TITLE 329 SOLID WASTE MANAGEMENT BOARD

Final Rule

LSA Document #05-167(F)

DIGEST

First Notice of Comment Period: July 1, 2005, Indiana Register (28 IR 3060).

Continuation of First Notice of Comment Period: January 1, 2006, Indiana Register (29 IR 1393).

Second Notice of Comment Period: April 1, 2006, Indiana Register (29 IR 2380).

First Hearing Notice: April 1, 2006, Indiana Register (29 IR 2391).

Date of First Hearing: July 18, 2006, continued to September 19, 2006.

Date of Second Hearing: January 16, 2007.

Authority: IC 13-14-8-7; IC 13-15; IC 13-19-3

Sec. 24. (a) The owner, operator, or permittee of an MSWLF shall maintain the series of identifiable boundary markers required under 329 IAC 10-19-1(a)(2)(B) to delineate the approved solid waste land disposal facility boundary and approved solid waste boundaries for the life of the MSWLF. (b) The owner, operator, or permittee shall maintain the on-site benchmarks required under 329 IAC 10-19-1(a)(2)(c) so that no portion of the proposed solid waste disposal area is further than one thousand (1,000) feet from a benchmark unless a greater distance is:

(1) necessary to avoid the placement of benchmarks on filled areas; and is

(2) approved by the commissioner.

(c) The owner, operator, or permittee shall conduct an annual survey between October December 1 and December March 31 of each year for the purpose of establishing a contour map that indicates existing contours of the MSWLF and the existing limits of solid waste disposed at the MSWLF. The contour map must be done at the same scale as the final contour map required under 329 IAC 10-15-2. The contour map must:

(1) indicate the day the survey was conducted; and must

(2) be submitted to the department by February June 15 of the year following the survey in a paper copy form.

(d) The owner, operator, or permittee of a currently permitted MSWLF shall submit a present contour map and a proposed final contour map on paper copy form as required by 329 IAC 10-15-2(b). In addition to the paper copy forms, a copy may also be submitted electronically. No subsequent annual submissions of the final contour map will be necessary unless there is a change to the approved final contours.

329 IAC 10-39-2 Closure; financial responsibility

Authority: IC 13-14-8-7; IC 13-15; IC 13-19-3

Sec. 2. (a) The permittee shall establish financial responsibility for closure of all the permitted acreage for the solid waste land disposal facility before waste placement, except as provided in subsection (b). The permittee shall choose from the following options:

(1) The trust fund option, including the following:

(A) The permittee may satisfy the requirements of this section by establishing a trust agreement on:

(i) forms provided by the commissioner; or on such

(ii) other form as forms approved by the commissioner.

(B) All trust agreements must contain the following:

(i) Identification of solid waste land disposal facilities and corresponding closure cost estimates covered by the trust agreement.

(ii) The establishment of a trust fund in the amount determined by subsection (b) and guarantee payments from that fund either:

(AA) reimbursing the permittee for commissioner-approved closure work done; or

(BB) making payments to the commissioner for accomplishing required closure work.

(iii) The requirement of annual evaluations of the trust to be submitted to the commissioner.

(iv) The requirement of successor trustees to notify the commissioner, in writing, of their appointment at least ten (10) days prior to before the appointment becoming effective.

(v) The requirement of the trustee to notify the commissioner, in writing, of the failure of the permittee to make a required payment into the fund.

(vi) The establishment that the trust is irrevocable unless terminated, in writing, with the approval of the:

(AA) permittee; the

(BB) trustee; and the

(CC) commissioner.

(vii) A certification that the signatory of the trust agreement for the permittee was duly authorized to bind the permittee.

(viii) A notarization of all signatures by a notary public commissioned to be a notary public in the state of Indiana at the time of notarization.

(ix) The establishment that the trustee is:

(AA) authorized to act as a trustee; and is

(BB) an entity whose operations are regulated and examined by a federal and state of Indiana agency.

(x) The requirement of:

(AA) initial payment into the fund be made within thirty (30) days of the commissioner's approval of the trust agreement; and

(BB) any subsequent payments be made within thirty (30) days of each anniversary of the initial payment. annually not later than June 15.

(2) The surety bond option, including the following:

(A) The permittee may satisfy the requirements of this section by establishing a surety bond on:

(i) forms provided by the commissioner; or on such

(ii) other forms as approved by the commissioner.

(B) All surety bonds must contain the following:

(i) The establishment of penal sums in the amount determined by subsection (b).

(ii) Provision that the surety:

(AA) will be liable to fulfill the permittee's closure obligations upon notice from the commissioner that the permittee has failed to do so; and

(iii) Provision that the surety (BB) may not cancel the bond without first sending notice of cancellation by certified mail to the permittee and the commissioner at least one hundred twenty (120) days prior to before the effective date of the cancellation.

(iv) (iii) Provision that the permittee may not terminate the bond without prior written authorization by the commissioner.

(C) The permittee shall establish a standby trust fund to be utilized in the event the:

(i) permittee fails to fulfill closure obligations; and the

(ii) bond guarantee is exercised. Such

The trust fund must be established in accordance with the requirements of subdivision (1).

(D) The surety company issuing the bond must be:

(i) among those listed as acceptable sureties for federal bonds in Circular 570 of the United States Department of the Treasury; and must be

(ii) authorized to do business in Indiana.

(E) The surety will not be liable for deficiencies in the performance of closure by the permittee after the commissioner releases the permittee in accordance with section 6 of this rule.

(3) The letter of credit option, including the following:

(A) The permittee may satisfy the requirements of this section by establishing a letter of credit on:

(i) forms provided by the commissioner; or on such

(ii) other forms as approved by the commissioner.

(B) All letters of credit must contain the following:

(i) The establishment of credit in the amount determined by subsection (b).

(ii) Irrevocability.

(iii) An effective period of at least one (1) year and automatic extensions for periods of at least one (1) year unless the issuing institution provides written notification of cancellation by certified mail to both the permittee and the commissioner at least one hundred twenty (120) days prior to before the effective date of cancellation.

(iv) Provision that, upon written notice from the commissioner, the institution issuing the letter of credit will:

(AA) state that the permittee's obligations have not been fulfilled; and the institution will

(BB) deposit funds equal to the amount of the letter of credit into a trust fund to be used to ensure the permittee's closure obligations are fulfilled.

(C) The permittee shall establish a standby trust fund to be utilized in the event the:

(i) permittee fails to fulfill its closure obligations; and the

(ii) letter of credit is utilized. Such

The trust funds must be established in accordance with the requirements of subdivision (1).

(D) The issuing institution must be an entity:

(i) that has the authority to issue letters of credit; and

(ii) whose letters of credit operations are regulated and examined by a federal or Indiana agency.

(4) The insurance option, including the following:

(A) The permittee may satisfy the requirements of this section by providing evidence of insurance on:

(i) forms provided by the commissioner; or on such

(ii) other forms as approved by the commissioner.

(B) All insurance must include the following requirements:

(i) Be in the amount determined by subsection (b).

(ii) Provide that, upon written notification to the insurer by the commissioner that the permittee has failed to perform final closure, the insurer shall make payments:

(AA) in any amount, not to exceed the amount insured; and

(BB) to any person authorized by the commissioner.

(iii) Provide that the permittee shall maintain the policy in full force and effect unless the commissioner consents in writing to termination of the policy.

(iv) Provide for assignment of the policy to a transferee permittee.

(v) Provide that the insurer may not cancel, terminate, or fail to renew the policy except for failure of the permittee to pay the premium. No policy may:

(AA) be canceled;

(BB) be terminated; or

(CC) fail to be renewed;

unless at least one hundred twenty (120) days prior to such before the event the commissioner and the permittee are notified by the insurer in writing.

(C) The insurer shall either be:

(i) licensed to transact the business of insurance; or be

(ii) eligible to provide insurance as an excess or surplus lines insurer;

in one (1) or more states.

(5) The financial test for restricted waste sites option, including the following:

(A) This financial test is only available for restricted waste sites.

(B) If a permittee meets the criteria set forth in item (I) and either item (ii) or (iii), the permittee shall be deemed to have established financial responsibility as follows:

(i) Less than fifty percent (50%) of the company's gross revenues are derived from waste management.

(ii) The permittee meets the following four (4) tests:

(AA) Two (2) of the following three (3) ratios are met:

(aa) A ratio of total liabilities to net worth less than two (2.0).

(bb) A ratio of the sum of net income plus depreciation, depletion, and amortization to total liabilities greater than one-tenth (0.1).

(cc) A ratio of current assets to current liabilities greater than one and one-half (1.5).

(BB) Net working capital and tangible net worth each at least six (6) times the sum of the current closure and current post-closure cost estimates.

(CC) Tangible net worth of at least ten million dollars ($10,000,000).

(DD) Assets in the United States amounting to at least ninety percent (90%) of the permittee's total assets or at least six (6) times the sum of the current closure and current post-closure costs estimates.

(iii) The permittee meets the following four (4) tests:

(AA) A current rating for the permittee's most recent bond issuance of AAA, AA, A, or BBB as issued by Standard and Poor's or Aaa, Aa, A, or Baa as issued by Moody's.

(BB) Tangible net worth of at least six (6) times the sum of the current closure and current post-closure cost estimates.

(CC) Tangible net worth of at least ten million dollars ($10,000,000).

(DD) Assets located in the United States amounting to at least ninety percent (90%) of the permittee's total assets or at least six (6) times the sum of the current closure and current post-closure estimates.

(C)To demonstrate the financial test has been met, the permittee shall submit the following documents to the commissioner:

(i) A form provided by the commissioner or such other form as approved by the commissioner, signed by the permittee's chief financial officer, demonstrating the applicable criteria have been met.

(ii) A copy of an independent certified public accountant's report examining the permittee's financial statements for the latest completed fiscal year.

(iii) A special report from the permittee's independent certified public accountant to the permittee stating the following:

(AA) The certified public accountant has compared the data that the letter from the chief financial officer specifies as having been derived from the independently audited, year-end financial statements for the latest fiscal year with the amounts in such the financial statements. and

(BB) In connection with that procedure, no matters come came to the attention of the certified public accountant that caused the certified public accountant to believe that the specified data should be adjusted.

(D) The permittee shall submit updated clause (C) documents to the commissioner within ninety (90) days after the close of each fiscal year.

(E) If at any time the permittee fails to meet the financial test, the permittee shall establish an alternate financial responsibility mechanism within one hundred twenty (120) days after the end of the fiscal year for which the year-end financial data shows that the permittee no longer meets the requirements.

(F) The commissioner may disallow use of this test on the basis of qualifications in the opinion expressed in the independent certified public accountant's report examining the permittee's financial statements. An adverse opinion or a disclaimer of opinion will be cause for disallowance. Other qualifications may be cause for disallowance if, in the opinion of the commissioner, they indicate the permittee does not meet the requirements of this subdivision. The permittee shall choose an alternate financial responsibility mechanism within thirty (30) days after notification of the disallowance.

(6) The local government financial test option, including the following:

(A) This financial test is only available for permittees that are local governments. As used in this subdivision, "local government" means a county, municipality, township, or solid waste management district.

(B) A local government permittee that satisfies the following requirements may demonstrate financial assurance up to the amount specified in clause (C):

(i) The local government permittee shall meet the following financial component requirements:

(AA) The local government permittee shall satisfy either of the following as applicable:

(aa) If the local government permittee has outstanding, rated general obligation bonds that are not secured by insurance, a letter of credit, or other collateral or guarantee, the local government permittee shall have a current rating of:

(1) Aaa, Aa, A, or Baa as issued by Moody's; or

(2) AAA, AA, A, or BBB as issued by Standard and Poor's;

on all such the general obligation bonds.

(bb) The local government permittee shall satisfy the following financial ratios based on the local government permittee's most recent audited annual financial statement:

(1) A ratio of cash plus marketable securities to total expenditures greater than or equal to five-hundredths (0.05).

(2) A ratio of annual debt service to total expenditures less than or equal to two-tenths (0.20).

(BB) The local government permittee shall:

(aa) prepare the local government permittee's financial statements in conformity with generally accepted accounting principles (GAAP) for governments; and

(bb) have the financial statements audited by an independent certified public accountant or the state board of accounts.

(CC) A local government permittee is not eligible to assure the local government permittee's obligations under this subdivision if any of the following applies to the local government permittee:

(aa) The local government permittee is currently in default on any outstanding general obligation bonds.

(bb) The local government permittee has any outstanding general obligation bonds rated lower than Baa as issued by Moody's or BBB as issued by Standard and Poor's.

(cc) The local government permittee has operated at a deficit equal to five percent (5%) or more of total annual revenue in each of the past two (2) fiscal years.

(dd) The local government permittee receives an adverse opinion, disclaimer of opinion, or other qualified opinion from the independent certified public accountant or the state board of accounts auditing its financial statement as required under subitem (BB). The commissioner may evaluate qualified opinions on a case-by-case basis and allow use of the financial test in cases where the commissioner deems the qualification insufficient to warrant disallowance of use of the test.

(DD) As used in this subdivision, the following terms apply:

(aa) "Cash plus marketable securities" means all the cash plus marketable securities held by the local government permittee on the last day of a fiscal year, excluding cash and marketable securities designated to satisfy past obligations, such as pensions.

(bb) "Debt service" means the amount of principal and interest due on a loan in a given time period, typically the current year.

(cc) "Deficit" means total annual revenues minus total annual expenditures.

(dd) "Total expenditures" means all expenditures, excluding capital outlays and debt repayment.

(ee) "Total revenues" means revenues from all taxes and fees but does not include the proceeds from borrowing or asset sales, excluding revenues from funds managed by the local government permittee on behalf of a specific third party.

(ii) The local government permittee shall meet the following public notice component requirements:

(AA) The local government permittee shall place a reference to the closure and post-closure care costs assured through the financial test into the local government permittee's next comprehensive annual financial report (CAFR) at the time of the next required local government financial test annual submittal or prior to before the initial receipt of waste at the facility, whichever is later. Disclosure must include the following:

(aa) Nature and source of closure and post-closure care requirements.

(bb) Reported liability at the balance sheet date.

(cc) Estimated total closure and post-closure care cost remaining to be recognized.

(dd) Percentage of landfill capacity used to date.

(ee) Estimated landfill life in years.

(BB) A reference to corrective action costs must be placed in the CAFR not later than one hundred twenty (120) days after the corrective action remedy has been selected in accordance with the requirements of 329 IAC 10-21-13. (CC) For the first year the financial test is used to assure costs at a particular facility, the reference may instead be placed in the facility's operating record until issuance of the next available CAFR if timing does not permit the reference to be incorporated into the most recently issued CAFR or budget.

(DD) For closure and post-closure costs, conformance with Government Accounting Standards Board Statement 18 assures compliance with this public notice component.

(iii) The local government permittee shall meet the following record keeping and reporting requirements:

(AA) The local government permittee shall place the following items in the facility's operating record:

(aa) A letter signed by the local government permittee's chief financial officer that completes the following:

(1) Lists all of the current cost estimates covered by a financial test as described in clause (C).

(2) Provides evidence and certifies that the local government permittee meets the conditions of item (i)(AA) (i)(BB), and through (i)(CC).

(3) Certifies that the local government permittee meets the conditions of item (ii) and clause (C).

(bb) The local government permittee's independently audited year-end financial statements for the latest fiscal year (except for local government permittees where audits are required every two (2) years when unaudited statements may be used in years when audits are not required), including the unqualified opinion of the auditor, who shall be an independent certified public accountant, or the state board of accounts that conducts equivalent comprehensive audits.

(cc) A report to the local government permittee from the local government permittee's independent certified public accountant or the state board of accounts based on performing an agreed upon procedures engagement relative to the:

(1) financial ratios required by item (i)(AA)(bb), if applicable; and

(2) requirements of item (i)(BB), (i)(CC)(cc), and (i)(CC)(dd).

The independent certified public accountant's or state board of accounts' report must state the procedures performed and the findings.

(dd) A copy of the CAFR used to comply with item (ii) or certification that the requirements of General Accounting Standards Board Statement 18 have been met.

(BB) The items required in subitem (AA) must be placed in the facility operating record as follows:

(aa) In the case of closure and post-closure care, either at the time of the next required local government financial test annual submittal or prior to before the initial receipt of waste at the facility, whichever is later.

(bb) In the case of corrective action, not later than one hundred twenty (120) days after the corrective action remedy is selected in accordance with the requirements of 329 IAC 10-21-13. (CC) After the initial placement of the items in the facility's operating record, the local government permittee shall:

(aa) update the information; and

(bb) place the updated information in the operating record;

within one hundred eighty (180) days following the close of the local government permittee's fiscal year.

(DD) The local government permittee is no longer required to meet the requirements of this item when either of the following occur: local government permittee:

(aa) The local government permittee substitutes alternate financial assurance as specified in this rule; or

(bb) The local government permittee is released from the requirements of this rule in accordance with section 6 or 11 of this rule.

(EE) A local government permittee shall satisfy the requirements of the financial test at the close of each fiscal year. If the local government permittee no longer meets the requirements of the local government financial test, the local government permittee shall, within one hundred twenty (120) days following the close of the local government permittee's fiscal year, complete the following:

(aa) Obtain alternative financial assurance that meets the requirements of this rule.

(bb) Place the required submissions for that assurance in the facility's operating record.

(cc) Notify the commissioner that the local government permittee no longer meets the criteria of the financial test and that alternate assurance has been obtained.

(FF) The commissioner, based on a reasonable belief that the local government permittee may no longer meet the requirements of the local government financial test, may require additional reports of financial condition from the local government permittee at any time. If the commissioner finds, on the basis of such the reports or other information, that the local government permittee no longer meets the requirements of the local government financial test, the local government permittee shall provide alternate financial assurance in accordance with this rule.

(GG) The commissioner may disallow use of this test on the basis of qualifications in the opinion expressed in the state board of accounts' annual financial audit of the local government permittee. An adverse opinion or a disclaimer of opinion is cause for disallowance. Other qualifications may be cause for disallowance if, in the opinion of the commissioner, the qualifications indicate the local government permittee does not meet the requirements of this subdivision. The local government permittee shall choose an alternate financial responsibility mechanism within ninety (90) days after notification of the disallowance.

(C) The local government permittee shall complete the calculation of costs to be assured. The portion of the closure, post-closure, and corrective action costs for which a local government permittee can assure under this subdivision is determined as follows:

(i) If the local government permittee does not assure other environmental obligations through a financial test, the local government permittee may assure closure, post-closure, and corrective action costs that equal up to forty-three percent (43%) of the local government permittee's total annual revenue.

(ii) If the local government permittee assures other environmental obligations through a financial test, including those associated with:

(AA) underground injection control (UIC) facilities under 40 CFR 144.62;

(BB) petroleum underground storage tank facilities under 329 IAC 9-8; (CC) polychlorinated biphenyls (PCB) storage facilities under 40 CFR 761; and

the local government permittee shall add those costs to the closure, post-closure, and corrective action costs the local government permittee seeks to assure under this subdivision. The total that may be assured must not exceed forty-three percent (43%) of the local government permittee's total annual revenue.

(iii) The local government permittee shall obtain an alternate financial assurance instrument for those costs that exceed the limits set in this clause.

(7) The local government guarantee option, including the following:

(A) A permittee may demonstrate financial assurance for closure, post-closure, and corrective action, as required by sections 2, 3, and 10 of this rule, by obtaining a written guarantee provided by a local government.

(B) The guarantor shall meet the requirements of the local government financial test in subdivision (6) and shall comply with the terms of a written guarantee as follows:

(i) The guarantee must be effective:

(AA) before the initial receipt of waste or at the time of the next required local government financial test annual submittal, whichever is later, in the case of closure and post-closure care; or

(BB) no not later than one hundred twenty (120) days after the corrective action remedy has been selected in accordance with the requirements of 329 IAC 10-21-13. (ii) The guarantee must provide the following:

(AA) If the permittee fails to perform any combination of closure, post-closure care, or corrective action of a facility covered by the guarantee, the guarantor shall:

(aa) perform or pay a third party to perform any combination of closure, post-closure care, or corrective action as required under this subitem; or

(bb) establish a fully funded trust fund as specified in subdivision (1) in the name of the permittee.

(BB) The guarantee will remain in force unless the guarantor sends notice of cancellation by certified mail to the permittee and to the commissioner. Cancellation must not occur during the one hundred twenty (120) days beginning on the date of receipt of the notice of cancellation by both the permittee and the commissioner as evidenced by the return receipts.

(CC) If a guarantee is canceled under subitem (BB), the permittee shall, within ninety (90) days following receipt of the cancellation notice by the permittee and the commissioner, complete the following:

(aa) Obtain alternate financial assurance under this rule.

(bb) Place evidence of that alternate financial assurance in the facility operating record.

(cc) Notify the commissioner.

(DD) If the permittee fails to provide alternate financial assurance within the ninety (90) day period under subitem (CC), the guarantor shall complete the following:

(aa) Provide alternate assurance within one hundred twenty (120) days following the guarantor's notice of cancellation.

(bb) Place evidence of the alternate assurance in the facility operating record.

(cc) Notify the commissioner.

(C) The permittee shall complete the following record keeping and reporting requirements:

(i) The permittee shall place a certified copy of the guarantee along with the items required under subdivision (6)(B)(iii) into the facility's operating record:

(AA) before the initial receipt of waste or at the time of the next required local government financial test annual submittal, whichever is later, in the case of closure and post-closure care; or

(BB) no not later than one hundred twenty (120) days after the corrective action remedy has been selected in accordance with 329 IAC 10-21-13. (ii) The permittee is no longer required to maintain the items specified in this clause when the permittee:

(AA) the permittee substitutes alternate financial assurance as specified in this rule; or

(BB) the permittee is released from the requirements of this rule in accordance with section 6 or 11 of this rule.

(iii) If a local government guarantor no longer meets the requirements of subdivision (6), the permittee shall, within ninety (90) days, complete the following:

(AA) Obtain alternative assurance.

(BB) Place evidence of the alternate assurance in the facility operating record.

(CC) Notify the commissioner.

If the permittee fails to obtain alternate financial assurance within the ninety (90) day period, the guarantor shall provide that alternate assurance within the next thirty (30) days.

(b) Financial responsibility closure cost estimate requirements must be as follows:

(1) For purposes of establishing financial responsibility, the permittee shall have a detailed written estimate of the cost of closing the facility based on the following:

(A) The closure costs derived under:

(B) One (1) of the closure cost estimating standards under subdivision (3).

(2) As used in this section, "establishment of financial responsibility" means submission of financial responsibility to the commissioner in the form of one (1) of the options under subsection (a).

(3) The permittee shall use one (1) of the following closure cost estimating standards:

(A) The entire solid waste land disposal facility closure standard is an amount that equals the estimated total cost of closing the entire solid waste land disposal facility, less an amount representing portions of the solid waste land disposal facility that have been certified for partial closure in accordance with:

(B) The incremental closure standard is an amount which, that, for any year of operation, equals the total cost of closing the portion of the solid waste land disposal facility dedicated to the current year of solid waste land disposal facility operation, plus all closure amounts from all other partially or completely filled portions of the solid waste land disposal facility from prior years of operation that have not yet been certified for partial closure in accordance with:

(c) Until final closure of the solid waste land disposal facility is certified, the permittee shall annually review and submit to the commissioner the financial closure estimate derived under this section within thirty (30) days after the annual submittal date. The funding must be established or updated within thirty (30) days after the original effective date of the establishment of responsibility for closure. The funding must be updated within thirty (30) days after the annual submittal date. annually not later than June 15. The submittal must also include a copy of the final contour map of the solid waste land disposal facility that delineates the boundaries of all areas into which waste has been placed as of the annual review and certified by a registered professional engineer or registered land surveyor. In addition, as part of the annual review, the permittee shall revise the closure estimate as follows:

(1) For inflation, using an inflation factor derived from the annual implicit price deflator for gross national product as published by the United States Department of Commerce in its Survey of Current Business. The inflation factor is the result of dividing the latest published annual deflator by the deflator for the previous year as follows:

(A) The first revision is made by multiplying the original closure cost estimate by the inflation factor. The result is the revised closure cost estimate.

(B) Subsequent revisions are made by multiplying the latest revised closure cost estimate by the latest inflation factor.

(2) For changes in the closure plan, whenever such the changes increase the cost of closure.

(d) The permittee may revise the closure cost estimate downward whenever a change in the closure plan decreases the cost of closure or whenever portions of the solid waste land disposal facility have been certified for partial closure under:

329 IAC 10-39-3 Post-closure; financial responsibility

Authority: IC 13-14-8-7; IC 13-15; IC 13-19-3

Sec. 3. (a) The permittee shall establish financial responsibility for post-closure care for all the permitted acreage of the solid waste land disposal facility before waste placement, except as provided by subsection (b). The permittee shall choose from the following options:

(1) The trust fund option, including the following:

(A) The permittee shall establish a trust agreement on:

(i) forms provided by the commissioner; or on such

(ii) other forms as approved by the commissioner.

(B) All trust agreements must conform to the requirements detailed in section 2(a)(1)(B) of this rule, with the exception that the term "post-closure" be substituted for the term "closure".

(2) The surety bond option, including the following:

(A) The permittee shall establish a surety bond on:

(i) forms provided by the commissioner; or on such

(ii) other form as forms approved by the commissioner.

(B) All surety bonds must conform to the requirements detailed in section 2(a)(2)(B) through 2(a)(2)(E) of this rule, with the exception that the term "post-closure" be substituted for the term "closure".

(3) The letter of credit option, including the following:

(A) The permittee shall establish a letter of credit on:

(i) forms provided by the commissioner; or on such

(ii) other forms as approved by the commissioner.

(B) All letters of credit must conform to the requirements detailed in section 2(a)(3)(B) through 2(a)(3)(D) of this rule, with the exception that the term "post-closure" be substituted for the term "closure".

(4) The insurance option, including the following:

(A) The permittee shall provide evidence of insurance on:

(i) forms provided by the commissioner; or on such

(ii) other forms as approved by the commissioner.

(B) All insurance must conform to the requirements detailed in section 2(a)(4)(B) through and 2(a)(4)(C) of this rule, with the exception that the term "post-closure" be substituted for the term "closure".

(5) The financial test for restricted waste sites option, including the following:

(A) This financial test is only available for restricted waste sites.

(B) If a permittee meets the criteria set forth in section 2(a)(5)(B) through 2(a)(5)(D) of this rule, the permittee shall be deemed to have established financial responsibility.

(6) The local government financial test option, including the following:

(A) This financial test is only available for permittees that are local governments. As used in this subdivision, "local government" means a county, municipality, township, or solid waste management district.

(B) If a permittee meets the criteria set forth in section 2(a)(6)(B) through and 2(a)(6)(C)of this rule, the permittee shall be deemed to have established financial responsibility.

(C) If, at any time, the permittee fails to meet the financial test, the permittee shall establish an alternate financial responsibility mechanism within one hundred twenty (120) days after the end of the fiscal year for which the financial data required by this clause shows that the permittee no longer meets the requirements.

(D) The commissioner may disallow use of this test on the basis of qualifications in the opinion expressed in the state board of accounts' annual financial audit of the permittee. An adverse opinion or a disclaimer of opinion is cause for disallowance. Other qualifications may be cause for disallowance if, in the opinion of the commissioner, the qualifications indicate the permittee does not meet the requirements of this subdivision. The permittee shall choose an alternate financial responsibility mechanism within ninety (90) days after notification of the disallowance.

(7) The local government guarantee option. If the local government guarantor and the permittee meet the requirements of section 2(a)(7)(B) and 2(a)(7)(C) of this rule, the permittee shall be deemed to have established financial responsibility.

(b) The permittee shall choose a financial responsibility mechanism, as provided in subsection (a), that guarantees funds will be available to meet the post-closure requirements of the solid waste land disposal facility, including the following:

(1) As applicable, funding must equal the amount determined under:

(2) Funding may be accomplished by initially funding the chosen financial responsibility mechanism in an amount equal to the amount determined under:

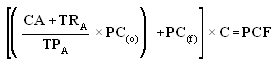

(2) Except for the trust fund mechanism, the permittee may completely fund the post-closure care amount, as determined under subdivision (1), based on the following formula and before the placement of any waste in the permitted area that is certified to receive waste:

| | | |

| Where: | CA | = | Total of existing acres certified to receive waste and acres that received waste previously. |

| | TPA | = | Total permitted acres. |

| | TRA | = | Total projected acres that will be certified to receive waste within the current annual update year, which is June 15 to June 15. |

| | PC(f) | = | Fixed post-closure costs. |

| | PC(o) | = | All other post-closure costs but fixed post-closure costs. |

| | C | = | Contingencies, which equals 1.25. |

| | PCF | = | Post-closure funding. |

Fixed costs include semiannual inspections and reports, access control and benchmark maintenance, ground water monitoring and well maintenance, and methane gas monitoring and maintenance.

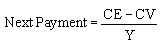

(3) For only the trust fund mechanism, funding may also be accomplished by making annual payments equal to the amount determined by the formula:

| | | |

| Where: | CE | = | The current total post-closure cost estimate as determined by subdivision (1). |

| | CV | = | The current value of the trust fund. |

| | Y | = | The number of years remaining in the pay-in period term of the original permit, which is five (5) years or less, or over the remaining life of the solid waste land disposal facility, whichever is shorter. |

Annual funding must be no accomplished not later than thirty (30) days after either each annual anniversary date of the first payment into the mechanism or the establishment of the mechanism, if no payments are required. June 15 of each year.

(c) The permittee shall submit an annual update for the amount calculated under subsection (b) for inflation and for changes in the post-closure plan, which increase the costs of post-closure, within thirty (30) days after the annual submittal date not later than June 15 of each year to the commissioner regarding post-closure financial assurance until final closure certification.

(d) If the formula in subsection (b)(2) is used, the permittee shall itemize separately both the fixed costs and all other costs.

(Solid Waste Management Board; 329 IAC 10-39-3; filed Mar 14, 1996, 5:00 p.m.: 19 IR 1922; filed Feb 26, 1999, 5:45 p.m.: 22 IR 2235; filed Aug 2, 1999, 11:50 a.m.: 22 IR 3871; filed Feb 9, 2004, 4:51 p.m.: 27 IR 1870, eff Apr 1, 2004; filed Jul 10, 2007, 2:26 p.m.: 20070808-IR-329050167FRA)

Hearing Held: January 16, 2007

Approved by Attorney General: July 2, 2007

Approved by Governor: July 10, 2007

Filed with Publisher: July 10, 2007, 2:26 p.m.

Documents Incorporated by Reference: None Received by Publisher

Small Business Regulatory Coordinator: Sandra El-Yusuf, IDEM Compliance and Technical Assistance Program, OPPTA-MC60-04, 100 North Senate Avenue, W-041, Indianapolis, IN 46204-2251, (317) 232-8578, selyusuf@idem.in.gov

Small Business Assistance Program Ombudsman: Eric Levenhagen, IDEM Small Business Assistance, Program Ombudsman, External Affairs - MC50-01, 100 North Senate Avenue, IGCN 1301, Indianapolis, IN 46204-2251, (317) 234-3386, elevenha@idem.in.gov

Posted: 08/08/2007 by Legislative Services Agency

DIN: 20070808-IR-329050167FRA

Composed: Apr 24,2024 8:52:53PM EDT

A PDF version of this document.

|