DEPARTMENT OF STATE REVENUE

Information Bulletin #4

Sales Tax

December 2018

(Replaces Bulletin #4 dated June 2016)

Effective Date: Upon Publication

SUBJECT: Sales to and by Indiana State and Local Governments, the United States Government, its Agencies, and Federal Instrumentalities

DISCLAIMER: Information bulletins are intended to provide nontechnical assistance to the general public. Every attempt is made to provide information that is consistent with the appropriate statutes, rules, and court decisions. Any information that is not consistent with the law, regulations, or court decisions is not binding on either the department or the taxpayer. Therefore, the information provided herein should serve only as a foundation for further investigation and study of the current law and procedures related to the subject matter covered herein.

Aside from nonsubstantive, technical changes, this bulletin is changed to reflect updates to guidance concerning the United States governmental exemption and the use of GSA SmartPay cards. The bulletin also clarifies that the exemption for state and local government agencies only applies to Indiana agencies and not to agencies of another state.

Generally, purchases of tangible personal property, accommodations, or utilities made directly by Indiana state and local government entities are exempt from sales tax. Sales by Indiana state and local government agencies also are exempt from Indiana sales tax unless the sales involve a proprietary or nontraditional activity (i.e., an activity that traditionally is engaged in by a private or commercial entity and that does not directly serve the public's general health, welfare, and/or safety).

Purchases of tangible personal property, accommodations, or utilities made directly by the United States government, its agencies, and instrumentalities are exempt from Indiana sales tax. Sales by these same entities are also exempt from sales tax.

State agency - means an authority, a board, a branch, a commission, a committee, a department, a division, or other instrumentality of the executive, legislative, or judicial departments of Indiana state government.

Local government - refers to any of the following:

• A municipal corporation (county, municipality, township, special taxing districts, etc.;

IC 36-1-2-10);

• Any agency of any of the above.

Federal Instrumentality - means an entity that is organized, created, or authorized under an Act of Congress and otherwise qualifies for inclusion under 26 U.S.C. 501(c)(1). The term does not include entities that are organized under 26 U.S.C. 501(c)(3).

III. PURCHASES BY STATE AND LOCAL GOVERNMENTS

The state of Indiana and its local governments are not subject to sales or use tax on any purchases to be used primarily to carry out a governmental function. Any purchases used primarily in connection with a proprietary function of the state or a local government are taxable unless some other specific exemption applies.

IC 6-2.5-5-44 provides that purchases of tangible personal property by a city or town to be used in the operation of a municipal golf course are exempt from the sales and use tax.

Traditional governmental activities such as police and fire protection; street construction and maintenance; and the operation of hospitals, public libraries, cemeteries, and similar activities are considered to be governmental functions.

A person who contracts with a municipality to operate, manage, or control any plant or equipment owned by the municipality for the collection, treatment, or processing of wastewater may purchase certain tangible personal property exempt from the sales or use tax. The property must be classified as collection plant expenses, treatment and disposal plant expenses, or system pumping plant expenses as defined in

IC 6-2.5-5-12.5.

A purchase is used "primarily" for a governmental function if the purchase is used more than 50 percent of the time in the performance of that function. To qualify for the exemption, the purchase must be invoiced directly to the state or local government making the purchase.

NOTE: If a state or local government employee purchases an item, the purchase is not exempt and the employee must pay sales tax at the time of purchase even if the employee is to be reimbursed by the governmental entity.

To purchase property exempt from tax, local governments must register with the department and issue an exemption certificate to the seller. To recover taxes paid on exempt purchases, the state agency or local government must file a claim for refund with the department.

A state agency that makes only exempt purchases is not required to register with the department. All state agencies should use the federal ID number and the state TID number issued to the Auditor of State on their exemption certificate (Form ST-105) when making exempt purchases. Additionally, Indiana state agencies issue procurement cards for travel expenses. When invoiced directly to the state or local government, purchases made by these cards are paid directly by the agency and therefore are properly exempt from Indiana sales and use tax without the need for an exemption certificate.

NOTE: This exemption only applies to Indiana state and local government entities. The governmental entities of another state (or governmental entities of a local government of another state) are not eligible for this exemption.

IV. SALES BY THE STATE OF INDIANA OR ITS LOCAL GOVERNMENTS

A state agency or local unit of government that sells tangible personal property and collects sales tax on those transactions is required to register as a retail merchant and remit the sales tax collected to the department. For example, the sale of key chains or license cases by a license branch is taxable. The state may purchase any property to be resold exempt from tax, but it must collect the tax from the purchaser at the point of sale. The following are other examples of proprietary activities that require the state agency or local unit of government to collect tax from the purchaser:

• Sales of tangible personal property from college bookstores; sales and rentals in state parks; food services and concessions; and similar activities;

• The rental of tangible personal property to the public;

• Sales of the byproducts of sewage disposal plants; or

• Any other activity customarily considered as being competitive with private enterprise.

Some sales may qualify as related to the performance of a governmental function if the sales do not compete with private enterprise. For example, if a city in Indiana were to charge a fee for providing copies of its ordinances, the city would not need to collect tax on the sale of the copies because providing the copies of its ordinances could be considered a governmental function of the city.

V. PURCHASES BY THE UNITED STATES GOVERNMENT AND ITS AGENCIES

The United States Constitution prohibits any state from imposing any tax directly on the U.S. government, its agencies, and federal instrumentalities, unless Congress consents to such taxation. Additionally, Congress has passed legislation prohibiting states from imposing taxes on entities that are instrumentalities not wholly owned or controlled by the U.S. government, such as the American Red Cross, federal land banks, federal reserve banks, federal credit unions, and federal home loan banks. Thus, much federal purchasing, leasing, and renting of tangible personal property; the use of utilities; meals consumed in restaurants; and other normally taxable goods or services (including accommodations for fewer than 30 days) are exempt from Indiana sales and other transaction-based taxes. However, the fact that the U.S. government, agency, or federal instrumentality may ultimately reimburse an employee who paid the tax does not exempt such a purchase from tax.

Example: An employee of a federal credit union pays for lodging costs from his own funds. Tax should be collected at the time of payment, since payment is not being made directly by the federal credit union. However, if the same employee pays for the lodging with a check from the federal credit union's account or by the use of a credit card that is billed directly to the federal credit union, then this is a direct expenditure by the federal instrumentality. Therefore, this transaction is exempt from sales tax.

A vendor is not required to collect sales tax on sales made directly to the U.S. government, its agencies, and federal instrumentalities if the exemption can be verified by documenting the facts and circumstances of the transaction. Instead of presenting an ST-105, a U.S. governmental entity exhibits an exempt transaction through the use of the General Services Administration (GSA) SmartPay® Program credit cards. Please see Appendix A for a detailed description of the GSA SmartPay® Program.

VI. SALES BY THE UNITED STATES GOVERNMENT OR ITS AGENCIES

Under federal law (4 U.S.C. 107), state and local governments may not levy or collect any type of sales or use tax on transactions in which the U.S. government sells personal property to others. Therefore, federal agencies are not required to register as retail merchants with the department and will not have a Retail Merchants Certificate number to use on an exemption certificate (Form ST-105 or SSTGB Form F0003).

VII. SALES TO FOREIGN GOVERNMENTS

Foreign missions and diplomats of foreign countries are provided exemption from certain state and local sales taxes by international treaty, provided their government grants such tax exemption to American Embassies and their personnel. The provisions of these treaties are administered by the Office of Foreign Missions.

Thus, for foreign missions, accredited members, and certain dependents, most purchases, leases, or rentals of tangible personal property; meals consumed in restaurants; and other normally taxable goods or services (including accommodations for fewer than 30 days) are exempt from Indiana sales and other transaction-based taxes. However, exemptions from sales tax at the point of purchase do not apply to the purchases of motor vehicles, gasoline/diesel fuel, or utility services. Further, the fact that a foreign mission may ultimately reimburse an otherwise eligible individual who paid the tax does not exempt such a purchase from tax.

The Office of Foreign Missions issues a Tax Exemption Card to foreign officials entitled to sales and use tax exemption. An individual's name, photograph, and personal identification appear on the card. There are several different types of cards with minimum purchase amount requirements and other conditions for exemption. Each card provides an explanation of conditions on the reverse.

A vendor is not required to collect sales tax on sales made directly to the foreign mission, accredited members, and certain dependents if the exemption can be verified by documenting the facts and circumstances of the transaction. The person claiming such an exemption should provide a copy of the Tax Exemption Card issued by the United States (or, in the case of Taiwan, the American Institute in Taiwan) and a properly executed exemption certificate (ST-105).

_________________________

Appendix A

NOTE: The following information is taken from the General Services Administration's (GSA) SmartPay website at https://smartpay.gsa.gov/ and other resources provided by the GSA, as well as Federation of Tax Administrators Bulletin B-07/02, dated Feb. 26, 2002.

FEDERAL GOVERNMENT ISSUANCE OF

CREDIT CARDS TO EMPLOYEES

On November 30, 1999, the Federal government through the General Services Administration (GSA) began a new credit card program called GSA SmartPay. Effective November 30, 2018, GSA SmartPay will be starting a new phase (GSA SmartPay 3). Charge cards issued under the program will have specific account number prefixes, as seen in the chart below. GSA SmartPay 3 accounts will be issued by Citibank and US Bank. The GSA SmartPay program provides four business lines: Purchase, Travel, Fleet, and Integrated. Accounts can be Centrally Billed Accounts (CBA) or Individually Billed Accounts (IBA).

Generally speaking, when a card is billed directly to the Federal government (CBI), any tax would be treated as being levied directly on the Federal government and therefore prohibited by the U.S. Constitution. A CBI card is proof that the purchase is exempt, and therefore an ST-105 is not required for the purchase. However, Indiana law requires that when the card is billed to the employee (IBA), the appropriate taxes must be applied to the purchase unless the employee can prove that the purchase is eligible for an exemption other than the exemption for purchases by the United States government by providing an ST-105.

What is the GSA SmartPay Program?

It is the largest federal government payments program. Many government employees will use a GSA SmartPay Purchase Card, Travel Card, Fleet Card, or Integrated Card as a form of payment when making authorized purchases, on official government travel, or when using a government fleet vehicle.

What are the Different Ways Federal Government Charge Cards Are Billed?

• Centrally Billed Account (CBA) expenses are directly paid by the federal government and should not be charged state taxes.

• Individually Billed Account (IBA) expenses are paid by the federal cardholder and are not eligible for state tax exemption, unless it is eligible for an exemption other than the exemption for purchases by the United States government.

All types of federal government charge cards include cards that are centrally billed, but only some SmartPay Travel Cards and Integrated Cards include cards that are individually billed.

What is a GSA SmartPay Purchase Card?

The GSA SmartPay Purchase Card is used by federal employees to purchase general supplies, goods and services. All Federal Government Purchase Card accounts are centrally billed.

What is a GSA SmartPay Fleet Card?

The GSA SmartPay Fleet Card is specifically designed for the purchase of fuel, maintenance services, and repair services of official government vehicles. All Federal Government Fleet Card accounts are centrally billed.

What is a GSA SmartPay Travel Card?

The GSA SmartPay Travel Card is used by federal employees for official government travel and travel-related costs, including airfare, lodging, meals, and so on. Federal Government Travel Card accounts may be centrally billed or individually billed. The type of account will be distinguished by the 6th digit of the account number, as reflected in the table below.

An example of a travel account is the GSA SmartPay Tax Advantage Travel Accounts, which are travel accounts that are in the name of an individual wherein specific Merchant Category Codes (MCCs) for lodging and/or rental cars are centrally billed to the Federal Government for direct payment. GSA SmartPay Tax Advantage accounts will be distinguished by the 6th digit of the account number, as reflected in the table below (a zero (0) in the 6th digit).

What is a GSA SmartPay Integrated Card?

The GSA SmartPay Integrated Card is a specialized card designed to combine the functions of the Purchase, Travel, and Fleet Cards into one charge card. Federal Government Integrated Card accounts are centrally billed or individually billed.

NOTE: The SmartPay Travel Card can be used by any federal agency. The SmartPay Integrated (combined) card is in use only by the Department of Interior.

Tax Status

All SmartPay cards that are centrally billed (CBA) cannot be taxed. Federal employee credit card purchases that are billed to the employee (IBA) must be taxed, unless the purchase is eligible for an exemption other than the exemption for purchases by the United States government.

Determining Whether a Card is Individually or Centrally Billed

To determine whether the travel or integrated card is a CBA (exempt) or an IBA (non-exempt), refer to the 6th digit of the account number on the card. Below are two tables that can help make that determination:

Table effective until November 30, 2018:

| | | | |

| Prefix (1st four digits) | Sixth Digit | Platform | Issuing Bank | Billing Type |

| 4486 & 4614 & 4716 | 0, 6, 7, 8, 9 | Visa | Citibank | Centrally Billed |

| JP Morgan Chase |

| US Bank |

| 4486 & 4614 | 1, 2, 3, 4 | Visa | Citibank | Individually Billed |

| JP Morgan Chase |

| US Bank |

| 5565 & 5568 | 0, 6, 7, 8, 9 | MasterCard | Citibank | Centrally Billed |

| JP Morgan Chase |

| US Bank |

| 5565 & 5568 | 1, 2, 3, 4 | MasterCard | Citibank | Individually Billed |

| JP Morgan Chase |

| US Bank |

Table effective November 30, 2018:

| | | | |

| | Purchase | Travel | Fleet |

| Prefix (1st four digits) | 4614 - Visa | 4614 - Visa | 4486 - Visa |

| 4716 - Visa | 4615 - Visa | 5563 - Mastercard |

| 5565 - Mastercard | 4486 - Visa | 5568 - Mastercard |

| 5568 - Mastercard | 5565 - Mastercard | 6900 - WEX |

| | 5568 - Mastercard | 7071 - WEX |

| | | 7088 - Voyager |

| 6th digit | N/A | 0 | GSA SmartPay Tax Advantage CBA by MCC | N/A |

| 1 | IBA |

| 2 - 4 | IBA |

| 5 | Reserved |

| 6 - 9 | CBA |

In addition to the second table provided above, please note the following information:

• Specific to Travel Accounts, use the 6th digit to identify whether the account is a Centrally Billed Account (CBA) (Digits 6-9), Individually Billed Account (IBA) (Digits 1-4), or GSA SmartPay Tax Advantage (Centrally Billed for specific MCCs) (Digit 0).

• The numbering structure for Integrated Cards to differentiate between centrally and/or individually billed transactions will be specific to each agency/organization using the Integrated card. This information is provided on the GSA SmartPay® website (www.gsa.gov/gsasmartpay) under the SmartPay Card Services "Tax Information" tab.

Records to be Kept

Sellers must keep proper documentation as follows:

• The vendor's copy of the invoice issued directly to the government agency must be kept when a CBA card is used.

• A photocopy of the GSA card.

• In the case of an IBA card where the purchaser is eligible for a different exemption, a signed copy of Form ST-105.

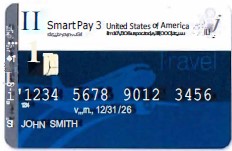

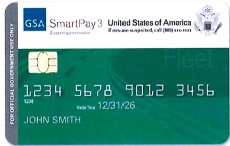

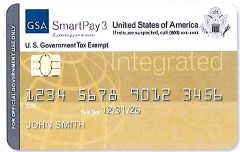

Card Designs

GSA SmartPay Purchase Card (CBA)

GSA SmartPay Travel Card (CBA)

GSA SmartPay Tax Advantage Travel Card (IBA)

GSA SmartPay Fleet Card (CBA)

GSA SmartPay Integrated Card (CBA)

Posted: 01/30/2019 by Legislative Services Agency

DIN: 20190130-IR-045190037NRA

Composed: Apr 29,2024 9:19:21PM EDT

A

PDF version of this document.