County Bulletins

Search for Keywords

- A

Agricultural Associations and Societies - Grants

Allocation of Registered Motor Vehicle Penalties

Annual Reports

100-R and Annual Financial Report

Appropriations

Construction Or Repair Of Bridges

Proceeds From Property Damage Claims

When Required By County Council Only

Approval of Accounting Forms and Systems

Assessment

IC 5-13-6-3 allows counties to advance taxes units amounting to 95% of the amount such unit would get in a distribution of the taxes collected for the unit at the time of advancement. The term “taxes collected” includes property tax and license excise tax. The request for an advance tax draw must be filed at least thirty (30) days before the treasurer is required to make the advance.

The following procedures should be followed:

1. The collections for each taxing district within the municipal corporation, as shown by the records of the county treasurer, should be multiplied by 95%.

2. Divide the answer under (1) by the total tax rate for the taxing district to obtain the factor to be used in apportioning the tax.

3. Multiply the factor by the tax rate for the fund for which the advance draw is requested, to arrive at the maximum amount which can be advanced.

4. Issue an application to pay and quietus in favor of the county treasurer for the amount to be advanced to the credit of the fund for which advanced and issue a warrant therefore in favor of the proper officer of the municipal corporation.

The treasurer shall enter the advance on line 42 on the left side of the Daily Balance of Cash and Depositories and such amounts are deducted from the amount of total taxes collected shown on line 41. This will leave the total amount of taxes to be settled on line 43.

It is imperative that advances be recorded by the treasurer to insure the proper amounts are distributed at Settlement.

The General Assembly amended IC 6-1.1-15-11, IC 36-2-6-3, and IC 36-2-4.5 so that claims under these codes are no longer required to be published unless it is an allowance made by the court. IC 36-2-6-3 states: “(a) This section does not apply to claims for salaries fixed in a definite amount by ordinance or statute, per diem of jurors, and salaries of officers of a court. (b) The county auditor shall publish all allowances made by courts of the county. Court allowances shall be published at least three (3) days before the issuance of warrants in payment of those allowances. Allowances subject to this section shall be published as prescribed by IC 5-3-1 except that only one (1) publication in two (2) newspapers is required. (c) A county auditor who issues warrants in payment of allowances made by a court of the county, before compliance with subsection (b), commits a Class C infraction. (d) A county auditor shall publish one (1) time in accordance with IC 5-3-1 a notice of all allowances made by a circuit or superior court. The notice must be published within sixty (60) days after the allowances are made and must state their amount, to whom they are made, and for what purpose they are made.” Further explanation and examples of court jurisdiction may be found in the Accounting and Uniform Compliance Guidelines for County Auditor.

AGRICULTURAL ASSOCIATIONS AND SOCIETIES (FAIRS) – GRANTS FROM COUNTY

The board of county commissioners may make an allowance from the general fund to any 4-H Club Association having for its purpose the promotion of agriculture or horticultural interests of the county. A petition signed by thirty or more resident freeholders is required and same petition, without the signatures, must be published in a newspaper of general circulation. If a petition in remonstrance be signed by more resident freeholders than the petition for such grant, the board of county commissioners shall dismiss the first petition and take no further action. Any such petition, after final acceptance, shall be effective for one or more years, not to exceed five years, such time to be determined by the board of county commissioners. (IC 15-14-7-3)

The board of county commissioners may levy an annual tax of not to exceed $0.0333 on each $100 valuation for construction, operation or maintenance of any building owned or operated by such association, only until the building has been constructed, and in no event for a period more than five years.

After a building has been constructed the county council may levy an annual tax of not to exceed $0.0067 on each $100 valuation for operating and maintaining such building. (IC 15-14-7-4)

The county councils and boards of county commissioners may appropriate and pay to any agricultural fair or association or 4-H club, a sum not exceeding four cents ($0.04) on each $100 valuation, from the general fund for necessary costs and expenses, premiums, and judging. This appropriation cannot include purses for speed contests and cannot be extended to any association conducting fair for gain, not to street fairs or exhibitions. (IC 15-14-9-2)

ALLOCATION OF PENALTIES COLLECTED FOR FAILURE TO TIMELY REGISTER MOTOR VEHICLES

IC 9-18.1-2-6 states: “A nonresident may that becomes an Indiana resident may operate a vehicle on a highway for not more than sixty (60) days without registering the vehicle under this article, if the vehicle in registered in accordance with the laws for the jurisdiction in which the nonresident was a resident.”

IC 9-18.1-2-11 states: “A person that fails to register a vehicle that is required to be registered under this chapter commits a Class C infraction.” IC 34-28-5-17(b) states: “In addition to…any judgment assessed under IC 34-28-5…, a person that violates IC 9-18.1-2-3 shall be assessed a judgment equal to the amount of excise tax due on the vehicle under IC 6-6-5 or IC 6-6-5.5…”

IC 34-28-5-17 goes on to require the clerk to collect the additional judgment and transfer the additional judgments collected to the county auditor on a calendar year basis. The auditor shall distribute the funds to the law enforcement agencies, including the state police, responsible for issuing citations to enforce section 1 of this chapter. The percentage of the funds distributed to an agency equals the percentage of the total number of citations issued by the agency for the purpose of enforcing section 1 of this chapter during the applicable period.

Funds distributed under this section shall be used for any law enforcement purpose including contributions to the pension fund of the law enforcement agency.

To facilitate the handling and allocation of these fees under IC 34-28-5-17, the clerk should use General Form No. 367 (1984) entitled “Clerk’s Report to Auditor of Additional Judgments for Excise Tax.” In using this form the following procedures should be observed:

1. The clerk of the court which collects these penalties must include a memorandum with the remittance which shows the number of citations filed in the court by each law enforcement agency for failure to timely register a motor vehicle. Such memorandum could be as follows:

Law Enforcement Agency (Number of Citations)County Sheriff (6)

Urban City Police (2)

Best Town Marshall (2)

Total (10)2. The amount received from the clerk would be receipted to a fund called “Judgments Due Law Enforcement” fund #7305

3. The amount receipted to the Judgments Due Law Enforcement Agencies Fund would then be multiplied by the percentage of the total citations which were filed by each law enforcement agency during the applicable period to determine the amount due each law enforcement agency.

Using the number of citations shown in Item 1 above an example of a worksheet to determine the allocation of funds is as follows:

Amount Received From Court $450.00

Law Enforcement Agency Number of Citations Percentage of Total Amount Due Agency County Sheriff 6 60% $270 Urban City Police 2 20% $90 Best Town Marshall 2 20% $90 Total 10 100% $450 4. After the amount due each law enforcement agency is determined a warrant should be issued to the disbursing officer of the particular governmental unit for the amount due. The warrant should be accompanied by a brief explanation showing the purpose of the distribution.

5. The amount due to the county on account of citations filed by the sheriff’s department should be receipted by quietus to a fund called “Motor Vehicle Registration Penalties” Fund #1214. This fund can be expended for any law enforcement purpose. However, disbursement should be by county warrant and only after a duly itemized claim has been approved by the Board of County Commissioners.

6. Any amount due on account of citations issued by the state police would be sent to the Auditor of State

ANNUAL REPORTS

SUPPLEMENTAL ANNUAL REPORT AND USE BY THE COUNTY AUDITOR FOR THE ANNUAL REPORT

The supplemental annual report forms are submitted by other county offices and departments to be used by the county auditor to provide complete financial information for the annual report by reporting financial activity that is maintained outside of the county auditor’s system. The supplemental annual reports are only to be submitted with financial activity that is not eventually accounted for in the county’s general ledger system. For example, the recorder’s office may maintain a cashbook and an outside bank account, but those receipts are turned over monthly and accounted for monthly in the auditor’s system and so would not be reported on the supplemental annual report, even that portion at year end that has yet to be remitted to the county auditor’s office.

The common financial activities that are maintained outside of the county auditor’s system are the clerk’s trust (including ISETS), jail commissary, sheriff’s inmate trust, county home commissary, and county home residents’ trust. Redevelopment commission funds for capital projects (bond proceeds) and debt service (incremental tax) should also be considered.

There are two exceptions to the rule that only financial activity that is not eventually accounted for in the county’s general ledger system be reported on the supplemental annual report to be included in the annual report by the county auditor.

One exception is the clerk’s trust fund. The clerk’s trust fund includes receipts that are turned over monthly and accounted for in the county auditor’s system. This activity will not be separated out. The financial activity that will be reported on the supplemental annual report by the clerk and in turn reported by the county auditor on the annual report under the clerk’s trust fund will be inclusive of the activity for these receipts.

The other exception is the after December settlement collections by the treasurer. The county treasurer will reflect on the supplemental annual report as the beginning balance the previous year’s ending balance. The disbursements column will be the same as the beginning balance. This has the effect of reversing out the prior year activity. The amount for receipts and ending balance is arrived at by taking the ending balance on the treasurer’s daily cash sheet for the current December 31th balance of taxes to be settled + total other sources. The county auditor will reflect these amounts as the beginning balance, receipt, disbursement, and ending balance on the annual report under the after settlement collections fund. This is the only fund that provides the timing difference of financial activity that has not yet been recorded in the auditor’s general ledger system.

Three resources that should be referred to for any updates to this process are the Accounting and Financial Reporting Regulation Manual, which may be found on our web site under manuals, the user guide for the gateway annual report and instructions for the supplemental annual financial report, both of which may be found on our web site under gateway annual report.

Certified Report of Names, Addresses, Duties and Compensation of Public Employees (100R) and Annual Financial Report (AFR)

Pursuant to IC 5-11-13-1, all governmental units in the state must file the certified personnel report (Form 100R) in January of each year with the State Board of Accounts. Also, pursuant to IC 5-11-1-4, all local governmental units in the state must file an Annual Financial Report (AFR) not later than 60 days after the close of each fiscal year. The Indiana Gateway for Government Units (Gateway) system was created to collect both of these reports.

Due to the importance of these reports, the State Examiner has established the following procedures for reports not filed timely:

If either the 100R or the AFR are not filed by the statutory due date, the State Board of Accounts will subpoena the fiscal officer to appear in our Indianapolis office with the information necessary to complete the 100R or AFR, as applicable. This subpoena will be served either by certified mail or through personal service by a representative of the Office of the Attorney General (OAG).

If the fiscal officer does not appear or does not submit the 100R or AFR in response to the subpoena, the State Examiner will send a notification to the OAG requesting the OAG to compel the fiscal officer to appear in court to answer as to his or her failure to file the report. The State Examiner may also send notification of the officer’s failure to comply with the law to the local prosecuting attorney.

Indiana Code 5-11-1-10 addresses the penalty for not filing a required report and not following the directions of the State Examiner:A public officer who:

(1) fails to make, verify, and file with the state examiner any report required by this chapter;

(2) fails to follow the directions of the state examiner in keeping the accounts of the officer's office;

(3) refuses the state examiner, deputy examiner, field examiner, or private examiner access to the books, accounts, papers, documents, cash drawer, or cash of the officer's office; or

(4) interferes with an examiner in the discharge of the examiner's official duties; commits a Class B infraction and forfeits office. (Our emphasis)

If you need submission rights or have any questions regarding the use of Gateway, please contact our help desk at gateway@sboa.in.gov. Also, please feel free to contact our Directors of Audit Services if you are having difficulty completing your 100R or AFR. Contact information is available on our website at www.in.gov/sboa.

APPROPRIATIONS

It is possible to appropriate more money in a particular year after the budget is approved if the proper officers determine that additional appropriations re needed. See IC 6-1.1-18-5. A public hearing must take place and proper notice must be given in compliance with IC 5-3-1-2. For counties, IC 36-2-5-12 allows the council to make additional appropriations at a special meeting. To determine if the additional appropriations need the approval of DLGF, see IC 6-1.1-18-5 for guidance. If the additional appropriation is for a fund that DLGF has certified the budget, rate or levy, then DLGF must approve any additional appropriation to that fund.

APPROPRIATION FOR CONSTRUCTION OR REPAIR OF BRIDGES

The budgetary laws specifically (IC 36-2-5-7) states in part:

"…the county executive shall prepare an itemized estimate of all money drawn by the members of the executive and all expenditures to be made by the executive or under its orders during the next calendar year. Each executive's budget estimate must include:…(2) the expense of constructing and repairing bridges, itemized by the location of and amount for each bridge;…"

Cumulative Bridge Fund

IC 8-16-3-3(e) states: "An appropriation from the bridge fund may be made without the approval of the department of local government finance if:

(1) the county executive requests the appropriation; and(2) the appropriation is for the purpose of constructing, maintaining, or repairing bridges, approaches, or grade separations."

APPROPRIATIONS CARRIED FORWARD (ENCUMBRANCES)

Appropriations may be carried forward to the following year if any of the following conditions exist:

1. A lawful contract has been entered into with a vendor or contractor on or before December 31 and all or a part of the contract has not been paid.

2. A purchase order has been issued on or before December 31, entered as an encumbrance against an existing appropriation, and isn’t paid as of December 31.

3. Proceeds of a bond issue have been duly appropriated and remain unexpended as of December 31.

4. Appropriations which are obligated by a contract or a agreement executed on or before December 31, between the county and any federal or state agency, such as a criminal justice planning grant, local road and street project, or federal grant requiring local matching funds.

Only the amount required to meet the balance due on a contract or purchase order may be carried forward; the amount remaining in the appropriation account shall revert to the fund from which appropriated.

Whenever a valid appropriation has been lawfully encumbered by a contract or by the issuance of a purchase order, the appropriation to the extent of the encumbrance may be carried forward to the succeeding year and made available for payment of the obligation which encumbered it. Only so much of the appropriation as is lawfully encumbered may be carried forward. All appropriations not lawfully encumbered by contract or purchase order revert at the close of the year.

We suggest the proper officials of the county make a listing of these encumbered items and make it part of their minutes in their last business meeting of the year. The Department of Local Government Finance should be sent a copy of the listing. Keep in mind the appropriations encumbered and carried forward can be used for no other purpose other than the purchase order or the contract for which they were appropriated.

APPROPRIATIONS – PROCEEDS FROM PROPRERTY DAMAGE CLAIMS

IC 6-1.1-18-7 states: “Notwithstanding the other provisions of this chapter, the fiscal officer of a political subdivision may appropriate funds received from a person as defined by IC 6-1.1-1-10 if:

(1) The funds are received as a result of damage to property of the political subdivision; and

(2) The funds are appropriated for the purpose of repairing or replacing the damage property.

However, this section applies only if the funds are in fact expended to repair or replace the property within the twelve (12) month period after they are received.”

IC 6-1.1-18-9 states: “Notwithstanding the other provisions of this chapter, the proper officer or officers of a political subdivision may:

(1) reappropriate money recovered from erroneous or excessive disbursements if the error and recovery are made within the current budget year; or

(2) refund, without appropriation, money erroneously received.”

IC 6-1.1-18-6 states the following, “The proper officers of a political subdivision may transfer money from one major budget classification to another within a department or office if: 1) they determine the transfer is necessary; 2) the transfer does not require the expenditure of more money than the total amount set out in the budget as finally determined by this article; 3) the transfer is made at a regular meeting and by proper ordinance or resolution; and 4) the transfer is certified to the county auditor. A transfer may be made under this section without notice and without the approval of the department of local government finance.”

This statute is addressing transfers from one major classification to another major classification within a department. For example, a transfer in the County Auditor’s budget from a 300 account to a 200 account. No transfers are allowed from one department to another, i.e. from the County Auditor’s budget to the County Treasurer’s budget. To do this would require a budget reduction in one department and an additional appropriation to the other department by the County Council. Transfers within a major classification in a department may be made without County Council action unless your local policy is for all transfers to go before the County Council. (i.e. from a 200 account to another 200 account within the County Auditor’s budget)

APPROPRIATIONS - WHEN NOT REQUIRED

In some instances statutory authority is given the county auditor to make disbursements without an appropriation having been previously made for the specific purpose. Examples are as follows:

1. Premiums on official bonds. (IC 5-4-5-3)

2. Tax refunds. (IC 36-2-9-14)

3. Any money belonging to the state, school fund, or any fund of any township, town or city and commanded by law to be paid to such municipality. (IC 36-2-9-14)

4. Any money collected from a taxpayer from an assessment and is being paid on a public improvement such as ditches and drains. (IC 36-2-9-14)

5. Redemption of property sold at tax sale. (IC 36-2-9-14)

6. Per diem, lodging, and mileage for conferences called by State Board of Accounts. (IC 5-11-14-1)

7. Examination of records. (IC 5-11-4-4)

8. Line fence assessments. (IC 32-26-9-4)

9. Federal grants, if advanced and not received as a reimbursement of expenditures.

10. Advances to conservancy districts on order of court. (IC 14-33-7-15)

11. Surplus tax refunds. (IC 6-1.1-26-5)

12. Refund of money erroneously received. (IC 6-1.1-18-9)

13. Correction of errors in posting. (IC 6-1.1-18-9)

14. Jail commissary fund. (IC 36-8-10-21)

15. Investment of funds.

16. Title IV-D incentive fund (clerk and prosecuting attorney portions). (IC 31-25-4-23)

17. Repayment of temporary loans.

18. Recorder’s records perpetuation fund. (IC 36-2-7-10)

19. Firearms Training Fund. (REFUNDS ONLY) (IC 35-47-2-3).

20. Accident Report Fund. (IC 9-29-11-1)

21. County Law Enforcement Continuing Education Fund. (IC 5-2-8-1)

22. Special Death Benefit Fee Fund. (IC 5-10-10; IC 35-33-8-3.2)

23. Military Fines. (IC 10-16-9-3)

24. Payment of accrued interest on cemetery trust funds paid on the last Monday in January (IC 23-14-70-2).There may be other laws under which funds may be disbursed without appropriation; however,

appropriations are required before disbursements may be made from any fund subject to the Budget Laws

unless specific authority to disburse without appropriation is provided by law.APPROPRIATIONS - REQUIRED BY COUNTY COUNCIL ONLY

The following is a list of funds which require county council approval of an appropriation. Due to the nature of the funds, the Department of Local Government Finance does not require submission of an additional appropriation request before the local appropriation can be approved.

1. County Supplemental Adult Probation Services Fund. (IC 35-38-2-1)

2. County Supplemental Juvenile Probation Services Fund. (IC 31-40-2-2)

3. County User Fee Fund. (IC 33-37-8-6)

4. Plat Book Fund. (IC 36-2-9-18)

5. Local Emergency Right to Know Fund. (IC 13-25-2-10.6)

6. Pretrial Diversion Fund (Excess). (IC 33-37-8-7)

7. Community Corrections Home Detention Fund. (IC 11-12-7-3; IC 35-38-2.5-8)

8. County Extradition Fund. (IC 35-33-14)

9. County Misdemeanant Fund (IC 11-12-2-11)

10. Supplemental Public Defender Services Fund. (IC 33-40-3-2)

11. Emergency Telephone System Fund. (IC 36-8-16.7-38)

12. Cumulative Bridge Fund. (IC 8-16-3-3)

13. Local Health Maintenance Fund. (IC 16-46-10)

14. Vehicle Inspection Fund. (IC 9-17-2-12)

15. Community Corrections Grant and Project Income Fund (IC11-12-2-2)

16. Payments from State or Federal Grant as reimbursement of expenses (IC 6-1.1-18-7.5)

17. Firearms Training Fund. (IC 35-47-2-3).APPROVAL OF ACCOUNTING FORMS AND SYSTEMS

The State Board of Accounts is charged by law with the responsibility of prescribing and installing a system of accounting and reporting which shall be uniform for every public office and every public account of the same class and contain written standards that an entity that is subject to audit must observe. The system must exhibit true accounts and detailed statements of funds collected, received, obligated and expended for or on account of the public for any and every purpose. It must show the receipt, use and disposition of all public property and the income, if any, derived from the property. It must show all sources of public income and the amounts due and received form each source. Finally it must show all receipts, vouchers, contracts, obligations, and other documents kept, or that may be required to be kept, to prove the validity of every transaction. [IC 5-11-1-2]

The system of accounting prescribed is made up of the uniform compliance guidelines and the prescribed forms. A prescribed form is one which is put into general use for all offices of the same class.

Computer hardware, software and application systems can now produce exact replicas of the forms prescribed by the State Board of Accounts. An exact replica of a prescribed form is a computerized form that incorporates all of the same information as the manual prescribed form. Prescribed form replication is the preferred approach from the State Board of Accounts’ position. These exact replicas are the equivalent of the prescribed form and require no further action for the county to install the form within their accounting system.

Governments are required by law to use the forms prescribed by this department. However, if it is desirable to use a form other than the prescribed manual form, that is not an exact replica; the new form must be approved by State Board of Accounts.All forms previously approved by sending copies to State Board of Accounts and receiving a form approval letter are approved with the conditions contained within the letter. All forms previously approved by the adoption of a resolution as allowed by County Bulletin article on Approval of Accounting Forms and Systems, published in Volume 354, pages 13-16 are also considered approved.

After April 1, 2014, if a government implements, consistent with the provisions of Indiana Code and Uniform Compliance Guidelines, an automated accounting system that is to be considered for approval, the responsible official is not required to maintain the prescribed forms replaced by the automated system while awaiting the approval. New forms must be in place during at least one (1) State Board of Accounts audit and must not be an element of an audit finding or audit result and comment that is responsible or partially responsible for an exception found during an audit to be considered approved. The government is responsible for placing on new forms the year of installation in the upper right corner. This reference should be similar to “Installed in ______________ County, (Year).” The county must maintain and present for audit a log of forms installed after April 1, 2014 with the year installed for all forms that replace forms prescribed by State Board of Accounts.

The government agrees to comply with the following conditions, if applicable, for any new forms installed.

1. The forms and system installed are subject to review and/or recommendations during audits of the government to ensure compliance with current statutes and uniform compliance guidelines.

2. The government shall continue to maintain all prescribed forms not otherwise covered by an approval.

3. All transactions that occur in the accounting system must be recorded and accessible upon proper request. Transactions can be maintained electronically, with proper backups, microfilmed, or printed on hardcopy. These transactions include, but are not limited to, all input transactions, transactions that generate receipts, transactions that generate checks, master file updates, and all transactions that affect the ledgers in any way. The system must be designed so that changes to a transaction file cannot occur without being processed through an application.

4. The ability must not exist to change data after it is posted. If an error is discovered after the entry has been posted, then a separate correcting entry must be made. Both the correcting entry and the original entry must be maintained.

5. If the unit owns the source code, sufficient controls must exist to prevent unauthorized modification. If the unit does not own the source code, the vendor shall provide representatives of the State Board of Accounts with access to all computer source codes for the system upon request for audit purposes. In addition, the vendor shall provide representatives of the State Board of Accounts with a document describing the operating system used, the language that the source code is written in, the name of the compiler used, and the structure of the data files including data file names, data file descriptions, field names, and field descriptions for the system.

6. Any receipts, checks, purchase orders, or other forms that require numbering shall be either pre-numbered by an outside printing supplier or numbered by the units computer system with sufficient controls installed in the system to prevent unauthorized generation of the form or duplication of numbers.

7. All receipts must be either in duplicate or recorded in a prescribed or approved register of receipts.

8. All checks must be either in duplicate or recorded in a register of checks generated by the computer.

9. Recap sheets for each deposit for deposit advices, if applicable, will be maintained indicating direct deposits. Individual wage assignment agreements will be kept on file to support direct deposit.

10. "Installed by __________ County, (Year)" shall be printed, in the upper right corner, on each approved form furnished by a printing supplier and, when practical, on those printed from accounting systems at the unit. Upon the installation of a new form the form will be entered on a log for this purpose with the date of installation; and the name and number of the prescribed form replaced. The log must be available for audit.

11. The government officials are responsible to ensure that forms and accounting systems installed comply with the uniform compliance guidelines for information technology services published in the County Bulletin and accounting manuals. This includes ensuring that customization of the system done by the vendor for implementation at the government is done in such a manner that the system remains compliant.

12. In the event a change is required due to the passage of a State or Federal law, the government agrees to implement the change in a timely manner.

ASSESSMENT

"Before the assessment date of each year, the county auditor shall deliver to each township assessor (if any) and the county assessor the proper assessment books and necessary blanks for the listing and assessment of personal property." (IC 6-1.1-3-5)

Per IC 6-1.1-4-13.6, the county assessor shall determine the values of all classes of commercial, industrial, and residential land (including farm home sites) in the county using guidelines determined by the department of local government finance. The assessor determining the values of land shall submit the values, all data supporting the values, and all information required under rules of the department of local government finance relating to the determination of land values to the county property tax assessment board of appeals by the dates specified in the county’s reassessment plan.

If the county assessor fails to determine land values before the deadlines in the county's reassessment plan, the county property tax assessment board of appeals shall determine the values. If the county property tax assessment board of appeals fails to determine the values before the land values become effective, the department of local government finance shall determine the values.

The county assessor shall notify all township assessors in the county of the values. Assessing officials shall use the values determined under this section.

A petition for the review of the land values determined by a county assessor under this section may be filed with the department of local government finance not later than forty-five (45) days after the county assessor makes the determination of the land values. The petition must be signed by at least the lesser of:

one hundred (100) property owners in the county; or five percent (5%) of the property owners in the county.Upon receipt of a petition for review, the department of local government finance shall review the land values determined by the county assessor; and after a public hearing, shall: approve; modify; or disapprove the land values.

ASSESSMENT REGISTRATION NOTICES

IC 6-1.1-5-15 states before an owner of real property demolishes, structurally modifies, or improves it at a cost of more that five hundred dollars ($500) for materials and/or labor, the owner or his agent shall:

1. file with area plan commission or the county assessor an assessment registration notice on a form prescribed by the Department of Local Government Finance, and the commissioner or assessor charges a five dollar ($5) filing fee. or

2. obtain a permit from an agency, official of the state, or a political subdivision, then the owner is not required to file an assessment registration notice.

A township or county assessor shall immediately notify the county treasurer if the assessor discovers property that has been improved or structurally modified at a cost of more than five hundred dollars ($500) and the owner of the property has failed to obtain the required building permit or file an assessment registration notice.

Any person who fails to obtain one of these is subject to a civil penalty of one hundred dollars ($100). The county treasurer shall include the penalty on the person’s property tax statement and collect it in the same manner as delinquent personal property taxes under IC 6-1.1-23. However, if a person files a late registration notice, the person shall pay the fee, if any, and the penalty to the area plan commission or the county assessor at the time the person files the late registration notice. Both the five dollar ($5) fee and the one hundred dollar ($100) penalty would be receipted to the County Property Reassessment Fund.

ASSESSORS - TOWNSHIP - BOND PREMIUM – PAYMENT

The bond premium on the official bond of the township assessor should be paid from county funds and not from township funds.

IC 5-4-1-18 requires the township assessor to file an individual surety bond, blanket bond, or crime insurance policy in the amount fixed by the fiscal body at not less than eight thousand five hundred dollars ($15,000). Statutes do not require the deputy assessor to execute a bond; however, such bond may be required by the elected township assessor. When so required, such bond must be recorded in the office of county recorder.

- B

Bank/Credit Card Payments to Counties

Benefits

Establishing Employee Benefits

Board of Finance

Bonds

Premium and Accrued Interest on Bonds Issued and Sold

Borrowing

Breaks (Paid) for Expressing Milk

BANK RECONCILEMENTS

Indiana Code 5-13-6-1(e) requires that bank reconcilements be completed monthly. During an audit we would expect to see bank reconcilements performed each month. Failure to complete bank reconcilements on a monthly basis could result in an audit finding. This would apply to all county bank accounts including those held outside of the county treasurer, such as held by the Recorder, Clerk, and Sheriff. In addition to compliance with statute, monthly bank reconcilements provide internal controls to achieve the safeguarding of public assets.We have received numerous reports that bank routing and account information is being used to create false checks that are clearing bank accounts and stealing public funds. If the unauthorized payments from the account are brought to the attention of the bank in a timely manner, the bank will replace the amount that was stolen. However, if you are not reconciling monthly, you would not be aware of these fraudulent transactions and the delay in reporting these fraudulent transaction to the bank may make it more difficult to get the bank to restore the funds to the bank account. If the money is being held in trust such as the Sheriff’s Inmate Trust Account or the Clerk’s Trust or ISETS Accounts, the county is responsible to make the accounts whole. If money is misappropriated, the fraudulent activity is not reported timely to the bank, and the delay in reporting is due to a failure to reconcile the bank accounts each month, the elected officer may be held personally responsible for replacing the stolen funds.

We realize that it is possible to have unidentified variances between the bank statements and your record balance and that it may take some time to identify those items and complete the reconcilement. However, do not let those issues prevent you from continuing to reconcile each month, even if you are carrying those unidentified variances forward each month. At the very minimum, you should review the bank statement monthly and verify that all of your recorded deposits are credited to your account and all withdrawals from the account are transactions that trace to checks prepared by your office or electronic funds transfers that you have authorized. In that way you would catch any bank errors in a timely manner. In addition you would be able to identify any fraudulent activity as early as possible.

BANK/CREDIT CARD PAYMENTS TO COUNTIES

A payment to a county may be made by any of the following financial instruments that the fiscal body of the county authorizes for use:

1. Cash

2. Check

3. Bank Draft

4. Money Order

5. Bank card or credit card

6. Electronic fund transfer

7. Any other financial instrument authorized by the fiscal bodyIf there is a charge to the county for the use of a financial instrument, the county may collect a sum equal to the amount of the charge from the person who uses the financial instrument.

If authorized by the fiscal body of the county, the county may accept payments with a bank card or credit card. However, the procedure authorized for a particular type of payment must be uniformly applied to all payments of the same type.

The county may contract with a bank card or credit card vendor for acceptance of bank cards or credit cards. The county may pay any applicable bank card or credit card service charge associated with the use of a bank card or credit card. However, if there is a vendor transaction charge or discount fee the county may collect from the person using the card an official fee that does not exceed the transaction charge or discount fee and/or a reasonable convenience fee. The convenience fee may not exceed $3 and must be uniform regardless of bank or credit card used. (IC 36-1-8-11)

It is our position that such a fee be deposited in the general fund.

RESPONSIBILITY FOR ESTABLISHING VACATION, SICK LEAVE, PAID HOLIDAYS, AND OTHER SIMILAR BENEFITS

IC 5-10-6-1(b) states: “Employees of the political subdivisions of the state may be granted a vacation with pay, sick leave, paid holidays, and other similar benefits by ordinance of the legislative body of a county, city, town, township, or controlling board of a municipally owned utility, board of directors or regents of a cemetery, or board of trustees of any library district.”

It is imperative that the county adopt a policy regarding leave rules and other benefits. The State Board of Accounts will be auditing to see that the employees of the county are following the adopted policy.

BOARD OF FINANCE – ANNUAL MEETING

IC 5-13-7-6 requires each local board of finance to meet annually after the first Monday and on or before the last day of January. At the annual meeting the board of finance shall elect from the board's membership a president and secretary. The officers hold office until the officer's successors are elected and qualified.

The board of finance shall also receive and review the written report of the investing officer that summarizes the county's investments during the previous year. The report must contain the name if each financial institution, governmental agency or instrumentality or other person with whom the county invested money during the previous calendar year.

The board of finance is to review overall investment policy of the county.

Each county treasurer shall deposit the boat excise taxes collected by the Bureau of Motor Vehicles and the boat excise taxes distributed by the Auditor of State under IC 6-6-11-29 into a boat excise tax fund. Such fund shall be accounted for by county treasurers on the Other Sources sections of the Treasurer’s Daily Balance of Cash and Depositories.

IC 6-6-11-33 states: “The county treasurer shall do the following:

(1) At the same time a settlement is made with the county auditor under IC 6-1.1-27, file a report, on a form prescribed by the state board of accounts, with the county auditor concerning the boat excise taxes received during the preceding six (6) month period.

(2) In the manner and at the times prescribed in IC 6-1.1-27, make a settlement with the county auditor for the boat excise taxes received under this chapter.

(3) In the manner prescribed by the state board of accounts, maintain records concerning the boat excise taxes received and distributed.”

Because of new guidance we received from the Attorney General, we are changing our audit position regarding the retention of a bond administrative fee. IC 35-33-8-3.2 states in part regarding surety bonds, cash and security deposits, real estate bonds or any combination of these posted for bail: “…A portion of the deposit, not to exceed ten percent (10%) of the monetary value of the deposit or fifty dollars ($50), whichever is the lesser amount, may be retained as an administrative fee. The clerk shall also retain from the deposit under this subdivision fines, costs, fees, and restitution as ordered by the court, publicly paid costs of representation that shall be disposed of in accordance with subsection (b), and the fee required by subsection (d). In the event of the posting of a real estate bond, the bond shall be used only to insure the presence of the defendant at any stage of the legal proceedings, but shall not be foreclosed for the payment of fines, costs, fees, or restitution. The individual posting bail for the defendant or the defendant admitted to bail under this subdivision must be notified by the sheriff, court, or clerk that the defendant’s deposit may be forfeited under section 7 of this chapter or retained under subsection (b)….”

The Attorney General has clarified to us by advisory letter that conviction is not required in order to retain the administrative fee. After disposition of the charges, whether by dismissal, acquittal, or conviction, the clerk must return to the defendant only the amount not retained. Therefore, during an audit of the county, we will be following this guidance. Conviction will not be considered a requirement to retain the bond administrative fee from a bail bond that is not a real estate bond.

PREMIUM AND ACCRUED INTEREST ON BONDS ISSUED AND SOLDIC 5-1-12-2 requires that:

"Whenever any bonds are sold by any municipal corporation and when the successful bidder agrees to pay and does pay any premium as a part of the bid price of such bonds, any and all premiums so received shall be paid into and shall constitute a part of the fund which is created to retire such bonds and to pay the interest thereon"

In the sale of bonds "accrued interest" is the interest on the obligations from the date of the bonds to date of their delivery to the purchaser. Interest coupons attached to bonds are for exact sums of money which the issuing authority is required to pay, but between the date of bonds and date of delivery and receiving payment of the bid price, no interest is actually earned. The so-called accrued interest is simply a reimbursement to the municipal corporation for the unearned part of the interest the municipal corporation will be required to pay pursuant its interest coupons.

Accrued interest also must be receipted to the bond fund so that same may be used in retiring the bonds and interest. Only the principal sum of the bonds can be placed in the fund to carry out the project for which the bonds were issued.

IC 20-42-2-11 and 20-42-2-12 contain authority for counties to borrow from the Congressional School Fund. Any such loans must be authorized by an ordinance of the county council.

Some of the statutes which authorize other means of borrowing are:

IC 36-2-6-18 through 36-2-6-20 Temporary Loans, Bonds and Tax Anticipation Warrants

IC 5-19-1.5 Grant Anticipation Notes

IC 36-1-8-4 Temporary Loans Between Funds

PAID BREAKS FOR EXPRESSING MILK

IC 5-10-6-2 states: " (a) The state and political subdivisions of the state shall provide reasonable paid break time each day to an employee who needs to express breast milk for the employee’s infant child. The break time must, if possible, run concurrently with any break time already provided to the employee. The state and political subdivisions are not required to provide break time under this section if providing break time would unduly disrupt the operations of the state or political subdivisions.

(b) The state and political subdivisions of the state shall make reasonable efforts to provide a room or other location, other than a toilet stall, in close proximity to the work area, where an employee described in subsection (a) can express the employee’s breast milk in privacy. The state and political subdivisions shall make reasonable efforts to provide a refrigerator or other cold storage space for keeping milk that has been expressed. The state or a political subdivision is not liable if the state or political subdivision makes a reasonable effort to comply with this subsection.”

Plans and specifications for the construction of bridges are not required to be approved by the state highway commission unless Federal funds, disbursed by the state highway commission, are used in the construction of the bridge. The highway commission will render assistance to the county highway department when such assistance is requested, whether or not Federal funds are used.

Construction of bridges may be financed in four manners, funds arising from a separate source for each:

1. County General Fund – IC 8-16-5-3; 36-2-5-7

2. Cumulative Bridge Fund – IC 8-16-3-1

3. Major Bridge Fund – IC 8-16-3.1

4. County Cumulative Capital Development Fund – IC 36-9-14.5According to IC 10-17-10-1, the board of county commissioners may allow for the claim of a burial allowance not to exceed one thousand dollars ($1,000) in an amount set by ordinance for the burial of an individual who:

"….(A) has served as a member of the armed forces of the United States as a soldier, sailor, or marine in the army, air force, or navy of the United States or as a member of the women's components of the army, air force, or navy of the United States, is a resident of Indiana, and dies while a member of the armed forces and before discharge from the armed forces or after receiving an honorable discharge from the armed forces; or

(B) is the spouse or surviving spouse of a person described in clause (A) and is a resident of Indiana…"

The claim must be filed by an interested person with the board of county commissioners of the county of residence of the deceased person and state certain facts; such as, the military service rendered, date of death, and date of discharge (if discharged from service before death), and that the deceased has been buried in a decent and respectable manner in a cemetery or burial ground.

- C

Capital Assets

Establishing the Estimated Cost

CemeteriesSmaller Purchases Not Capitalized

Child Support Program

Claims

Officials' Signatures on Claims, Warrants, and Other Official Documents

Commisary Fund

Community Corrections Programs

Compensation

Changing Compensation of County Officers and Employees

Employee Employed in More Than One Position

Fair Labor Standards Act - Compensatory Time

County Auditor

Clerk of County Board of Commissioners

County Commissioners

County Coroner

Training and Continuing Education Fee

County Council

County Economic Development Income Tax (CEDIT) - Capital Improvement Fund

County Elected Officials Training Fund

County Extradition and Sheriff Assistance Fund

County Law Enforcement Continuing Education Fund

Claims by State Police and DNR

Courts

Calculation of Interest on Judgments

Clerk of the Circuit Court

Bank/Credit Card Payments to the County Courts

Clerk's Record Perpetuation Fund

Use of Record Perpetuation Funds

Judgments Collected on Overweight Vehicles

Court Reporters - Transcript Preparation

Support Order - Residence Change

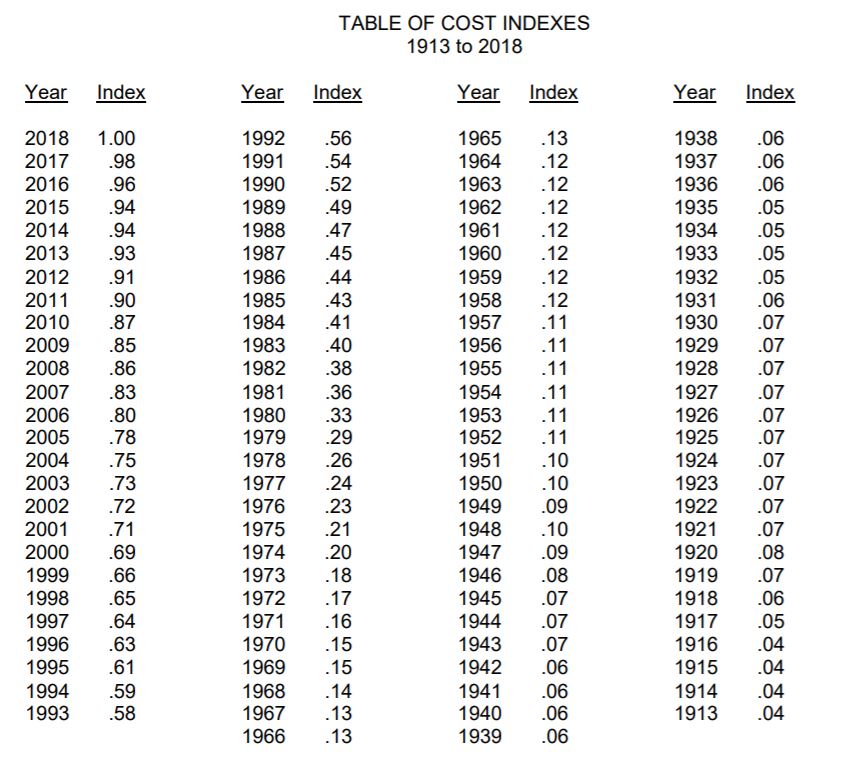

ESTABLISHING THE ESTIMATED COST OF CAPITAL ASSETS

When it is not possible to determine the historical cost of capital assets owned by a governmental unit, the following procedure should be followed.

Develop an inventory of all capital assets which are significant for which records of the historical costs are not available. Obtain an estimate of the replacement costs of these assets. Through inquiry determine the year or approximate year of acquisition. Then multiply the estimate replacement cost by the factor for the year of acquisition from the Table of Cost Indexes. The resulting amount will be the estimated cost of the asset.

In some cases estimated replacement cost can be obtained from insurance policies; however, if estimated replacement costs are not available from insurance policies, you should obtain or make an estimate of the replacement costs.

If the replacement cost is estimated to be $76,000.00 and the asset was constructed about 1930, then the estimated cost of the asset should be reported as $6,840.00.

$76,000.00 X .07 = $5,320.00

CAPITAL ASSETS – CEMETERIES

County Owned Cemeteries are considered capital assets and need to be properly recorded on General Form 369 – Capital Assets Ledger. The cemeteries are to be reported on General Form 369 – Capital Assets Ledger at the actual or estimated historical cost based on appraisals or deflated current replacement cost. Contributed or donated assets are reported at estimated fair value at the time received. General Form 369 – Capital Assets Ledger does not have a separate classification for cemeteries, so the cemetery ground will be recorded on the capital asset ledger under land, any structures on the cemetery grounds under buildings, and roads and drainage systems will be recorded under infrastructure. There will be no effect on the value of the asset as plots are sold. The purchase of a burial plot is a real estate transaction; however, cemetery plot deeds grant burial rights that create an easement for the specific purpose of burial but do not alter the County’s ownership of the cemetery as a whole.

Each county is required to adopt a capital asset policy that details the threshold at which an item is considered a capital asset. A complete physical inventory must be taken at least every two years, unless more stringent requirements exist, to verify account balances carried in the accounting records.CAPITAL ASSETS – SMALLER PURCHASES NOT CAPITALIZED

Assets include any items that are purchased by the County that will be useful for more than one year. This can include items such as office equipment and furniture as examples. Each County should have a capitalization policy that sets a threshold at which these assets are capitalized and added to the capital asset detail. The threshold amount is a county decision. As an example, if the threshold is set for $5,000 than any asset purchased that costs more than $5,000 is added to the capital asset detail. If the asset costs less than $5,000, it is not capitalized.It is the responsibility of the county to safeguard all assets purchased, even those that are not capitalized. Some purchases, such as electronic equipment (laptops, tablets, cell phones, PC’s etc.) may be at higher risk of loss due to theft or misuse, but still cost less than the capitalization threshold. For those items, the County should have an inventory policy to provide control over those items. This policy could be part of the capitalization policy or a separate policy. The inventory policy would allow the county to track and account for these assets that are not capitalized but still need to be monitored.

You do need to have control procedures in place to safeguard these items. We used electronic items as an example, but there are other items that should also be considered such as copiers, generators, radios and tools. Your policy needs to consider what items are worth the cost of tracking and which are not, for example, a laptop is worth tracking, while a chair may not be. The policy could establish a threshold similar to the capital asset threshold for a dollar amount that would be tracked. Alternatively, the policy could specify particular types of equipment that should be tracked. The County would need to decide based on the risks and resources of the County. The policy should also specify who will do the tracking, for example, in many counties, the IT departments often track all of the electronic equipment. For other items, the Department heads might keep a departmental inventory.

Some additional items to consider:

1. A way to track these items (serial numbers, stickers or other tagging, for example)

2. A complete inventory of these items (using serial numbers, tag numbers, locations) this could be done manually or with a spreadsheet or data base.

3. A physical inventory should be conducted periodically by departments to determine the accuracy of the inventory.

4. Policies and procedures for adding new purchases and removing the items when they are no longer owned by the County.

5. Policies and procedures for missing items.IC 36-1-8-2 states:

“(a) The fiscal body of a political subdivision may permit any of its officers or employees having a duty to collect cash revenues to establish a cash change fund. Such a fund must be established by a warrant drawn on the appropriate fund of the political subdivision in favor of the officer or employee, in an amount determined by the fiscal body without need for appropriation to be made for it.

(b) The officer or employee who establishes a cash change fund shall convert the warrant to cash, shall use it to make change when collecting cash revenues, and shall account for it in the same manner as is required for other funds of the political subdivision.

(c) The fiscal body shall require the entire cash change fund to be returned to the appropriate fund whenever there is a change of the custodian of the fund or if the fund is no longer needed.”

A claim should be filed by the officer or employee designated by the fiscal body. The claim should contain a statement regarding the necessity for such fund together with the statutory reference (IC 36-1-8-2) authorizing its establishment. We do caution officials the amount advanced should not be greater than seems reasonably needed by the officer or employee.

Affected Cemeteries

IC 23-14-67 applies to cemeteries that:

(1) are without funds or sources of funds for reasonable maintenance;

(2) have suffered neglect and deterioration;

(3) may be the burial grounds for Indiana pioneer leaders as well as for veterans of every American war including the Revolutionary War; and

(4) either:

(A) was established before 1875; or

(B) is a burial ground for a veteran of the Civil War.

Appointment and Term of Commission

The board of commissioners of a county may appoint a county cemetery commission of five (5) county residents. County cemetery commission members shall be appointed for a term of five (5) years, staggered by the board of county commissioners to permit an appointment or a reappointment of one (1) commissioner member per year. (IC 23-14-67-2)

Annual Tax Levy and Budget

The commission may request the levy of an annual tax not exceeding fifty cents ($.50) on each one hundred dollars ($100) of assessed valuation of property in the county for the purpose of restoring and maintaining the cemeteries described above. (IC 23-14-67-3)

The county cemetery commission shall present an annual plan and budget to the board of county commissioners and the county council for approval and shall make an annual report to those bodies and the Indiana Historical Bureau. (IC 23-14-67-4) (IC 23-14-67-3.5)

Trusts for Cemetery Associations

IC 23-14-70 authorizes the following:

The board of commissioners of a county may receive from or on behalf of any cemetery corporation, church, association, or organization that has been dissolved or is to be dissolved a deposit of money to be held in trust under terms that are designated in writing. The interest on the money shall be used to keep in good condition any abandoned cemetery, public incorporated cemetery, or lots, monuments, mausoleums, vaults, or other burial structures in any cemetery. The board of commissioners may not expend more for this purpose than the interest earned from the loan or investment of the funds. (IC 23-14-70-1)

All money received by the board of commissioners may be invested in compliance with IC 20-42-1-14. (IC 23-14-70-2)

The county auditor shall make distribution of the interest earned on any cemetery fund or funds on the last Monday of January of each year and to the following person or persons:

(1) To the trustee of the township in which an abandoned or unincorporated cemetery is located.

(2) To the trustee of the township lying on the east or south of the cemetery if the cemetery is located on a county boundary or on a township boundary.

(3) To the treasurer of the board of directors of an incorporated cemetery. (IC 23-14-70-3)

The township trustee or the treasurer of the board of directors shall each make a receipt or voucher for any money paid out, stating the amount paid out, the purpose for which it was expended, and the fund from which it came. The receipts and vouchers shall be filed with county auditor before January 2 each year and shall be presented to the board of commissioners for examination and approval at its January meeting. (IC 23-14-70-4)

The auditor is liable on his bond for any neglect or failure of duty with respect to this fund in the same manner as with respect to the school fund. The county is also liable for the preservation of the principal and the payment of the interest on the fund to the same extent that it is liable with respect to the principal and interest of the school fund. (IC 23-14-70-5)

If a cemetery is under the control of a duly organized board of directors of an incorporated cemetery or the trustees or officers of the church, association, or other organization, the board of county commissioners may, on its own initiative or upon request of the proper officers of the cemetery, pay over or return to the treasurer of the cemetery any money deposited with the county, to be held and managed by the corporation, church, association, or organization in compliance with the terms of the bequest, legacy, or endowment and applicable statutes. (IC 23-14-70-6)

COUNTY UNIFORM CHART OF ACCOUNTS

All counties must implement the use of the new chart of accounts by January 1, 2012. Although the transition may be tedious we are confident the use of a standard chart of accounts will ultimately help with training and reporting of financial information. The chart of accounts, instructions, and other tools for using the uniform chart of accounts are on the State Board of Accounts website at www.IN.gov/sboa/. Look in “Counties” under the topic “Political Subdivisions” and choose the County Auditor link under County Offices. On the County Auditor page, navigate to Overview and Chart of Accounts.

CHILD SUPPORT PROGRAM - ARRA INCENTIVE FUNDS

Indiana counties receive Title IVD incentive funds for participating in the child support enforcement program. The incentive funds are paid to the Prosecutors, Clerk and County. Currently there are six incentive funds being used to account for these funds. Three for regular incentive funds and three for ARRA incentive funds. ARRA funds are no longer being distributed. Counties were encouraged to pay any expenses from the ARRA Incentive funds first so that the funds could be closed out. However, there is still approximately $500,000 in ARRA money remaining in these funds in Indiana. ARRA funds were required to be maintained separately so that they could be reported on ARRA reports.

These accounts on the funds ledger are Prosecutor IV-D ARRA Fund, Clerk IV-D ARRA Fund, and County IV-D ARRA Fund. ARRA funds are treated exactly the same as the regular funds as far as who can use them and how they can be spent. The Department of Health and Human Services (HHS) has provided direction to the Indiana Child Support Bureau (CSB) that oversees the Title IVD program in Indiana, that there is no longer a need to report the ARRA funds separately from the regular incentive funds. HHS has given their approval for the counties to combine the ARRA balances with their corresponding regular incentive funds. The CSB is providing guidance to the County Auditors to transfer the ARRA balance into the respective Incentive fund. The balance in the Prosecutor IV-D ARRA will be transferred to Prosecutor IV-D Incentive fund as will the Clerk IV-D ARRA to Clerk IV-D Incentive and County IV-D ARRA to County IV-D Incentive.

The CSB has directed a check be written from the ARRA funds to the regular incentive funds in order to provide adequate supporting documentation of the transfer.

The CSB will send partially completed Incentive Transfer Forms to Auditors. Auditors are to include dollar amounts and transfer dates. The form is only signed by the Auditor for these ARRA transfers.

Officials have been warned not to close out ARRA funds yet until a revised form is approved. CSB must receive transfer forms and the Quarterly Incentive Balance (QIB) Report with adjustments before 12-31-18 to close out for 2019. If the transfers occur in 2019, then close accounts by the end of year for 2020. The transfer agreement, including ledgers and fund balances, are to be uploaded with the QIB.

IC 33-37-7-6 requires that three percent (3%) of all court costs collected by the Clerk of the Circuit Court to be set aside by the County Auditor in a City and Town Court Cost Fund. Such funds shall be distributed semiannually to each city and town in the county that maintains a law enforcement agency and prosecutes at least fifty percent (50%) of its ordinance violations in a circuit, superior, or county court in the county. If a city or town located in Marion County prosecutes its ordinance violations in a municipal court, then that city or town would qualify for such distribution.

The county auditor shall determine the amount to be distributed to each city and town qualified as follows:

STEP ONE: Determine the population of the qualified city or town.

STEP TWO: Add the populations of all qualified cities and towns determined under STEP ONE.

STEP THREE: Divide the population of each qualified city and town by the sum determined under STEP TWO.

STEP FOUR: Multiply the result determined under STEP THREE for each qualified city and town by the amount of the qualified municipality share.

The county auditor shall semiannually (in June and December) distribute to each qualified city and town the amount computed for that city or town under STEP FOUR.

If no city or town qualifies for a semiannual distribution, the monies shall remain in the city and town court cost fund for future distribution, it is not to be transferred to the County General Fund.

Each city and town that qualifies is encouraged to contact the County Auditor in their county each May and November about the distribution.

Several questions concerning the distribution of the City and Town Court Cost Fund by the County Auditor have been asked by city, town and county officials. The questions, along with our audit positions, are as follows:

Question #1 What must a municipality do to qualify for a share of the City and Town Court Cost Fund?

Answer #1 A municipality must maintain a law enforcement agency and prosecute at least fifty percent (50%) of its ordinance violations in a Circuit, Superior, or County Court located in the county. The County Auditor shall determine the amount to be distributed to each qualified city and town. (IC 33-37-7-6)

Question #2 Does a city ordinance violation filed in County Court qualify the city to receive such funds even if the case is dismissed by the city?

Answer #2 No. The city must prosecute the case in order to qualify.

Question #3 In which semiannual period does the city or town receive a share of such funds assuming only one (1) case is filed? Is it the period in which the case was filed or is it the period in which it was prosecuted?

Answer #3 The period in which the case was prosecuted would govern the period of distribution. Distributions are to be made semiannually (June and December) for the previous six (6) months collections.

Question #4 Can a city or a town with an Ordinance Violations Bureau qualify for the distribution?

Answer #4 Yes. IC 33-36-3-6(b) states that ordinances processed through an Ordinance Violations Bureau are not to be considered in determining whether the unit prosecuted at least fifty percent (50%) of its ordinance violations in a Circuit, Superior, or County Court.

Question #5 To what fund does a city/town receipt the distributions?

Answer #5 Distributions should be receipted to the General Fund.

OFFICIALS’ SIGNATURES ON CLAIMS, WARRANTS, AND OTHER OFFICIAL DOCUMENTS

The State Board of Accounts is often asked to approve the use of rubber stamps or other devices for affixing facsimile signatures of public officials on claims, warrants, and other official documents. The decision as to whether or not the number of documents to be signed justifies the use of a rubber stamp or other device for affixing his/her signature must be made by each official. Since each official is responsible for his/her signature, a rubber stamp or other signing device should be used only under the closest direction of the official and must be properly safeguarded when not in use.

SEMIANNUAL REPORTS OF THE COMMISSARY FUND - SHERIFF

The sheriff is to provide a copy of the commissary fund’s receipts and disbursements to the county council. The semiannual reports are due on July 1 and December 31 of each year. The SBOA has prescribed Form 205, Ledger of Receipts, Disbursements and Balances for the Commissary fund, for use as a semiannual report. The County always has the option to choose an alternative form and have that form (or report) approved as part of the audit process

COMMUNITY CORRECTIONS PROGRAMS

Indiana Department of Corrections (IDOC) provides grant funding to the counties. Historically that has been for one project, the county’s Community Corrections program. The grant was deposited to a grant fund and the Program Income was deposited to a separate fund. With recent legislation, the grant funding has been expanded to include other programs and this has further complicated the accounting for these grants.

The Auditor is the fiscal officer for the grant. The Auditor must have sufficient information on the grant and the grant budget to be able to audit the claims and post receipts to the correct funds. Starting with the 2016-2017 grants, the grant agreement and attachments that contain the approved budgets for the grants are sent to the County Auditors for signature. A copy of these grant documents should be made by the auditor’s office to keep in the grant file. There are two main sources of funding for the Community Corrections which comprise the grant distributions sent from the state each month and project income. The county may also appropriate money the general fund to support the Community Corrections programs.Originally, the Community Corrections was one grant and the collection of user fees related to the Community Corrections program was posted to a separate project income fund (Fund 1122 in the Uniform Chart of Accounts). With the expansion of the grant funding in recent legislation and starting with the 2016-2017 fiscal year, the Community Corrections grant can be awarded to Probation Departments, Prosecutor Diversion Programs and Court Recidivism Programs. In addition, the Community Corrections program for juveniles is now tracked separately from the Community Corrections program for adults. In theory, a county could be awarded as many as five projects from the Community Corrections grant funding. Each project needs to have its own separate grant fund within the fund numbers assigned to State and Local Grants (9000 series in the Uniform Chart of Accounts). At the end of the grant year, the IDOC will evaluate and audit the ending fund balance in the grant funds and determine if the balance is to be returned to the state or may be carried over to a new grant year.

Community Corrections grants are advance grants. IDOC will send out 25% of the total award in the first month of the fiscal year (July). The remaining 75% of the grant is divided over 12 months and 1/12th is sent out each month, also starting with July. The grant agreement will specify how the total grant is to be divided among the approved projects. The payments will be made by EFT and there will be one payment amount each month. Using the grant agreement information, the auditor will have to determine what percentage of the total payment to allocate to each project. The July payment will include the 25% advance and the 1/12th payment for July. Starting with the August payment, the payment amounts should remain consistent and the allocation should remain the same each month. The grant agreement will have attachments that contain the approved budgets for each project. By statute, the council must also approve the appropriations.

For the Community Corrections projects, the Community Corrections Advisory Board will set user fees for participation in the program. Community Corrections personnel collect these fees and the fees would be posted to a project income fund. (Fund 1122). Prior to the 2016-2017 year, both adult and juvenile community corrections were placed in the Community Corrections fund. Now, however IDOC is tracking juvenile programs separately from adult programs and there would need to be a separate project income fund for juvenile program fees if your county has a juvenile community corrections program. The program may also collect user fees that offset the cost of certain services provided to participants, such as educational classes, treatment or drug testing. These fees would also be deposited into the project income fund.

For Probation and Pretrial Diversion programs, user fees for participation in the programs are established by statute. For Court Recidivism (Problem Solving Courts) the court establishes the user fees for participation. In each of these three programs, statute directs these user fees to be deposited into specific funds, such as adult and juvenile supplemental probation funds and appropriate user fee funds for the court. The auditor will continue to post those fees as they have always been posted, and that will not change due to a grant from Community Corrections awarded to those offices. However, if the community correction grant received by one of these offices pays for an educational class, drug testing or treatment and a fee is charged the participants to reimburse the costs of these programs, those user fees would have to be deposited into a separate project income fund for that offices. If the grant does not pay any of these costs, the user fees collected would be posted to the appropriate user fee fund. It becomes extremely important that the project leaders for each office provide sufficient information to allow the receipts to be posted to the correct fund. The only way for the auditor’s office to know how to deposit these collections is for the project directors to provide a report of collections that details how this money is to be posted.

Any balance in a project income fund would remain at the county at the end of each fiscal year. In order to disburse Community Corrections project income funds, the disbursement must be in compliance with the approved budget for the project income. These budgets would be included in the attachments with the grant budgets. Any changes to the approved budgets would need to be approved by IDOC and the project leader should be able to provide documentation of that approval.Employees of a Community Corrections program are to be considered County employees. All claims are to be submitted to the Board of County Commissioners for approval before payment.

COMPENSATION – ANNUAL SALARIES – PROPER PAYMENTS

Indiana statutes require salary ordinances to be enacted annually for all elected and appointed county officials and employees. Historically, even dollar amounts such as $20,000 are set as an annual salary for an employee. With a bi-weekly payroll period established for the unit, it becomes difficult to pay an employee the exact amount of his/her annual salary since twenty-six payrolls (in some years there are twenty-seven) will not divide evenly. Unless an odd amount is paid for the last payroll period, the employee is either over or under paid the amount established in the salary ordinance causing either an unhappy employee or an unhappy local fiscal officer.

It is suggested for salary ordinances enacted in 2003 and all future periods, the employee salaries be established to coincide with the customary work and pay period. (For example, instead of $20,000 annually, adopt $385.00 weekly or $770.00 bi-weekly.) By using this method it will make no difference if there are 52 or 53 weekly pays or 26 or 27 bi-weekly pays.

When using this suggestion and preparing your budget, it will be imperative the proper number of pays be computed in order to not under-estimate the next year’s requirements for personal services and associated fringe benefits. Keep in mind that the salary ordinance and the budget ordinance are two different statutory requirements. You should not attempt to combine the ordinances.

CHANGING COMPENSATION OF COUNTY OFFICERS & EMPLOYEES

The compensation of an elected county officer may not be changed in the year for which it is fixed, unless it is changed for a newly elected officer. IC 36-2-5-13(b) provides the process to change a newly elected officer’s compensation. Otherwise, an elected officer’s compensation may be changed if the amended salary ordinance is enacted in the year PRECEDING the year that salary payment is made.

The compensation of the other county officers who are not elected, deputies, and employees or the number of each may be changed at any time upon proper application and a majority vote of the county fiscal body [IC 36-2-5-13(a)].

EMPLOYEE EMPLOYED IN MORE THAN ONE POSITION

IC 5-11-9-4 requires that records be maintained showing which hours are worked each day for employees employed by more than one political subdivision or in more than one position by the same public agency. We have been asked if for those working in two different positions for the same unit if prescribed form 99A, The Employee Service Record, is sufficient and if one or two service records must be maintained. While form 99A shows the number of hours worked, it does not show which hours were worked in each position. For this reason we require a log be maintained that reflects which hours are worked. If an employee is working in two different positions in the same unit we will not take exception to one form 99A being maintained but a log must also be maintained to reflect which hours were worked in each position.

COMPENSATORY TIME – FAIR LABOR STANDARDS ACTThe following article was contributed by the Indianapolis Office of the Wage and Hour Division of the United States Department of Labor.

Use of Compensatory Time Off Under the Fair Labor Standards Act

The Fair Labor Standards Act (FLSA) is a federal law that sets standards for minimum wage, overtime, and child labor. Under Sec. 7(o), public sector employers may provide compensatory time off in lieu of monetary overtime compensation. The compensatory time off must be at the rate of not less than 1 and ½ hours for each overtime hour worked.

As a condition for use of compensatory time off in lieu of overtime payment in cash, an agreement of understanding must be reached prior to performance of the work. Such an agreement may involve a collective bargaining agreement, a memorandum of understanding, or any other type of agreement between the public agency and the employees’ representative. (If the employees do not have representative, then the agreement must be between the public agency and the individual employee.) The agreement may contain provisions that address the preservation, use, or cashing out of compensatory time, as long as they are consistent with Sec. 7(o).

As an example, if an agreement specifically provides that an employee must use accrued compensatory time prior to the use of vacation leave, then this policy would be within the FLSA, assuming that employees have knowingly and voluntarily agreed to such a provision freely and without coercion or pressure. On the other hand, if the compensatory agreement did not specifically address that issue, then the employer could not require an employee to take their accrued compensatory time prior to vacation leave.

Here’s a different type of example: An agreement states that requests for compensatory time off have to be submitted with adequate advance notice and that management will approve them based on scheduling needs, allowing only one employee off per shift. Sec 7(o)(5) of FSLA says that requests for use of compensatory time off will be permitted within a “reasonable period”, if such use does not “unduly disrupt” the operations of the agency. In this example, the agreement would be inconsistent with the FLSA since it would allow for the denial of a request for reasons other than unduly disrupting the operations of the agency.