2023 Schools - Bulletins

Search for Keywords

- A

Accounting and Financial Regulatory Manual

Accounts Receivable – School Lunch and Textbook Rental

Affordable Care Act Penalties, Fines, or Tax

Average Daily Membership (ADM)

The following was provided by the Indiana Archives and Records Administration in response to an inquiry made with the Indiana Public Access Counselor "As I understand your questions, a bank/payroll vendor will be serving as an agent for an Indiana governmental unit regarding access to public records and compliance with records retention. The bank/vendor would thus be required to maintain the checks, bank statements, payroll records, etc. for the same period as the agency. The bank/vendor may well hold the information, but the obligation remains with the agency to provide access upon request, not the bank or vendor. The agency further has the obligation to provide access to the materials throughout the required retention. In the case of cancelled checks/warrants they are currently required to be maintained for 6 (six) years after the completion of the State Board of Accounts Audit. Payroll records are dependent upon the type."

2019 ACCOUNTING AND FINANCIAL REGULATORY MANUAL

We have updated the Accounting and Financial Regulatory Reporting Manual effective for reporting periods beginning January 1, 2019. Units provide information in the Gateway Annual Financial Report submission and that information is included in the financial statements in accordance with this manual. These financial statements are audited by the State Board of Accounts. The following changes discuss the additional information that will be presented in the financial statements and collected from the Annual Financial Report submission in Gateway. This new manual can be found at the link below and under the Uniform Compliance Guidelines section of the school page on the State Board of Accounts website at https://www.in.gov/sboa/4449.htm.

2019 Accounting and Financial Regulatory Reporting Manual

The financial statement will present the beginning balance, total receipts, total disbursements, and ending balance for each fund separately.

Debt and leases will no longer be included in unaudited information but will instead appear in the notes to the financial statements. The debt note disclosure has been updated to include the beginning balance for the year, as well as increases and decreases of long-term debt during the year. The disclosures for debt and leases will include a schedule of principal and interest payments until the maturity of the debt or lease.

Transfers to and from funds will appear as a note disclosure. The note will contain details of the specific fund that transferred money and the fund that received the money. The amount will also be disclosed.

The pension note disclosure will provide additional details, such as benefits provided under the plan, actuarial assumptions, and the funding policy. If postemployment benefits other than pension benefits are offered, a note should indicate the plan type, plan description, benefits offered, and contributions to the plan.

The only schedule appearing as supplementary information will be the Schedule of Capital Assets. The format has been updated to include the beginning balance for the year, as well as increases and decreases of capital assets during the year by asset category.

The appendix of the manual contains examples of the financial statement, note disclosures, and the supplementary information.

We have compiled a document that outlines the schedule of changes to the Accounting and Financial Regulatory Reporting Manual below.

Schedule of Regulatory Changes

The board of school trustees or other governing body of a school corporation has the responsibility to examine and approve all accounts payable vouchers (claims) before they are forwarded to the treasurer of the school corporation for checks to be written in payment thereof. Accordingly, each accounts payable voucher (claim) should be made available for examination by each member of the board present at a public meeting.

IC 5-11-10-1.6(c) provides: "The fiscal officer of a governmental entity may not draw a warrant or check for payment of a claim unless: (1) there is a fully itemized invoice or bill for the claim; (2) the invoice or bill is approved by the officer or person receiving the goods and services; (3) the invoice or bill is filed with the governmental entity's fiscal officer; (4) the fiscal officer audits and certifies before payment that the invoice or bill is true and correct; and (5) payment of the claim is allowed by the governmental entity's legislative body or the board having jurisdiction over allowance of payment of the claim. This subsection does not prohibit a school corporation, with prior approval of the board having jurisdiction over allowance of payment of the claim, from making payment in advance of receipt of services as allowed by guidelines developed under IC 20-20-13-10. "We are of the audit position IC 5-11-10-1.6(c)(2) may be complied with by attaching to the Accounts Payable Voucher Form 523, the receiving copy of the Purchase Order Form 98, signed by the person receiving the goods or services.

IC 5-11-10-2 requires the State Board of Accounts to prescribe a form which will permit claims from two (2) or more claimants to be listed on a single document. IC 5-11-10-2 further provides that when such list is signed by members of the governing body, showing the claims and amounts allowed each claimant and the total claimed and allowed as listed on such document, the members of such governing body need not sign each claim. The form prescribed under this provision shall be prepared by or filed with the disbursing officer of the political subdivision (Treasurer of a School Corporation) together with the supporting claims and all such documents shall be carefully preserved by the disbursing officer as a part of the official records of the office.

The State Board of Accounts has prescribed General Form 364 titled "Accounts Payable Voucher Register". The form provides for showing the dates of the period covered and the number of each page and the total number of pages, date the claim was filed with the school corporation by the claimant, the number assigned to the claim by the school corporation, the name of the claimant, the fund to which the payment will be charged, the amount of the claim as filed, the amount allowed by the board, the check number and any necessary memoranda concerning the claim, particularly in relation to amounts disallowed.

When using General Form 364 in the process of allowing claims, members of the board need not sign or initial each claim. All members present at the meeting at which the claims listed on the register are allowed, in whole or in part, must sign the register.

ACCOUNTS RECEIVABLE – SCHOOL LUNCH AND TEXTBOOK RENTAL

The governing body of a governmental unit should have a written policy concerning a procedure for the writing off of bad debts, uncollectible accounts receivable, or any adjustments to record balances. Documentation should exist for all efforts made by the governmental unit to collect amounts owed prior to any write-offs. Officials or employees authorizing, directing or executing write-offs or adjustments to records which are not documented or warranted may be held personally responsible. We have not taken exception with a School Board approved policy regarding inactive accounts. The policy should define when an account balance is considered inactive. A policy may allow positive account balances to be receipted back into the Fund (we recommend account balances of $10 or less). However, keep in mind that if a parent or anyone else comes forward and makes a request (and could document entitlement), then they would be entitled to a refund. A school should have a policy in place that does not allow significant negative account balances to incur. The School Board approved policy could allow nominal negative account balances to be offset against the positive balances in the Fund. However, any material negative balances should be pursued for collection.

Due to upcoming changes to the Accounting and Financial Regulatory manual issued by the State Board of Accounts (SBOA), the Gateway Annual Financial Report (IC 5-11-1-4) that is due on August 29th, 2021 will be requiring that accumulated depreciation be reported for capital assets. There will be an additional table under the capital assets section of the report which will be requiring the beginning balance, additions, reductions, and the ending balance of accumulated depreciation by asset class. There are other changes to the report such as revisions of the risk assessment questions, financial data by fund reporting, and other changes that SBOA has trained school officials on the past few years.

We have not previously provided specific training on accumulated depreciation, so we are creating a training video that will be emailed out to all units soon. If you have any questions as you are filing the AFR, please contact gateway@sboa.in.gov.

The following is required if the proper officers of any school corporation determine the need for expenditure of more money in the current year than was provided for in the approved annual budget:

(1) The governing body in all cases of additional appropriations must meet and determine that they desire to appropriate for the expenditure of more money than was appropriated in the annual budget. Accordingly, questions concerning the procedures for additional appropriations, should be directed to the Department of Local Government Finance

(2) The governing body determines whether to proceed with the proposal. An approval may not be in excess of the amount advertised, but can be less than requested. The governing body must adopt a resolution of additional appropriations.

(3) If a school corporation proposes an additional appropriation from a fund that receives property tax levied under IC 6-1.1, the additional appropriation must be reported to and approved by the Department of Local Government Finance. A school corporation may make an additional appropriation without the approval of the Department of Local Government Finance if the appropriation is from a fund that does not receive property tax, however, those appropriations shall be reported to the Department of Local Government Finance.

After the public hearing, the proper officers of a school corporation shall file a certified copy of the final proposal and any other relevant information to the Department of Local Government Finance.

(4) Upon receipt of the certified copy of a proposal for additional appropriations, the Department of Local Government Finance will, in not less than fifteen (15) days after receiving the certificate, determine (in writing) if sufficient funds are available or will be available. The Department of Local Government Finance shall limit the additional appropriation to revenues available or to be made available, which have not been previously appropriated.

(5) If the Department of Local Government Finance disapproves an additional appropriation under IC 6-1.1- 18-5, the Department of Local Government Finance shall specify the reason for disapproval on the determination sent to the school corporation.

A school corporation may request a reconsideration of a determination of the Department of Local Government Finance by filing a written request for reconsideration. A request for reconsideration must: (1) be filed with the Department of Local Government Finance within fifteen (15) days of the receipt of the determination by the political subdivision; and (2) state with reasonable specificity the reason for the request. The Department of Local Government Finance must act on a request for reconsideration within fifteen (15) days of receiving the request.

ADMINISTRATIVE EXPENSES TITLES I AND II

Allowable maximums for administrative expenses under Titles I and II are 5% and 10% respectively. Administrative salary expense is governed by federal and state regulations. Salaries of Superintendents of School Districts, Assistant Superintendents, Treasurers of School Districts, Principals of Schools and their Assistants are regularly paid from the General Fund of the School Corporation as necessary operating expenses. Normally the positions are covered by full-time contracts and cannot be reimbursed with Title I and II funds. Payments of salaries from Title I and II funds to these individuals could be considered as supplanting of expenses regularly paid from other school funds. Reimbursement for services provided by these staff positions for these federal funds may be recouped by claiming an Indirect Cost Expense based on the approved school corporation rate. Payments of salaries to a less than full-time treasurer, bookkeeper, teacher or aide whose time can be documented as to which Title served, should be included as a direct expense on the budget. A time log must be maintained to substantiate the charges to each of the applicable funds for person’s salary is paid from more than one fund source.

AFFORDABLE CARE ACT PENALTIES, FINES, OR TAX

The State Board of Accounts has received many questions regarding our audit position with regards to the Affordable Care Act. Most of the questions have inquired specifically about the penalties, fines, or tax associated with this law. While our general audit guidelines prohibit the paying of penalties and interest and states that those payments would be a personal charge to the fiscal officer, administrator, or board, we do not believe this general guideline should apply to this controversial, mandated, and complicated law. We also believe that the governing boards should be making the fiscal decisions associated with their unit of government and the implementation of this law. Therefore, if the fiscally wise decision of the board is to pay the penalties, fines, or tax instead of the cost of the insurance then we will not personally charge the officials involved. One of the conditions necessary to not charging the penalties, fines, or tax is to have the governing board officially document their decision to not comply with the Affordable Care Act. This could be a motion in the board minutes, a resolution, or an ordinance. In summary, as long as there is an official action of the board to choose to pay the fines, penalties, or tax, the State Board of Accounts will not personally hold anyone in that unit of government accountable for reimbursing the cost of those penalties, fines, or tax.

Recently, we have been asked to provide an audit position regarding the distribution and transaction recordings for the Annual Performance Grant provided by IC 20-43-10-3. After discussions with other state agencies and review of the Indiana Code, we will not take exception to school corporations following their current collective bargaining agreement or, if the grant distribution is not included in the collective bargaining agreement, following the suggestions contained in the Indiana Department of Education’s December 3, 2014 memo to distribute the grant on a school building basis.

It is our audit position that we will not take exception to school corporations recording the Annual Performance Grant in their records by receipting the grant amount into the “Performance Based Awards” section (3750-3759) of the Chart of Accounts from the Accounting and Uniform Compliance Guidelines Manual for Indiana Public School Corporations. If the school board has not appropriated expenditures from the fund, then they would need to provide that appropriation prior to the disbursements of the grant.

Finally, it is our audit position that we will not take exception to school corporations recording the Annual Performance Grant in their records by following the suggestions contained in the Indiana Department of Education’s December 3, 2014 memo. The memo suggests that school corporations receipt the grant into the General fund (100). If there are not sufficient appropriations in that fund to make the disbursements, then the school board would have to request additional General fund appropriations approval from the Indiana Department of Local Government Finance.

IC 5-3-1-3(c) provides for the required components of the annual financial report.

IC 5-3-1-3(e) states, "The department of education shall do the following: (1) Develop guidelines for the preparation and form of the financial report. (2) Provide information to assist school corporations in the preparation of the financial report."

IC 5-3-1-3(f) states, "The annual reports required by this section and IC 36-2-2-19 and the abstract required by IC 36-6-4-13 shall each be published one (1) time only, in accordance with this chapter."

IC 5-3-1-3(g) states, “Each school corporation shall submit to the department of education a copy of the financial report required under this section. The department of education shall make the financial reports available for public inspection.”

Please note that the annual financial report referred to in these statutes is not the same Biannual Financial Report (Form 9) that is required to be submitted to IDOE School Finance and it is not the same Gateway Annual Financial Report that is required to be submitted to the State Examiner per IC 5-11-1-4.

IC 20-28-9-18 states "(a) Upon a teacher's written request, a governing body shall withhold the requested amount of money from the salary of the teacher for a purpose described in subsection (c). (b) Upon a written request from a beneficiary of the Indiana state teachers' retirement fund, a governing body may receive a given amount of money for a purpose described in subsection (c). (c) The governing body shall hold the amounts described in subsections (a) and (b) and pay the amounts, as requested by the teacher or the beneficiary, to an insurance company or other agency or organization in Indiana that provides, extends, supervises, or pays for: (1) insurance or other protection; or (2) the establishment of or payment on an annuity account; for the teacher. If a dividend accrues on a policy, the dividend shall be paid or credited to the teacher. (d) If less than twenty percent (20%) of the teachers employed by a governing body request payment of the amounts described in subsection (c) to a single recipient, withholding the amounts of money for insurance, dues, or other purposes is discretionary with the governing body."

Since the statutory definition of a teacher includes the other professional people of the School Corporation, administrators, attendance officers, librarians, etc., the State Board of Accounts will not take audit exception if a school corporation applies IC 20-28-9-18 to those employees also.

IC 5-10-1.1-1 provides, in part, ". . . any political subdivision (as defined by IC 36-1-2-13) may: (1) agree with any employee to reduce and defer any portion of such employee's compensation which under federal law may be deferred under a nonqualified deferred compensation plan and subsequently contract for, purchase, or otherwise procure insurance and investment products appropriate for a nonqualified deferred compensation plan (all referred to in this chapter as "funding"), for the purpose of funding a deferred compensation plan for such employee; (2) if the political subdivision is a school corporation, establish an employee savings plan that is a defined contribution plan qualified under Section 401(a) or 403(b) of the Internal Revenue Code, and contribute amounts to the plan on behalf of eligible employees to be credited and allocated to an account for each employee; and (3) contribute amounts before January 1, 1995, and continue or begin to contribute amounts after January 1, 1995, to a nonqualified deferred compensation plan on behalf of eligible employees, subject to any limits and provisions under Section 457 of the Internal Revenue Code."

The State Board of Accounts is of the audit position that when purchase orders or contracts have been written during the year for the necessary purchases of the school corporation and such purchase orders or contracts have been entered in the Ledger of Appropriations Allotments, Encumbrances, Disbursements and Balances to encumber a sufficient amount of the proper appropriation to provide for payment when due, a permissible procedure is available to carry forward to the next budget year any amounts so encumbered which have not been liquidated as of December 31. Any such encumbrances carried forward must be for the exact amount of the purchase orders or contracts outstanding shall be carried to the same program and expenditure account in the ledger for the new budget year as that in which they appeared for the year ending December 31. These amounts when carried forward should be entered individually on each of the expenditure accounts affected and in total on the program (appropriation) account as an opening entry separate from the next annual appropriation amount. The total amount of encumbered appropriations carried forward for any fund must not exceed the fund cash balance or the available appropriation balance as of December 31 or a funding difficulty could exist during the new budget year.

Liquidation of the amounts carried forward must be made individually for each purchase order encumbered when payment of the claim is entered on the record following receipt of the items purchased. The balance of an encumbrance for a vendor's claim for payment of specific purchases found to be less than the amount of the encumbrance carried forward, may not be used to authorize payment of any other claim. Such balance must be liquidated at the time of liquidating the purchase order or contract or permitted to expire at the close of the budget year. Any amount of claim for payment that is greater than the encumbered amount carried forward must be charged against the available appropriation for the same purpose from the current budget or an additional appropriation obtained for that specific purpose.

Please contact the Indiana Board for Depositories at 317-232-5258, if you have any questions regarding approved depositories or visit http://www.in.gov/tos/deposit/2377.htm.

Any assignment of the wages of an employee is valid only if all of the following conditions are satisfied in accordance with IC 22-2-6-2:

1. The assignment is:

- in writing;

- signed by the employee personally;

- by its terms revocable at any time by the employee upon written notice to the employer; and

- agreed to in writing by the employer.

2. An executed copy of the assignment is delivered to the employer within ten (10) days after its execution.

Some of the purposes for which paying a wage assignment may be made include the following:

1. Premium on a policy of insurance obtained for the employee by the employer.

2. Pledge or contribution of the employee to a charitable or nonprofit organization.

3. Purchase price of bonds or securities, issued or guaranteed by the United States.

4. Purchase price of shares of stock, or fractional interests therein, of the employing company, or of a company owning the majority of the issued and outstanding stock of the employing company, whether purchased from such company, in the open market or otherwise. However, if such shares are to be purchased on installments pursuant to a written purchase agreement, the employee has the right under the purchase agreement at any time before completing purchase of such shares to cancel said agreement and to have repaid promptly the amount of all installment payments which theretofore have been made.

5. Dues to become owing by the employee to a labor organization of which the employee is a member.

6. Purchase price of merchandise sold by the employer to the employee, at the written request of the employee.

7. Amount of a loan made to the employee by the employer and evidenced by a written instrument executed by the employee.

8. Contributions, assessments, or dues of the employee to a hospital service or a surgical or medical expense plan or to an employees' association, trust, or plan existing for the purpose of paying pensions or other benefits to said employee or to others designated by the employee.

9. Payment to any credit union, nonprofit organizations, or associations of employees of such employer organized under any law of this state or of the United States.

10. Payment to any person or organization regulated under the Uniform Consumer Credit Code (IC 24-4.5) for deposit or credit to the employee's account by electronic transfer or as otherwise designated by the employee.

11. Premiums on policies of insurance and annuities purchased by the employee on the employee's life.

12. The purchase price of shares or fractional interest in shares in one (1) or more mutual funds.

13. A judgment owed by the employee if the payment: A. is made in accordance with an agreement between the employee and the creditor; and B. is not a garnishment under IC 34-25-3.

Independent Contractor or Employee:

We often receive inquiries regarding whether an athletic official is an employee of the school corporation or an independent contractor.

The determination whether athletic officials are employees or independent contractors can have important tax, liability, and labor ramifications. Generally, an employer must withhold income taxes, withhold and pay Social Security and Medicare taxes, and pay unemployment tax on wages paid to an employee. An employer does not generally have to withhold or pay any taxes on payments to independent contractors.

IHSAA considers athletic officials to be independent contractors. The IHSAA Officials Handbook states:

"Independent Contractor Status: IHSAA licensed officials are considered independent contractors and not employees of the IHSAA or member schools. As independent contractors, the official is entitled to remunerations for services rendered, but has no entitlements which may be available to an employee of the IHSAA or member schools."

The IRS has not made an official determination of whether athletic officials are employees or independent contractors. However, the IRS has ruled on this issue twice in Revenue Rulings.

In Revenue Ruling 57-119, the IRS held that college sports officials were employees of an athletic association composed of colleges and universities for federal employment tax purposes. The association selected, trained and assigned the officials and also required extensive reporting by the officials.

In Revenue Ruling 67-119, the IRS ruled that a group of high school officials were independent contractors and not employees of their own associations. The association provided training and assigned the officials games, but found that these acts were not enough to make the officials employees of their own association.

The IRS has provided the following guidance for determining if an individual is an independent contractor or employee on their website (http://www.irs.gov/Businesses/Small-Businesses-&-SelfEmployed/Independent-Contractor-Self-Employed-or-Employee):

Common Law Rules

Facts that provide evidence of the degree of control and independence fall into three categories:

1. Behavioral: Does the company control or have the right to control what the worker does and how the worker does his or her job?

2. Financial: Are the business aspects of the worker’s job controlled by the payer? (these include things like how worker is paid, whether expenses are reimbursed, who provides tools/supplies, etc.)

3. Type of Relationship: Are there written contracts or employee type benefits (i.e. pension plan, insurance, vacation pay, etc.)? Will the relationship continue and is the work performed a key aspect of the business?

Businesses must weigh all these factors when determining whether a worker is an employee or independent contractor. Some factors may indicate that the worker is an employee, while other factors indicate that the worker is an independent contractor. There is no “magic” or set number of factors that “makes” the worker an employee or an independent contractor, and no one factor stands alone in making this determination. Also, factors which are relevant in one situation may not be relevant in another.

The keys are to look at the entire relationship, consider the degree or extent of the right to direct and control, and finally, to document each of the factors used in coming up with the determination.

Form SS-8

If, after reviewing the three categories of evidence, it is still unclear whether a worker is an employee or an independent contractor, Form SS-8, Determination of Worker Status for Purposes of Federal Employment Taxes and Income Tax Withholding (PDF) can be filed with the IRS. The form may be filed by either the business or the worker. The IRS will review the facts and circumstances and officially determine the worker’s status.

Be aware that it can take at least six months to get a determination, but a business that continually hires the same types of workers to perform particular services may want to consider filing the Form SS-8.

If you classify an employee as an independent contractor and you have no reasonable basis for doing so, you may be held liable for employment taxes for that worker.

When the athletic official is also employed by the school corporation as a teacher or other employee of the school corporation, this should be disclosed on Form SS-8 and may result in a different determination by the IRS. In instances where an individual provides services in two separate roles to the same business, the IRS examines separately the relationship between the worker and the business for each performance of services. Just as with any examination of worker status, the IRS examines each relationship based on facts that fall into the three categories of evidence explained above—behavioral controls, financial controls, and relationship of the parties. If an employer-employee relationship is found with regard to performance of services for only one role of the worker, remuneration with regard to only those specific services is subject to all FICA and income tax withholding requirements under the Code. If an employer-employee relationship is found for both roles, then remuneration for all services performed by the worker for the business are subject to withholding requirements under the Code.

In conclusion, the determination can be complex and depends on the facts and circumstances of each case. If the IRS rules that a worker was wrongly classified as an independent contractor, there could be significant tax penalties imposed on both the employer and employee. We recommend that either the employer or employee file Form SS-8 in advance with the IRS, which will result in the IRS officially determining the proper worker classification for each circumstance.

Payment of Athletic Officials:

The State Board of Accounts will not take exception to the payment of athletic officials using an online payment system with the following conditions:

1. The School Board must authorize the use of the online payment system through a resolution, which has been approved in the minutes.

2. The School Board must implement and insure that proper internal controls are in place.

3. The athletic director shall provide the ECA treasurer with a detailed list of athletic officials that have been scheduled to officiate each contest. A Purchase Order/Accounts Payable Voucher (SA-1) must be completed with a copy of the detailed list attached.

4. The ECA treasurer shall transfer the appropriate rate of payment for each official on the detailed list and the estimated transaction fees for the corresponding payments to the trust account.

5. After the officials have officiated a contest, the athletic director must validate that the contest was held and services were provided through the online payment system.

6. Once the contest has been validated by the athletic director, payments to the officials are initiated by the ECA treasurer through the online payment system.

7. The ECA treasurer shall print and retain a report of all payments and transaction fees paid from the trust account. This listing should be attached to the SA-1, supporting the disbursements from the trust account. Any payment without proper documentation may be the responsibility of that officer or employee.

8. The trust account must be reconciled by the ECA treasurer on a monthly basis.

9. The ECA treasurer is responsible for compliance with all rules, regulations, guidelines, and directives of the Internal Revenue Service and the Indiana Department of Revenue.

10. At the end of the school year, all funds remaining in the trust account must be receipted back into the extra-curricular Athletic Fund and deposited into the ECA bank account.

Attendance Officers; Appointment In Completely Reorganized Counties

In a county which has been completely reorganized into one or more school corporations under IC 20-23-4, the governing body of each school corporation with fifteen hundred (1,500) or more students in average daily attendance shall appoint an attendance officer. The governing body of each school corporation which has less than fifteen hundred (1,500) students in average daily attendance may appoint an attendance officer. If the governing body of a school corporation which has discretion in whether or not to appoint an attendance officer declines to make an appointment, the superintendent of the school corporation shall serve as ex officio attendance officer under section 35 of this chapter. When the governing body of a school corporation makes an appointment under this section, it shall appoint an individual nominated by the superintendent. However, the governing body may decline to appoint any nominee and require another nomination. The salary of each attendance officer appointed under this section shall be fixed by the governing body; in addition to salary, the attendance officer is entitled to receive reimbursement for actual expenses necessary to properly perform the officer’s duties. The salary and expenses of an attendance officer appointed under this section shall be paid by the treasurer of the school corporation. (IC 20-33-2-31)

Ex Officio Attendance Officers

When the governing body of a school corporation elects not to appoint an attendance officer under section 31 of this chapter or when an appointing authority elects not to appoint an attendance officer under section 33 of this chapter, the superintendent shall serve as an ex officio attendance officer. A superintendent acting in this capacity may designate one (1) or more teachers as assistant attendance officers. These assistant attendance officers shall act under the superintendent's direction and perform the duties the superintendent assigns. Ex officio attendance officers and assistant attendance officers appointed under this section shall receive no additional compensation for performing attendance services. (IC 20-33-2-35)

Joint Employment of Attendance Officer

The governing bodies of two or more school corporations may enter into a voluntary mutual agreement for the joint employment of an attendance officer. The agreement must stipulate the manner in which the joint attendance officer shall be appointed, paid and supervised. The attendance officer may then be appointed, paid and supervised under the terms of the agreement; however, compensation for any attendance officer employed under this section shall be paid entirely by the school corporations involved with no assistance from the civil government. (IC 20-33-2- 36)

Attendance Officers; Appointment In Optional Separate District

The governing body of a school corporation that has fewer than fifteen hundred (1,500) students in average daily attendance may organize the school corporation as a separate attendance district and appoint an attendance officer. The governing body, in making the appointment, shall appoint an individual nominated by the superintendent; however, it may decline to appoint any nominee and require another nomination. All compensation for an attendance officer appointed under this section shall be paid by the treasurer of the school corporation in which the officer is employed. (IC 20-33-2-37)

Attendance Officers; Appointment Of Additional Officers

Any school corporation, attendance district, or remainder attendance district may appoint more attendance officers than are specifically authorized or required under this chapter. However, these additional attendance officers shall be appointed in the same manner as required by law for other attendance officers. Compensation for additional attendance officers appointed under this section shall be paid entirely by the school corporation or school corporations involved. (IC 20-33-2-38)

See IC 20-33-2-39 through IC 20-33-2-41 for information relating to the duties of attendance officers and licensing requirements. See IC 20-33-2-32; IC 20-33-2-33; and IC 20-33-2-34 for information concerning school corporations that have not been reorganized under IC 20-23-4.

IC 20-34-3-14 states, "(a) The governing body of each school corporation shall annually conduct an audiometer test or a similar test to determine the hearing efficiency of the following students: (1) Students in grade 1, grade 4, grade 7, and grade 10. (2) A student who has transferred into the school corporation. (3) A student who is suspected of having hearing defects. (b) A governing body may appoint the technicians and assistants necessary to perform the testing required under this section. (c) Records of all tests shall be made and continuously maintained by the school corporation to provide information that may assist in diagnosing and treating any student's auditory abnormality. However, diagnosis and treatment shall be performed only on recommendation of an Indiana physician who has examined the student. (d) The governing body may adopt rules for the administration of this section." IC 20-34-3-15 used to provide remedial measures for hearing impaired students. However, it was repealed by P.L. 233- 2015.

Inquiries have questioned the correct procedure for accounting for school corporation audit costs.

We find that IC 5-11-4-3(b) remains applicable to guide these processes. IC 5-11-4-3 (b) states in part: ". . . Immediately upon receipt of the certified statement, the county auditor shall issue a warrant on the county treasurer payable to the treasurer of state out of the general fund of the county for the amount stated in the certificate. The county auditor shall reimburse the county general fund, except for the expense of examination and investigation of county offices, out of the money due the taxing units at the next semiannual settlement of the collection of taxes."

Therefore, counties shall continue to forward examination of record payments to the Treasurer of State for school corporation audits and examinations when billed by the State Board of Accounts. The county general fund shall then be reimbursed from property tax collections of that school corporation at the next semiannual settlement. The school corporation may direct the county auditor to reduce the distributions of a specific fund or multiple funds that continue to have property tax levies for the examination of records expense.

AVERAGE DAILY MEMBERSHIP (ADM)

Student Engagement Policy and Supporting Documentation:

When calculating a school’s ADM, which is incorporated into a school corporation’s state tuition support calculation, only “eligible pupils” may be included in the ADM. In order to be considered an “eligible” pupil, the student must be enrolled in the school corporation.

The Indiana Department of Education (IDOE) has released guidance for reporting ADM information and requires supporting documentation of enrollment and attendance information by grade and school to be signed by the building principle, or head of school, and made available in the event of an audit. There is no further guidance as to what the terms “enrolled” and “attending” mean outside of IC 20-43-1. Therefore we are of the audit position that each school should adopt a student engagement policy which would mirror the requirements set forth for virtual charter schools in IC 20-24-7-13(h). If a student fails to continue attending after the ADM count date, the student is still subject to the state’s Compulsory School Attendance requirements found in IC 20-33-2.

Recent audit reports are continuing to note that records to support Average Daily Membership (ADM) as reported to the Department of Education have not been retained in accordance with IC 5-15, the Preservation of Public Records Law.

The State Board of Accounts is of the audit position that School Officials should maintain all records, including ADM records (enrollment cards, rosters, reporting forms, etc.), which substantiate the number of students claimed for ADM.

The building level Official (Principal, Assistant Principal, etc.) responsible for reporting ADM to the School Corporation Central Office should provide a written certification of ADM (written or electronic, which is retained for audit) to properly document responsibility. The certification should at a minimum include a statement detailing the names and location of the records used (these records must be retained for public inspection and audit) to substantiate ADM claimed.

Virtual Schools:

The analysis to determine whether a student is eligible for inclusion in an ADM count for a virtual school is similar to a brick-and-mortar school. The definition of “attending” in IC 20-43-1-7.5 includes that a “virtual presence” is required for a student to be “enrolled” within the virtual school. “Virtual presence” is not defined, however IC 20-24-7-13(h) states:

(h) A virtual charter school shall adopt a student engagement policy. A student who regularly fails to participate in courses may be withdrawn from enrollment under policies adopted by the virtual charter school. The policies adopted by the virtual charter school must ensure that:

(1) adequate notice of the withdrawal is provided to the parent and the student; and

(2) an opportunity is provided, before the withdrawal of the student by the virtual charter school, for the student or the parent to demonstrate that failure to participate in the course is due to an event that would be considered an excused absence under IC 20-33-2.

(i) A student who is withdrawn from enrollment for failure to participate in courses pursuant to the school's student engagement policy may not reenroll in that same virtual charter school for the school year in which the student is withdrawn.

(j) An authorizer shall review and monitor whether a virtual charter school that is authorized by the authorizer complies with the requirements described in subsections (h) and (i).

Therefore, “virtual presence” refers to the regular participation of a student by virtual means. IDOE has recommended that a 30 day period of inactivity be considered when developing student engagement policies.

- B

Board of School Trustees:

Bond Tax Anticipation Warrants

Liability

IC 26-2-7-4 states: "Subject to section 8 of this chapter, a person found liable under other applicable law is liable under this chapter to the holder of a check if the person executed and delivered the check to another person drawn on or payable at a financial institution and the person does either of the following:

(1) Without valid legal cause stops payment on the check.

(2) Allows the check to be dishonored by a financial institution because of any of the following:

(A) Lack of funds.

(B) Failure to have an account.

(C) Lack of an authorized signature of the drawer or a necessary endorser."

Cost and Fees

IC 26-2-7-5 states: "A person liable under section 4 of this chapter is also liable for all of the following:

(1) Interest at the rate of eighteen percent (18%) per annum on the face amount of the check from the date of the check's execution until payment is made in full.

(2) Court costs incurred in prosecuting an action that may be brought by the holder to collect on the check.

(3) Reasonable attorney's fees incurred by the holder if the responsibility for collection is referred to an attorney who is not a salaried employee of the holder. If legal action is filed to effect collection and the collection on the check is referred to an attorney who is not a salaried employee of the holder, the holder of the check is entitled to minimum attorney's fees of not less than one hundred dollars ($100).

(4) Actual travel expenses not otherwise reimbursed under subdivisions (1) through (3) and incurred by the holder to do either of the following:

(A) Have the holder or an employee or agent of the holder file papers and attend court proceedings related to the recovery of a judgment under this chapter.

(B) Provide witnesses to testify in court proceedings related to the recovery of a judgment under this chapter.

(5) A reasonable amount to compensate the holder for time used to do either of the following:

(A) File papers and attend court proceedings related to the recovery of a judgment under this chapter.

(B) Travel to and from activities described in clause (A).

(6) Actual direct and indirect expenses incurred by the holder to compensate employees and agents for time used to do either of the following:

(A) File papers and attend court proceedings related to the recovery of a judgment under this section.

(B) Travel to and from activities described in clause (A).

(7) All other reasonable costs of collection."

Liability for Continued Nonpayment

IC 26-2-7-6 states: "(a) This section does not apply to a person who has allowed a check to be dishonored because of lack of funds if both of the following apply:

(1) The person reasonably believed that there were sufficient funds in the account to cover the check.

(2) The insufficiency of funds is caused by the dishonoring of a third party check that had been deposited into the person's account.

(b) If a person liable under this chapter does not pay to the holder the full amount of the check not more than thirty (30) days after the certified mailing of written notice that the check has not been paid, the person is liable for, and the court shall award judgment for, the following, whichever applies:

(1) If the face amount of the check is not greater than two hundred fifty dollars ($250), three (3) times the face amount of the check.

(2) If the face amount of the check is greater than two hundred fifty dollars ($250), the face amount of the check plus five hundred dollars ($500)."

Remedies

IC 26-2-7-7 states: "A person must elect whether to pursue a claim either under this chapter or under IC 34-24-3-1 (or IC 34-4-30-1 before its repeal)."

Exemption

IC 26-2-7-8 states:

"(a) A person who has allowed a check to be dishonored is not liable under this chapter if, not more than ten (10) days after the holder has given notice that the check has not been paid by the financial institution, the person pays to the holder the full amount of the check.

(b) A payment made under subsection (a) is effective for all purposes as of the date the payment is made." Also, please be aware of IC 35-43-5-5 concerning check deception.

We are often asked if "choir outfits" for students may be bought under the same statute regarding band uniform purchases even though the "choir outfits" could possibly be considered as personal in that the students may keep the clothing.

The State Board of Accounts is of the audit position IC 20-30-15-8(b) provides "A governing body may appropriate from the school corporation's general fund for any one (1) year an amount equal to the total funds raised by school patrons during the year in which the appropriation is made to purchase band uniforms for high school bands sponsored by high schools located within and operated by the school corporation." (Our emphasis) IC 20-30.15-8 does not specifically refer to "choir outfits".

The School Board, if desiring, could consider the provisions of IC 20-26-5-4(a)(3) "Promotion of School" or the provisions of IC 20-26-3-1, et seq., School Corporation Home Rule. The School Corporation Attorney should provide written guidance concerning the applicability of these statutes to the "choir outfits". The appropriateness of a purchase if deemed to be for personal purposes may result in an audit exception.

We have also taken the audit position the purchase of band uniforms is not only a one time purchase, but may be repeated in subsequent budget years, limited each year to an amount equal to the amount raised by school patrons during that same budget year.

BANK STATEMENTS AND CANCELED CHECKS

The treasurer of the school corporation should receive a monthly statement at the close of each month from each designated depository which should include all checks paid through the bank and canceled during the period covered by the statement. IC 5-13-6-1 provides in part, “(e) All local investment officers shall reconcile at least monthly the balance of public funds, as disclosed by the records of the local officers, with the balance statements provided by the respective depositories."

The State Board of Accounts’ audit position is that all canceled checks should be retained in the file with the bank statement with which they were returned which will facilitate any future reference of one to the other that may be necessary for either accounting or audit purposes.

IC 5-15-6-3(a) concerning optical imaging of checks states, in part:

“. . . 'original records' includes the optical image of a check or deposit document when:

(1) the check or deposit document is recorded, copied, or reproduced by an optical imaging process . . . ; and

(2) the drawer of the check receives an optical image of the check after the check is processed for payment . . ."

The Public Purchase Law, IC 5-22-1-1 et seq. and the Public Work Law, IC 36-1-12-1 et seq., both require the preparation of specifications, publication of a legal notice requesting bids for the designated purpose and publishing a time and place for opening of the bids received in required situations.

IC 20-26-4-6 provides that the governing body of any school corporation may designate a committee of at least two (2) of the governing body's members, or a committee of not less than two (2) employees of the school corporation, to open and tabulate bids in connection with the purchase of supplies, material, or equipment; for the construction or alteration of a building or facility; or for any similar purpose. Such bids may be opened by the committee at the time and place fixed by the advertisement for bids; must be read aloud and tabulated publicly, to the extent required by law for governing bodies; and must be available for inspection. The bids must be reported to, and tabulation entered upon the records of, the governing body at its next meeting following the bid opening. No bid shall be accepted or rejected by the committee, but such bid must be accepted or rejected solely by the governing body in a board meeting open to the public as provided in IC 20-26-4-3.

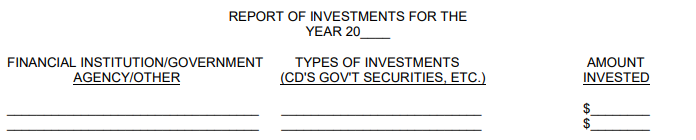

BOARD OF FINANCE - ANNUAL MEETING

IC 5-13-7-6 requires each local board of finance to meet annually after the first Monday and on or before the last day of January. At the annual meeting the board of finance shall elect from the board's membership a president and a secretary. The board of finance shall also receive and review the written report of the investing officer that summarizes the school corporation's investments during the previous year. The report must contain the name of each financial institution, governmental agency or instrumentality or other person with whom the school corporation invested money during the previous calendar year. The board of finance is to review the overall investment policy of the school corporation. The following format is recommended to be completed and given to the Board of Finance:

SCHOOL BOARD MEMBER COMPENSATION - PER DIEM

IC 20-26-4-7 states in part "(a)". . . the governing body of a school corporation by resolution has the power to pay each member of the governing body a reasonable amount for service as a member, not to exceed: (1) two thousand dollars ($2,000) per year; and (2) a per diem not to exceed the rate approved for members of the board of school commissioners under IC 20-25-3-3(d). (b) If the members of the governing body are totally comprised of appointed members, the appointive authority under IC 20- 23-4-28(e) shall approve the per diem rate allowable under subsection (a)(2) before the governing body may make the payments. (c) To make a valid approval under subsection (b), the appointive authority must approve the per diem rate with the same endorsement required under IC 20-23-4-28(f) to make the appointment of the member."

IC 20-25-3-3 states in part (d) "Board members are entitled to receive compensation not to exceed the amount allowed under IC 20-26-4-6 and a per diem not to exceed the rate approved for members of the city-county council established under IC 36-3-4 for attendance at each regular and committee meeting as determined by the board."

We understand members of the City-County Council in Marion County still currently receive one hundred twelve dollars ($112) for regular meetings and sixty-two dollars ($62) for committee meetings.

The State Board of Accounts will not take audit exception to reimbursement in accordance with the aforementioned for meetings that comply with IC 5-14-1.5-1 et seq., the Open Door Law.

Please note IC 5-14-1.5-4 provides in part (b) "As the meeting progresses, the following memoranda shall be kept: (1) The date, time, and place of the meeting. (2) The members of the governing body recorded as either present or absent. (3) The general substance of all matters proposed, discussed, or decided. (4) A record of all votes taken, by individual members if there is a roll call. (5) Any additional information required under IC 5-1.5-2-2.5. (c) The memoranda are to be available within a reasonable period of time after the meeting for the purpose of informing the public of the governing body's proceedings. The minutes, if any, are to be open for public inspection and copying."

We are of the audit position that a board of school trustees should formally determine board members that are eligible to attend, vote, testify, gather information for other committees, etc., and receive compensation for attendance at those individual committee meetings. We are also of the audit position board members which have not been formally authorized by a board of school trustees to attend committee meetings, should not receive compensation for attendance at committee meetings.

QUORUM FOR SCHOOL BOARD ACTION

The State Board of Accounts is sometimes questioned regarding the statutory provision concerning the number of board members necessary to take official action at a board meeting.

IC 20-26-4-3 (f) states "At a meeting of the governing body, a majority of the members constitutes a quorum. Action may not be taken unless a quorum is present. Except where a larger vote is required by statute or rule with respect to any matter, a majority of the members present may adopt a resolution or take any action."

Some specific statutes require a favorable vote from a majority of the total membership of the governing board. IC 20-26-4-4(c) states in part "If a vacancy in the membership of a governing body occurs for any reason . . . the remaining members of the governing body shall by majority vote fill the vacancy by appointing a person from within the boundaries of the school corporation, with the residence and other qualifications provided for a regularly elected or appointed board member filling the membership, to serve for the term or the balance of the term . . ."

IC 20-26-4-8 states in part concerning contracts "However, each contract must be approved by a majority of all members of the governing body." IC 6-1.1-17 which deals with formulation of the annual budget for the school corporation and IC 6-1.1-18-5 concerning additional appropriations each refers to the "proper officers" of the political subdivision which has been generally interpreted as all members of the governing board. If questions arise concerning signatures necessary on budget or additional appropriation documents, you should contact the Department of Local Government Finance.

IC 20-23-4 provides for the redemption of school aid bonds if any, by a reorganized school corporation. These are bonds which were issued by the township, city or town and although they are a debt obligation of the civil unit, since they were originally sold for school building purposes, the statute authorizes the school corporation to stand the expense of redemption by way of collections in the Debt Service Fund for payment to the officials of the civil unit who must in turn repay the bondholders or the paying agent.

Our long standing audit position has been as follows if any school aid bonds still exit: A community school corporation or a united school corporation organized according to the provisions of Chapter 202 of the Acts of 1959 as amended, may assume the obligation to pay the civil corporations located within the geographical limits of the school corporation the amount of the school aid bonds and coupons coming due each year, if the reorganization plan provided for such payments. If the organization plan did not provide for such payments, the board of school trustees may, by resolution adopted, provide for making such payments to civil corporations. The exact amounts of school aid bonds and coupons coming due each year shall be paid to civil townships, civil cities or civil towns in semiannual installments on the 20th day of June and December each year, regardless of the financial status of the civil corporation's Civil Bond Fund. Prior to the 20th day of June and December each year, request that the township trustee, city controller or city or town clerk-treasurer certify to the treasurer of the school corporation the exact amount of school aid bonds and coupons coming due in July and January. The amount so certified must be paid to the civil corporations. School corporation treasurers may not pay civil aid bonds and coupons directly to the payee because these obligations are not a debt of the school corporation. Payments must be made to township trustees or civil authorities. Payments for civil aid bond obligations must be made from the Debt Service Fund, Account 54300.

INDIANA BOND BANK – TAX ANTICIPATION WARRANTS

We are of the audit position that Indiana Bond Bank transactions should be recorded in the records. Accordingly, receipts should be issued (Account 5430) for the amount of the tax anticipation warrant, checks issued (Account 51200) for repayment of the amounts borrowed, Account 60300 should be charged for securities purchased, etc. Additionally, the Treasurer's Daily Balance of Cash, Depositories and Investments, (General Form 361), and Register of Investments (General Form 350) should contain a record of each transaction.

Please note all receipts, checks and records should contain notations that these transactions are in accordance with the Bond Bank Tax Anticipation Warrants issued and note where the securities are held by reference to the safekeeping receipt that you are to receive. Also, please ensure that interest income is properly receipted into the records through the normal accounting system.

Finally, we understand the Indiana Bond Bank will provide guidance concerning any potential arbitrage requirements, and if the entire amount available is not drawn by a school corporation, the residual amount will be sent to a school corporation to be used to repay the total amount of the advance.

AUDIT POSITION ON OFFICIAL BONDS

The State Board of Accounts (SBOA) received numerous questions, concerns, and comments from a variety of sources regarding the changes made to Ind. Code § 5-4-1-18 by Senate Enrolled Act (SEA) 393. In response, the SBOA is issuing the attached Updated Bulletin on SEA 393, which replaces the bulletin issued on July 24, 2015. The attached bulletin addresses or clarifies the following issues:

1. The SBOA will not take audit exception to schedule bonds—by name or position—if the bonds are authorized by ordinance, endorsed to cover faithful performance, and include aggregate coverage sufficient to cover all officers, employees, and contractors required to be bonded.

2. The SBOA will not take audit exception if a political subdivision purchases a crime insurance policy in lieu of a bond if the crime insurance policy is authorized by ordinance, endorsed to cover faithful performance, and includes aggregate coverage sufficient to cover all officers, employees, and contractors required to be bonded.

3. It is the audit position of the SBOA that, for purposes of IC 5-4-1-18(a)(7), a “contractor” is a person or business in a contractual relationship with the political subdivision who has a fiduciary relationship with or performs a fiscal responsibility for the political subdivision, and whose accounts are not otherwise covered by the Federal Deposit Insurance Corporation (FDIC).

…5. Considering materiality and the risk of loss to the governing body of a school corporation, the SBOA will not take audit exception if individuals who receive, process, deposit, disburse, or otherwise have access to public funds in an amount less than $100 per event or duty are not bonded.

...X. Bonds for School Treasurers

A. School Treasurers. School treasurers, deputy treasurers, and “any individual whose official duties include receiving, processing, depositing, disbursing, or otherwise having access to funds that belong to a school corporation or the governing body of a school corporation” must be bonded. IC 20-26-4-5(a).

1. The bond amount is determined by the school corporation’s governing body. IC 20-26-4-5(a).

2. The term of the bond is one year commencing on July 1.

3. The bond may be an individual bond, or a blanket bond if (1) the blanket bond is endorsed “to cover the faithful performance of all employees and individuals acting on behalf of the governing body or the governing body’s school corporation,” and (2) “includes aggregate coverage sufficient to provide coverage amounts specified for each individual required” to be bonded. IC 20-26-4-5(b).

4. The governing body must determine who must be bonded under the statute. The term “official duties” is not defined. It is our position that “official duties” may include duties set forth in a job description, duties that are customary or routinely performed, or duties that are assigned but not frequently performed. For example, cafeteria cashiers, teachers who routinely collect lunch money from students and employees who collect textbook rental fees must be bonded. The statute does not require the individual to be an employee of the school corporation. So, for example, parents volunteering in the school lunchroom or at an extracurricular sporting event must be bonded if their official volunteer duties include receiving public funds such as lunch money or admission fees.

5. There is no dollar threshold or de minimis exception in the statute. However, considering materiality and the risk of loss to the governing body, the SBOA will not take audit exception if individuals who receive, process, deposit, disburse, or otherwise have access to public funds in an amount less than $100 per event or duty are not bonded.

6. We recommend that all bonds be filed with and kept by the trustee or board of school trustees. Copies of the bonds must also be submitted to the State Board of Accounts electronically via Gateway with the school’s Annual Financial Report.

B. Extracurricular Treasurers. Extracurricular account treasurers must be bonded if they handle funds in excess of $300 during the school year. IC 20-41-1-6(a).

1. The bond amount is determined by the superintendent and principal of the school approximating the total “anticipated funds that will come into the possession of the treasurer at any one time during the regular school year.” IC 20-41-1-6(a). If school lunch or textbook rental fees are handled by an extracurricular treasurer, then the governing body must set the amount of the bond “sufficient to protect the account for all funds coming into the hands of the treasurer of the account.” IC 20-41-2-6(b).

2. The term of the bond is not specified, but an extracurricular treasurer must be designated “immediately upon the opening of the school term….” Thus, we recommend an annual bond commencing on July 1.

3. The bond may be an individual bond or a blanket position bond for all extracurricular account treasurers. IC 20-41-1-6(b).

4. The bond must be filed with the trustee or board of school trustees. IC 20-41-1- 6(a). A copy of the bond must also be submitted to the State Board of Accounts electronically via Gateway with the school’s Annual Financial Report.

All Bonding Situations

We have noted situations where various employees (other than bonded treasurers and deputy treasurers) are involved in handling cash and cash related transactions (i.e., textbook rental collections, school lunch, etc.) without the school corporation being afforded bond coverage.

We strongly recommend and encourage school officials to immediately obtain bond coverage for all employees that might be handling cash and related transactions. School corporation officials should also give consideration to providing supplemental crime insurance coverage.

Whenever deemed necessary to bond any other employee of a school corporation, the governing body may bond or cause to be bonded such employee or employees by either individual or blanket bonds conditioned upon faithful performance of duties, and in amounts and with surety approved by the school board. A blanket bond should not include any officer, deputy or employee for whom an individual bond is required by statute. Individual bonds are required for the school corporation treasurer and the deputy treasurer.

The official bonds of treasurers, corporation or extra-curricular, must be written for a period of one (1) year, the term of office of the respective treasurer. Bonds may be for a shorter period for a person appointed to complete the term of a treasurer who resigned or is deceased. The bonds shall be payable to the State of Indiana as required by IC 5-4-1-10; and, after approval, shall be filed and recorded in the office of the recorder of the county wherein the treasurer resides as provided in IC 5-4-1-5.1 as well as with Board of School Trustees. No charge shall be made by the recorder of the county for recording the official bonds of any public officer, deputy, appointee or employee (IC 36-2-7-10).

When a minimum premium is required for official bonds, school corporation officials should make certain maximum coverage is provided for the required minimum premium. The State Board of Accounts is of the audit position a new bond should be obtained each year and continuation certificates or renewals should not be used in lieu of obtaining a new bond.

The procedures for the accounting of the proceeds of the sale of a general obligation bond issue and the investment and use of same are somewhat complicated and require reference to several laws. Our article will be limited to the subject of bond issues for school construction as authorized by IC 20-48-1.

When bonds are sold, the amount of principal (face value) received shall be receipted to a Construction Fund in Receipt Account Number 5110 and deposited in a designated depository for necessary expenditure. The amount then (if desired) may be invested (please ensure arbitrage problems do not exist). Any premium on the sale or accrued interest (interest earned from date of issue or most recent prior interest payment date to the date of sale) must be receipted to the Debt Service Fund in Receipt Account Number 5120 (IC 5-1-12-2). Please do not confuse "accrued interest" with "interest earned from investment of the proceeds of the sale". Investment of the proceeds must be in accordance with the investment law as found in IC 5-13-9. Interest earned from investment of the proceeds shall be receipted to Receipt Account Number 1510 of the Construction Fund or, if the governing board so designates, to the General Fund or Debt Service Fund (IC 5-13-9-6)

When securities are purchased as an investment of Construction Fund moneys, the check is recorded in Expenditure Account Number 60300 of the Construction Fund. The amount of the check is included in the total expenditures for the day which is posted to the appropriation Control Account, the Construction Fund, and the Control of All Funds in the Fund Ledger. The amount invested or the cost of securities purchased is also entered in the Clearing Account for Investments (Account Number 8500) on the Receipts-Purchase of Investments (Number 8510) side to retain the identity of the asset and maintain the balance in your accounting records. Also set up a Register of Investments (Form 350) to provide a record of the investments and their earnings for the fund from which the investment was made (Construction Fund).

If interest is received while the security is held by the school corporation, record the amount on the Register of Investments on the same line as the investment is recorded; also, receipt the interest to Receipt Account Number 1510 of the Construction Fund (or General Fund or Debt Service Fund, if designated). Post the interest to the fund and the Control of All Funds. Deposit the interest in the designated depository.

When the investment is sold or matures, receipt the sale price to the Construction Fund and to the Control of All Funds. Record in the receipt account for the Construction Fund the purchase price of the security in Account Number 6510, Sale of Securities, and any amount received in excess of the purchase price to Account Number 1510, Interest on Investments. Also, disburse from Clearing Account 8500 by entering on the disbursements side. Sale of Investments (Number 8520) an amount equal to the purchase price of the security previously entered in Number 8510 which will reduce the balance for the overall investment transaction in the Clearing Account to zero. Record the sale on the Register of Investments on the same line as the purchase was recorded. Any amount received in excess of the purchase price will be recorded on the Register of Investments as interest received.

IC 20-27-8-7 states: “When a school bus driver operates under a transportation or fleet contract, the compensation for the school bus driver or fleet contractor is determined and fixed by the contract on a per diem basis for the number of days on which: (1) the calendar of the school corporation provides that students are to attend school; (2) the driver is required by the school corporation to operate the bus on school related activities; and (3) inservice training is required by statute or authorized by the school corporation, including the safety meeting workshops required under section 9 of this chapter.”

The contract forms for school bus providers are prescribed by the State School Bus Committee and are the Driver Owned Equipment Contract for Transporting Children or the Fleet Contract for Transporting Children, as applicable, for a driver-owner or a fleet contractor respectively.

Methods of Payment

Employment Contracts “(a) If a school corporation owns in its entirety the school bus equipment in its entirety, the school corporation may employ a school bus driver on a school year basis in the same manner as other noninstructional employees are employed. (b) If a school corporation employs a school bus driver under subsection (a), the employment contract between the school corporation and the school bus driver must be in writing. (c) A school corporation that hires a school bus driver under this section shall purchase and carry public liability and property damage insurance covering the operation of school bus equipment in compliance with IC 9-25. (d) Sections 5 through 32 of this chapter do not apply to the employment of school bus driver hired under this section.” (IC 20-27-5-4)

Driver Furnishing Body Or Chassis Of School Bus

“(a) If a school bus driver is required to furnish the school bus body or the school bus chassis, or both, the governing body of the school corporation shall enter into a written transportation contract with the school bus driver. (b) The transportation contract may include a provision allowing the school bus driver to be eligible for the life and health insurance benefits and other fringe benefits available to other school personnel.” (IC 20-27-5-5)

Fleet Contracts; Benefits Package

“(a) When a fleet contractor is required to provide two (2) or more school buses and school bus drivers, the governing body of the school corporation shall enter into a written fleet contract with the fleet contractor. (b) The fleet contract may include a provision allowing the school bus drivers to be eligible for the life and health insurance benefits and other fringe benefits available to other school personnel.” (IC 20-27-5-6)

Transportation Or Fleet Contracts; Negotiations

“Transportation or fleet contracts may either be: (1) negotiated and let after receiving bids on the basis of specifications, as provided for in section 10 of this chapter; or (2) negotiated on the basis of proposals by a bidder in which the bidder suggests additional or altered specifications. A school corporation negotiating and executing a transportation contract shall comply with section 5 and sections 9 through 16 of this chapter. A school corporation negotiating and executing a fleet contract shall comply with sections 8 through 16 of this chapter.” (IC 20-27-5-7)

Payments should be in accordance with applicable Internal Revenue and State Department of Revenue reporting requirements.

- C

Capital Assets Establishing the Estimated Cost

Charge for Use of School Facilities

Compensatory Time - Fair Labor Standards Act

Computer Consortium Advancements and Training Grants

Cybersecurity Incidents - Reporting

We have previously been provided the Division of School and Community Nutrition of the Department of Education policy regarding vending machines which states in part that vending machines containing foods of minimal nutritional value cannot be sold in the food service area during the breakfast and/or lunch periods. These foods (carbonated beverages, candy, etc.) may however be sold outside the food service area during meal periods. The policy also provided that the sale of competitive foods (which meet certain nutritional requirements) may, at the discretion of the state agency and school food authority, be allowed in the food service area during the breakfast or lunch periods only if the income from the sale of such foods accrues to the benefit of the nonprofit food service or the school or student organizations approved by the school.

The Division of School and Community Nutrition policy allows the school food authority to determine where the income from the sale of competitive foods shall go in conformity with the above policy.

The State Board of Accounts is of the audit position that as long as the Division of School and Community Nutrition policy allows for a choice that the decision of which fund the vending revenue is to be accounted for in should be in accordance with the following:

1. The proceeds should accrue to that group's extra-curricular fund if a particular student group or organization manages the vending function.

2. The proceeds may go to the athletic fund if the vending in question is located at athletic events and managed by athletes or athletic department individuals.

3. The proceeds should go to the School Lunch Fund or the Extra-Curricular General Fund, Student Activity Fund or Concession Fund for the benefit of all students and spent consistent with page 6-3 of the "Accounting and Uniform Compliance Guidelines manual for Extra-Curricular Accounts" if no particular student group manages the vending function.

The Board of School Trustees should document their preference in the board minutes.

The possibility exists that an Audit Result and Comment may appear in a report if the School Lunch Fund fiscal status is adversely affected by the policy.

ESTABLISHING THE ESTIMATED COST OF CAPITAL ASSETS

When it is not possible to determine the historical cos of capital assets owned by a governmental unit, the following procedure should be followed.

Develop and inventory of all capital assets which are significant for which records of the historical costs are not available.

Obtain an estimate of the replacement costs of these assets. Through inquiry determine the year or approximate year of acquisition. Then multiply the estimated replacement cost by the factor for the year of acquisitions from the Table of Cost Indexes. The resulting amount will be the estimated cost of the asset.

In some cases estimated replacement cost can be obtained from insurance policies; however, if estimated replacement costs are not available from insurance policies, you should obtain or make an estimate of the replacement costs.

If the replacement cost is estimated to be $76,000.00 and the asset was constructed about 1946, then the estimated cost of the asset should be reported as $6,080.00.

$76,000.00 X .08 = $6,080.00