By MoneyWise Staff

Wednesday, January 8, 2020

On average, an employee’s salary makes up seventy percent of their total compensation, while the remaining thirty percent is compiled of fringe benefits. These “extras” often include; insurance, tuition reimbursement, childcare, retirement plan contributions, and discounts. In my first post about understanding your paycheck, I discussed the common terms on most pay stubs such as Gross Income and Net Pay. In this post, I’m going to dive deeper into the deductions listed on most pay stubs to explain where every penny goes to determine your take-home check.

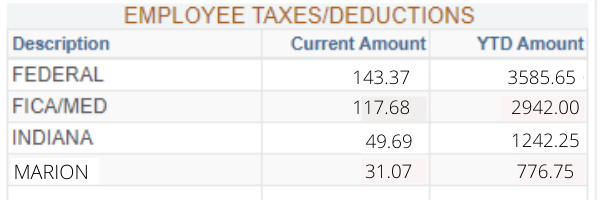

Before we talk benefits, I want to point out, about thirty percent of your Gross Income is reduced by taxes. Tax withholdings are dependent upon your W-4 form filling, the example pay stub (right) for John Smith is claiming one exemption. Multiple income tax withholdings are calculated according to a person’s claimed exemptions.

Federal Income Tax: Federal tax is calculated by tax brackets determined by taxable income and your tax filing status: single, married filing jointly, married filing separately, etc. There are  seven tax brackets, the progressive tax system allows your taxable income to be taxed in chunks according to the portion of income that falls in each tax rate category. John Smith is a single filer with $32,692.30 in annual taxable income. That puts him in the 12% tax bracket in 2019, but he only pays 10% on the first $9,700 of income, then he pays 12% on the rest up to $39,475 of taxable income, because the next bracket of 22% begins with $39,476 taxable income.

seven tax brackets, the progressive tax system allows your taxable income to be taxed in chunks according to the portion of income that falls in each tax rate category. John Smith is a single filer with $32,692.30 in annual taxable income. That puts him in the 12% tax bracket in 2019, but he only pays 10% on the first $9,700 of income, then he pays 12% on the rest up to $39,475 of taxable income, because the next bracket of 22% begins with $39,476 taxable income.

FICA/Medicare: Federal Insurance Contribution Act (FICA) tax is a payroll tax that funds Social Security benefits and Medicare health insurance. This tax is split between employers and employees who both pay 7.65% (6.2% for Social Security, 1.45% for Medicare). You can calculate these individually but for many employers, these are lumped together. John Smith is paying $95.38 for FICA and $22.30 for Medicare each pay period, equaling $117.68 together.

State Income Tax: Some states do not collect income tax, some collect a flat rate and some impose a progressive tax meaning people with higher levels of income pay higher taxes. The state of Indiana has a flat tax rate of 3.23%. John Smith will pay $49.69 per pay period or $1,242.25 a year in state income tax.

Local Tax: This is also known as county tax, in Indiana, this is based on your County of residence as of January 1 per tax year. For John Smith's pay stub, he is a Marion county resident with a tax rate of 0.0202%.

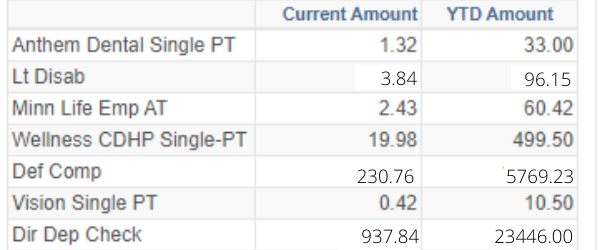

Insurance Premiums: Most pay stubs itemize the insurance premiums for the services you selected. For health, dental, vision, life and disability, your employer likely requires you to pay  a portion of the premium. These costs are deducted from your gross pay. If your employer offers TaxSaver benefits, this prevents you from paying tax on the premiums. John Smith has medical, dental, vision and life insurance on a single plan, rather than a family plan. If applicable, this section of your pay stub is also where you will find disability insurance. For state of Indiana employees, I have found that the employee portion of the premium for disability insurance is about 0.0025% per paycheck.

a portion of the premium. These costs are deducted from your gross pay. If your employer offers TaxSaver benefits, this prevents you from paying tax on the premiums. John Smith has medical, dental, vision and life insurance on a single plan, rather than a family plan. If applicable, this section of your pay stub is also where you will find disability insurance. For state of Indiana employees, I have found that the employee portion of the premium for disability insurance is about 0.0025% per paycheck.

Other deductions: Depending on your employer, there may be additional deductions. For example, if you choose to donate part of your paycheck to a charity that partners with your employer — like the State Employees' Community Campaign (SECC), this should appear on your pay stub.

Deferred Compensation: These funds are also known as your retirement money. The tax is deferred on this income until payout which is likely in your retirement years. The strategy with this is that you benefit from a lesser tax burden at the pay out because you expect to be in a lower tax bracket after retiring, than when you initially earned the income.

The Direct Deposit amount is your take-home pay, also known as net pay. Most pay stubs include how much you've received year to date (YTD).

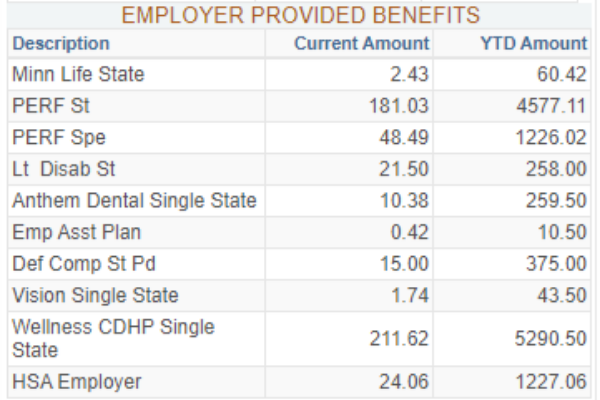

The last section of the state employee paycheck, Employer Provided Benefits, is my favorite. Most employers who offer benefits are required to pay a portion of the premiums for the employee’s coverage. For example, while John Smith pays $1.22 per pay period towards his premium for dental insurance, his employer pays $10.38 per pay period towards the premium. This is the same for medical, vision, life and disability insurance premiums.

Let’s talk about retirement accounts, this will be different for non-state employees, but I hope this information will provide some insight and spur you to find out more about how your employer retirement accounts are structured.

On John Smith’s pay stub, we see the deductions titled:

Def Comp.: This refers to a Target Retirement Fund account offered by Hoosier S.T.A.R.T., sometimes also referred to as a 457 plan, only for state and local government employees and some non-profits. This is similar to a 401(k) plan that might be offered by a private employer.

PERF St and PERF Spe: This could be referred to as your state employee pension and the state pays 100% of the cost. While employed, the state will continue to put money into these accounts, this is provided by INPRS. This appears as two separate contributions on the pay stub because a portion is invested via an annuity and the other via Target Date Funds.

Def Comp St Pd: This is another Hoosier S.T.A.R.T. sponsored retirement plan, sometimes referred to as a 401(a) plan. The unique feature of this plan is, state employees receive a $15-per-paycheck matching contribution which equates to $30/month or $390/year of “free money”. Another way of thinking is to view the state’s match as BOGO, you put in $15 a payday and the state will match that giving you $15 in your account each payday. It’s wise to contribute at least up to the match so you’re getting the benefit of all the money your employer is offering and padding your retirement savings.

HSA Employer: The last thing to mention is a Health Savings Account (HSA). If enrolled in a High Deductible Health insurance Plan (HDHP), you qualify for an HSA, an account allowing you to save specifically for medical costs. As an employer, the state of Indiana contributes thirty-nine percent of your annual deductible into your HSA. Your contributions to an HSA are pre-tax or tax-deductible and you don’t pay tax on the account’s growth nor the withdrawals if used for eligible expenses. An HSA is similar to a Flexible Spending Account (FSA), although an FSA does not allow for the leftover funds to roll over to the next year, and an FSA is often better paired with a lower deductible health insurance plan.

It’s important to stay on top of tracking your deductions and contributions. Any errors are your responsibility to find and report, the last thing you want is for an error to be repeated through several pay periods.

I can write from experience, my first year as a state of Indiana employee, somewhere a mistake was made by HR. The information on my W-4 was incorrectly filed in the system. For about seven months my taxes were withheld in “married” filing status, although I would be filing as “single”. I noticed this on my paystub a little too late in the year, and when tax filing time came around, I owed more than I was excited to pay.

If you have questions about any of the information listed on your pay stub, be sure to contact your human resources representative.

Blog topics: Budgeting, Credit, Archive

The MoneyWise Matters blog has a wealth of information about managing money and avoiding fraud. You can look through the complete archive here.