collected from tax levies, interest on investments, fees, fines, rentals, and other revenues shall be deposited into the 'library operating fund,' except as otherwise provided in this section, and must be budgeted and expended in the manner required by law."

Petty Cash. A "Petty Cash Fund" may be established, for the purpose of paying small or emergency items of operating expense. A receipt must document each disbursement made from the fund. Periodically a voucher must be filed by the custodian of the fund to reimburse the fund for disbursements made. However, no reimbursement can be made unless the original receipts totaling the disbursements claimed are attached to the petty cash voucher. Reimbursement shall be approved and made in the same manner as required for other disbursements for the library. [IC 36-1-8-3]

All receipts (from fines, taxes, etc.) must be deposited to the library's operating fund. According to IC 36-12-3-11, the library is prohibited from spending any of its receipts (with the exception of certain gifts and bequests) except by appropriation. Therefore, fine money may not be spent for the purchase of small items.

The following procedure is advised for minor cash purchases:

- The library board should authorize the establishment of a petty cash fund by placing an item in the budget under "Other Services and Charges" labeled "To establish petty cash fund $__________" (the amount to be determined by the library board). This figure is written into the budget when it is prepared in July or August.

Note: Although the law states that the petty cash fund may be established without appropriation, it is recommended that the library board make an appropriation for petty cash when the fund is established. - In January, when the new budget becomes effective, a warrant should be issued to the person designated by the board to be responsible for the petty cash fund as custodian. The custodian may then purchase small items through the petty cash fund. A receipt (such as a sales check or cash register receipt) must be obtained for each disbursement.

- Receipts and disbursements are then to be entered in a small book used for petty cash along with the balance in cash shown.

- When the need arises to replenish the cash in the fund, all receipts for disbursements from the fund are presented to the board with a claim or other similar certification, just as all other bills are presented.

- After the board approves the claim, another warrant will be issued to the custodian, in the amount of the claim, to reimburse the petty cash fund and bring it back to the original amount.

- At all times the amount of cash plus unreimbursed receipts must equal the original amount of the petty cash fund. Thus, if the fund is $50.00, and $42.33 has been spent for miscellaneous items, the cash on hand should be $7.67 and unreimbursed receipts should total $42.33.

- Expenditures from petty cash are classified in the same manner as all other library disbursements. For example, the total amount of a warrant to reimburse petty cash should be entered in the financial records; and then broken down according into the proper classified columns. A warrant totaling $42.33 may be posted as follows:

Disbursements Postage Office Supplies Cleaning Supplies Books $ 42.33 $ 12.50 $ 10.56 $ 3.96 $ 15.31 - During the course of the year, several warrants to reimburse petty cash may be issued but, in all instances, the expenses must be classified, charged to and limited by the proper appropriation accounts as above. 8. If the custodian of the petty cash funds changes, the entire fund must be returned to the library operating fund, or turned over and receipted for by the person designated by the board to have future custody.

- The library board should authorize the establishment of a petty cash fund by placing an item in the budget under "Other Services and Charges" labeled "To establish petty cash fund $__________" (the amount to be determined by the library board). This figure is written into the budget when it is prepared in July or August.

- Construction Fund

Sources

All money received from the sale of bonds or other evidences of indebtedness for the purpose of construction, reconstruction, or alteration of library buildings, except the premium and interest accrued on the bonds, shall be deposited into the construction fund.

Note: All premium or accrued interest received in the sale of the bonds should be deposited into the Bond and Interest Redemption Fund. [IC 36-12-3-11(a)(3)]

Uses

Money deposited into the construction fund shall be appropriated and expended solely for the purpose for which the indebtedness is created. As provided in the resolution, all expenses incidental to the issuance of the bonds, (including advertising, printing of bonds, attorney fees and any other expenses), and all other costs of construction, reconstruction, or alteration of library buildings incurred should be paid from the proceeds of the bond issue and would be posted, when paid, as disbursements for the Construction Fund. [IC 5-1-14-11] [IC 36-12-3-11(a))2)]

Surplus

Any surplus remaining in the Construction Fund after the purpose for which the bonds were issued has been accomplished or abandoned is required to be transferred by order of the library to the Bond and Interest Redemption Fund and used for the payment of interest bearing indebtedness. [IC 36-12-3-9(c)]

Recording

The "E" Columns, or any other columns not in use, of the Library Financial and Appropriation Record, provide space for entering all transactions affecting the Construction Fund; "E-1" receipts, "E-2" disbursements, and "E-3" balance.

- Bond and Interest Redemption Fund

Source

All money derived from the taxes levied for the purpose of retiring bonds or other evidence of indebtedness, together with any premium or accrued interest that may be received, shall be receipted into the "Bond and Interest Redemption Fund."

Uses

Money in the bond and interest redemption fund shall be used for no other purpose than the repayment of indebtedness.

Recording

The "D" columns of the Library Financial and Appropriation Record provide space for entering all transactions affecting the Bond and Interest Redemption Fund; "D-1" received, "D-2" disbursed, and "D-3" balance. The forth column "Approp. Debt Service" provides for posting of the total amount appropriated from the Bond and Interest Redemption Fund for the retirement of bond principal and payment of interest.

- Rainy Day Fund

IC 36-1-8-5.1 allows a library to establish a rainy day fund to receive transfers of unused and unencumbered funds. The rainy day fund is subject to the same appropriation process as other funds that receive tax money. The fund should be established by resolution and the resolution should state the purposes and sources of funding for the fund. In any fiscal year, a library may transfer not more than ten percent (10%) of the library’s total annual budget for that fiscal year to the rainy day fund.

If a library receives supplemental distributions of CAGIT under IC 6-3.5-1.1-21.1 or COIT under IC 6-3.5-6-17.3, such distributions must be receipted to the rainy day fund. Dormant fund balances under IC 36-1-8-5 may also be transferred to the rainy day fund. Transfers of supplemental distributions of CAGIT or COIT transfers of dormant fund balances are not subject to the ten percent (10%) transfer limit.

Transfers to the rainy day fund may be made at any time during the year. [IC 36-1-8]

Transfers from a debt service fund may not be made to the rainy day fund.

The Department of Local Government Finance may not reduce the actual or maximum permissible levy of a library as a result of a balance in the rainy day fund of the library.

- Library Improvement Reserve Fund

Purpose and Permitted Uses

"Money or securities may be accumulated in any library improvement reserve fund for the purpose of anticipating necessary future capital expenditures such as the purchase of land, the purchase and construction of buildings or structures, the construction of additions or improvements to existing structures, the purchase of equipment, and all repairs or replacements of buildings or equipment."

The Library Improvement Reserve Fund is intended to meet future capital expenditures and repairs for which taxes cannot reasonably be levied in any one year. The plan for using the fund should determine the amount to be appropriated annually to the Library Improvement Reserve Fund as well as the number of years requiring appropriations for this purpose.

Sources

Sources for the Library Improvement Reserve Fund may include endowments and gifts as well as money provided in the budget raised by taxation. However, no authority exists for a separate tax levy for the Library Improvement Reserve Fund.

Establishment

The Library Improvement Reserve Fund may be established by resolution of the library board at any time. However, any tax money to be accrued to the Library Improvement Reserve Fund must be anticipated in the annual budget.

Amount Budgeted

The amount budgeted annually for the Library Improvement Reserve Fund is not statutorily limited.

Any amount intended for an accretion to the Library Improvement Reserve Fund should appear in the annual operating budget in the "Other Services and Charges" section under the classification "Transfer to Library Improvement Reserve Fund."

Additional Appropriations

When Library Improvement Reserve Fund is to be advertised as an additional appropriation, the steps outlined in "Procedure for Requesting Additional Appropriation," should be followed. The model form includes the statement: "These appropriations are made from the unappropriated Library Improvement Reserve Fund balance."

Deposit and Accounting

The sum appropriated for the Library Improvement Reserve Fund should be transferred from the Library Operating Fund to the Library Improvement Reserve Fund. This transfer is achieved through proper authorization by the library board and a warrant drawn on the Library Operating Fund in favor of the Library Improvement Reserve Fund. The library treasurer should endorse the warrant and deposit it in the designated depository. (The Library Improvement Reserve Fund is not to be set up in a separate bank account.) The amount is receipted on the financial and appropriation record in columns "A-1" and "C-1".

While the transfer may be made at any time, it is advisable to make it immediately after each tax draw is received. If the transfer is made after each tax draw, the amount may be half the total amount appropriated to the Library Improvement Reserve Fund or, depending on the library's cash situation, the total amount may be transferred at one time. Unless the transfer is made, the appropriation for the Library Improvement Reserve Fund will expire at the end of the year like any other appropriation balance.

Disbursement Transactions

An appropriation is necessary before any disbursement from the Library Improvement Reserve Fund may be made, except for investments. Appropriation of this fund may be made in the annual budget or, if an emergency arises, an additional appropriation may be made in the regular legal manner, including advertising notice to the taxpayers, public hearing, action by the library board, and approval by the Department of Local Government Finance. The matters of budget, additional appropriation, giving of notices, hearings, etc., are governed by IC 6-1.1-17 and 6-1.1-18.

Disbursements can be made only upon a warrant of the library board, drawn on that bank in which the fund is deposited.

Library Improvement Reserve Fund disbursements should be made directly from the Library Improvement Reserve Fund. Library Improvement Reserve Fund appropriations should not be transferred to the Library Operating Fund before disbursement. Unencumbered balances of appropriations, if any, in the Library Improvement Reserve Fund revert to the Library Improvement Reserve Fund on December 31 of each year.

- Gift Fund

Establishment

Money or securities accepted and secured by the library board as a grant, gift, donation, endowment, bequest or trust may be set aside in a separate fund or funds, and shall be expended, without appropriation, in accordance with the conditions and purposes specified by the donor.

Definitions

The following definitions apply to the gift fund.

"Restricted" gifts are those to which the donor has attached terms, conditions and purposes. These may be quite specific or very general, such as "books", etc.

"Unrestricted" gifts are those to which the donor has not attached terms, conditions or purposes.

Sources

Grants, gifts, donations, endowments, and bequests (hereinafter required to collectively as "gift"). It is the prerogative of the Board to accept or reject any gift.

Income in the form of tax receipts, fees, sale of library property, rental, etc. may not be receipted into the library gift fund.

Accounting

Gifts may be handled in any of the following ways:

Operating Fund. If the gift is unrestricted, the library may receipt the gift into the library operating fund.

- If deposited into the library operating fund, the gift money must be budgeted, appropriated (in the regular budget or by additional appropriation) in the manner prescribed, including advertising and approval by the Department of Local Government Finance. Any gift receipted to the Library Operating Fund must be posted to Columns A-1 and B-1 of the Library Financial and Appropriation Record. Disbursements are to be posted to Columns A-2 and B-2 and also in the applicable appropriation columns.

- Gift money placed into the library operating fund may be spent as determined by the library board within the scope of its statutory authority. It is to be expended as other funds of the library.

- Gift money placed in the library operating fund does not accumulate and must be spent or encumbered within the fiscal year or it will revert to the library operating fund balance and must be reappropriated before the disbursement.

Separate Fund or Funds. A separate fund may be established for each gift; gifts for like purposes may be receipted into separate funds for each purpose; or all gifts may be placed into one "Gift Fund".

Use of Gift Funds. If the library board chooses to receipt any gift (restricted or unrestricted) to a separate fund or funds, the following will apply.

- Gift money may be spent without budgeting or appropriation.

- If restricted, it must be spent according to the donor's restrictions.

- If unrestricted, it may be spent as determined by the library board within the scope of its statutory authority.

- The fund or funds may be accumulated and may be spent at any time the library board determines, unless otherwise required by the terms of the donor.

Accounting. If all gifts are placed into a "Gift Fund", the following accounting will be necessary:

- A subsidiary record to keep track of the disbursements relating to each gift must be maintained.

- The subsidiary record may be kept on any appropriate commercial form or columnar worksheet, such as a cash journal.

- A separate sheet should be opened in this subsidiary record for each restricted gift. Entries to this separate sheet would include the receipt of the restricted gift and disbursements chargeable to each gift including the date, amount and explanation of each.

- Income from the interest on gifts may be receipted into the same fund in which the principal of such gift has been receipted provided it is to be used for the same purpose as the principal. However, if, under the terms of the trust, the principal must be held in trust in perpetuity and only the income used by the governmental unit, there should be two accounts established, one designated as "Trust Principal" and the other designated "Trust Income."

- Unrestricted gift fund monies may be invested as part of the "total monies on deposit," and the interest thereon receipted to the library operating fund.

- All funds, regardless of source, are deposited by the treasurer in only one bank account in each designated depository.

- Receipts to and disbursements from a separate gift fund or funds may be posted in columns D-1, D-2, E-1, E-2, and E-3 or F-1, F-2 , and F-3 on the Library Financial and Appropriation Record if such columns are not being used. If space for additional funds is needed, the optional flyleaf sheet (Library Form No. 1C) should be used. This form contains columns for four additional funds.

Community Foundation Transfers

Gifts to the library may be set aside in an account with a nonprofit corporation established for the sole purpose of building permanent endowments within a community (referred to as a "community foundation"). The earnings on the funds in the account, either deposited by the library or accepted by the community foundation on behalf of the library, may be distributed back to the library for disbursement, without appropriation, in accordance with the conditions and purposes specified by the donor. A community foundation that distributes earnings under this clause is not required to make more than one (1) distribution of earnings in a calendar year. [IC 36-12-3-11(a)(5)(B)]

This action must be authorized by the library board by resolution. Note that the statute does not provide for a return of principal to the library.

- Contractual Service Fund

"All money received in payment for library services or for library purchases made or to be made under the terms of a contract between two (2) or more public libraries under section 6 of this chapter shall be deposited into a contractual service fund. This money shall be expended solely for the purposes specified in the contract and shall be disbursed without further appropriation." [IC 36-12-3-11(a)(6)]

- Levy Excess Fund

Establishment